Frontier Economics' recently advised a number of clients in relation to the Queensland Competition Authority's review of its approach to climate change related expenditure. Below are some highlights and commentary on our advice included in the final position paper.

ensure its framework for assessing the prudency and efficiency of climate change related expenditure is fit-for-purpose and capable of incentivising timely investment when such expenditure would promote the long-term interests of consumers; and

provide greater clarity and certainty to stakeholders—including consumers and regulated businesses—on how the QCA intends to assess future proposals related to climate adaptation and mitigation expenditure.

Economic regulators need to perform a difficult balancing act when assessing expenditure proposals related to managing climate change risks. The impact of climate change on regulated infrastructure (and, therefore, on users of that infrastructure) is fraught with uncertainty.

If regulators set a low threshold for the prudency of climate change related expenditure, then consumers may pay more than the efficient amount required to manage climate change risks effectively.

Conversely, if regulators are too conservative in their assessment of climate change related expenditure, that may imperil the reliability and safety of the infrastructure used to deliver regulated services. This, in turn, may expose consumers to significant economic losses.

Uncertainty over whether regulators will approve climate change related expenditure—or over whether recovery of such expenditure would be disallowed once it has been incurred—may deter regulated businesses from making prudent and efficient investments to improve the resilience of their networks.

Clear guidance about how proposals for climate change related expenditure will be assessed by regulators can help reduce this uncertainty and encourage prudent and efficient investments that may otherwise be foregone.

For this reason, other economic regulators, should conduct their own reviews and publish formal guidelines on how they intend to assess regulatory proposals for climate change related expenditure. The QCA’s guidelines are not specific to any particular industry or jurisdiction, so would be a relevant starting point for other regulators and regulated businesses beyond Queensland.

Managing climate uncertainty to invest prudently and efficiently in resilience

Of the many issues covered by the QCA’s review, our advice focussed on the development of a framework to assess the prudency and efficiency of climate change adaptation expenditure.

Below are some highlights:

We advised Aurizon Network that:

“In assessing prudent and efficient ex ante resilience expenditure the QCA should encourage regulated entities to pragmatically incorporate the uncertainty inherent in climate change related risks into their proposals for adaptation expenditure.”

In our report to DBI, we added:

“Climate-resilience should be a necessary condition to project prudency and efficiency. Investing in infrastructure that is vulnerable, by design, to an accepted range of climate-related risks is likely to be lower cost in the short term but higher cost in total over the life of the asset.”

We discussed the development of an upfront expenditure framework that could facilitate investment under uncertainty, providing advantages to both regulated infrastructure providers and their customers. That is, a framework which:

is ex-ante in nature;

relies on the justification for the proposed expenditure;

includes in its ex-post review mechanisms a consideration of uncertainties related to climate-related risk; and

is proactive in managing long-term demand uncertainty.

We considered that these elements together would promote regulatory certainty and facilitate investment in prudent and efficient levels of infrastructure resilience.

The Coal Effect – funding and financing approaches to address residual stranding risk

Fossil fuel exposed firms are exposed to transition risk, or risks arising from the process of adjusting towards a lower-carbon economy. This can impact forecasted demand, the value of assets and liabilities, and thereby the risk profile and viability of the regulated business.

A key driver of transition risk for coal exposed companies is policy change. Net zero targets, can reduce domestic demand for coal. However, targets vary in status, development and expected achievement date. This uncertainty, in combination with uncertainty around technological development and carbon abatement costs, makes future demand for coal similarly unclear.

We identified a scenario where Aurizon Network may support more adaptation expenditure to increase the resilience of the network (with the expenditure to go into the regulatory asset base). However, future customers may be unwilling or unable to continue to pay for past adaptation expenditure. These factors create asset stranding risk, which may disincentivise a regulated business from investing in network resilience today, even if the investments are supported by current customers.

We then considered options the QCA might adopt to address asset stranding risk. We discussed the merits of addressing an increased stranding risk associated with climate change via an uplift to the allowed rate of return (i.e., the ‘fair bet’ approach) that would be just sufficient to compensate investors for the increase in stranding risk.

Also considered was the use of accelerated depreciation, which has been used by regulators in Western Australia (ERAWA) and New Zealand (the Commerce Commission) to address the stranding risks faced by gas pipelines following the adoption of emissions targets that have shortened the expected economic life of those regulated assets.

In our advice, we recommended that the QCA should confirm clearly that:

its regulatory framework will continue to provide regulated businesses with a realistic opportunity to recover past prudent and efficient expenditure over the long term;

regulatory allowances will be set such that climate change related expenditure that is deemed to be prudent and efficient, based on information available at the time, may be recovered over the expected economic life of the assets; and

the expected economic life of the assets should be reassessed periodically as new information becomes available.

Overall, we identified the benefits in the QCA providing clear upfront guidance on the types of information and evidence it would require from regulated businesses, to demonstrate asset stranding risks and management responses.

This could include the QCA needing to take into consideration a larger range of plausible future scenarios, rather than focusing on just the expected future profile of demand at a given point in time, reflecting the long-term uncertainty faced by the coal industry.

Frontier Economics Pty Ltd is a member of the Frontier Economics network, and is headquartered in Australia with a subsidiary company, Frontier Economics Pte Ltd in Singapore. Our fellow network member, Frontier Economics Ltd, is headquartered in the United Kingdom. The companies are independently owned, and legal commitments entered into by any one company do not impose any obligations on other companies in the network. All views expressed in this document are the views of Frontier Economics Pty Ltd.

At the International Institute of Communication’s Telecommunications and Media Forum, Sydney 2023 our Economist Warwick Davis joined a panel on competition issues in the sectors and commented on proposed merger reforms in Australia and the United States. He suggested that the Australian Competition and Consumer Commission (ACCC)’s proposed reforms for processes and legal tests for merger clearance will be contentious but seem more likely to produce economic benefits than the proposed changes to merger guidelines in the United States. This note explains the reasons for his view.

Merger reform proposals are a response to increasing market concentration

Competition authorities in many parts of the world are steering the debate on mergers towards sterner enforcement. The recently released details of proposed changes to merger enforcement in Australia and the United States show that competition authorities are on quite different paths to achieve that goal.

In Australia, details of the ACCC’s proposals for merger reform, as provided to Australian Treasury in March 2023, were recently released under Freedom of Information laws.[1]

The US Department of Justice and Federal Trade Commission (the Agencies) issued new draft merger Guidelines[2] for comment in July 2023. As in Australia, merger guidelines do not have the status of law, but they have been influential in US court merger proceedings.

The proposed changes are different, but they are both reactions to similar concerns – perceived harms from increasing market concentration that have not been prevented by merger laws and/or enforcement practices:

There is growing evidence to support the view that Australian markets are becoming more concentrated…It is important that Australia’s merger regime is effective in preventing increases in concentration before they occur.[3]

and:

[In the United States] Empirical research…has documented rising consolidation, declining competition, and a resulting assortment of economic ills and risks.[4]

Proposed changes to US Merger Guidelines renew emphasis on market concentration

The Agencies’ draft Guidelines have undergone a substantial change in form and substance from earlier versions.[5] The draft Guidelines show the Agencies’ desire to simplify the analysis of mergers that increase concentration or occur in concentrated markets, tied where possible to legal precedent. The FTC Chair has stated the draft Guidelines do not rely on “a formalistic set of theories” but “seek to understand the practical ways that firms compete, exert control, or block rivals”, and offer several ways to analyse transactions.[6]

The draft Guidelines have 13 specific guidelines that address analytical frameworks and specific challenges relating to serial acquisitions (creeping acquisitions in Australian parlance), buyer power in labour markets, platform markets and minority interests. This includes a return (in Guideline 1) to a stricter application of the ‘rebuttal presumption’ of market concentration that was first developed by the Supreme Court in 1961[7], and the introduction (in Guideline 6) of a rebuttable presumption in the case of vertical mergers, where a market share of more than 50% is involved.[8]

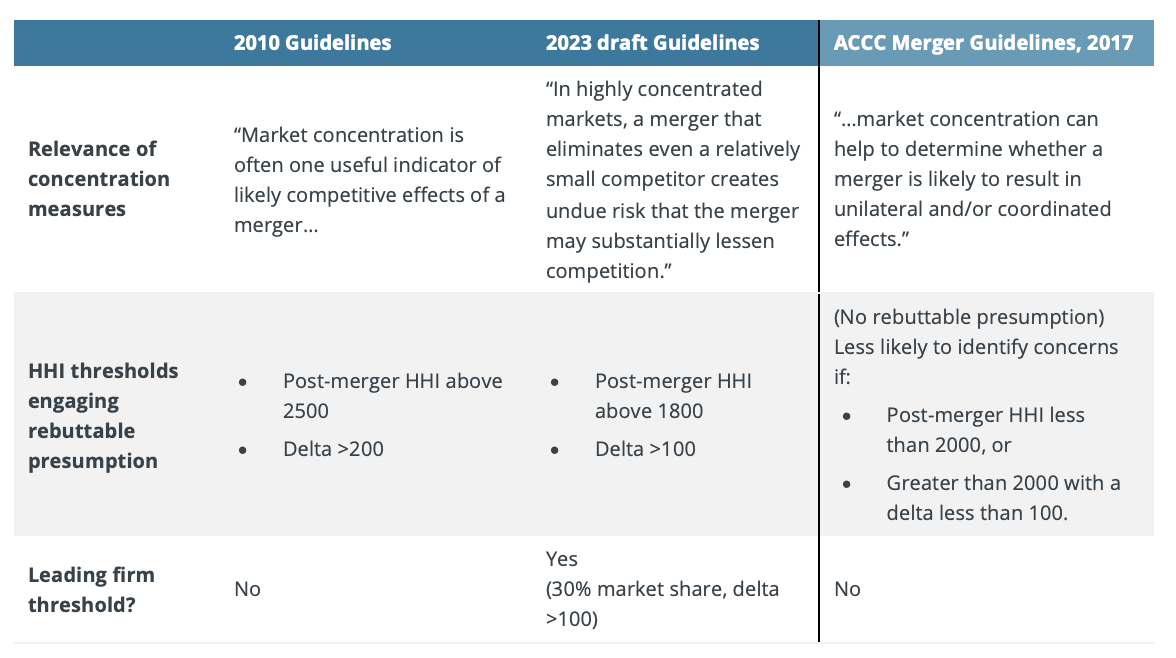

The changes from the 2010 version of the Guidelines on the significance of increasing market concentration are stark, as highlighted in Table 1. The thresholds at which the rebuttable presumption is engaged are reduced: in rough terms, a 6 to 5 merger of equally sized firms would now be subject to the rebuttable presumption while under the 2010 version it would not. For reference, the current ACCC Merger Guidelines approach (2017) is also highlighted, but these thresholds do not create rebuttable presumptions but instead provide an indication of the likelihood of concerns being raised.

Table 1: Changes in treatment of market concentration, US DOJ/FTC Merger Guidelines

Source: US Department of Justice and the Federal Trade Commission, Horizontal Merger Guidelines, August 19, 2010, draft Guidelines, p. 6, ACCC Merger Guidelines, 2017.

Similar problems, but different responses in merger reforms

The ACCC also has expressed concern with increasing market concentration. But the ACCC’s proposed reforms do not specifically focus on elevating market concentration to a more central role in merger analysis. Rather, the key elements of the ACCC’s reform proposals include:

A formal merger clearance regime: large mergers could not go ahead unless a clearance was obtained from the ACCC or Tribunal.

Changes to the merger clearance test: mergers can be blocked by the Federal Court under section 50 if they have the effect or likely effect of substantially lessening competition. The ACCC proposes that a merger would be cleared only if the ACCC (or Tribunal, on review) is satisfied that it is not likely to have the effect or likely effect of substantially lessening competition.

Revisions to the section 50 merger factors: added factors include an emphasis on creeping acquisitions and entrenching existing market power.[9]

Concentrating on the right measure of competition?

We have previously suggested that the ACCC’s proposed changes to the process by which mergers are assessed, including formal merger clearance, are worthy of serious consideration. The changes would address defects in the current informal clearance regime and adjudication processes, particularly by empowering the ACCC to be the principal decision-maker and increasing the transparency of its decisions.

On the added measures, the proposed ACCC reforms are better for not aiming directly at market concentration, albeit that concentration will remain a significant element of merger investigations. This is for two reasons:

Since the 1970s, economists have grown more sceptical of the causal connections between market concentration, competition, and economic performance. Concentration is only one factor in competitive health, and other market structures and conduct factors can be equally or more important.[10] For example, product differentiation, which is relevant to most mergers in Australia, highlights that the identity of competitors, and the similarity of their products, can have a greater influence on the competitive effects of mergers than aggregate concentration measures.

So much emphasis on concentration places an undue reliance on the defined markets. The definition of markets is rarely clearcut, particularly where products are differentiated, and is inevitably a matter of judgement.

Striking the right balance on the cost of errors

The ACCC’s proposed changes to the section 50 legal test are likely to have a significant impact on the chance of contentious mergers being proposed and approved. Mergers that have uncertain effects would be more likely to be blocked than under the current system.

One framework through which to view the proposed changes is whether they minimise the total costs of decision-making errors:

from not blocking anti-competitive mergers, and

from blocking mergers that pose no threat to competition.

Compared with the existing legal test, the ACCC’s proposed changes will reduce errors of the first kind while increasing errors of the second kind. Both kinds of errors are relevant: while errors of the first kind harm consumers directly, blocking mergers that are pro-competitive will also harm consumers.[11] Undoubtedly, the balance of errors is complex to assess and we expect further debate over whether the proposed change restores or upsets the right balance.

Other proposals to structural merger factors seem more likely to be positive. The proposals focusing on accumulation of market power address long-standing concerns about creeping acquisitions but avoid placing increased weight on market concentration thresholds. This leaves more room for nuance in the merger analysis.

A step in the right direction

The ACCC’s proposals are a serious attempt to improve the processes and outcomes of merger reviews. Although the ACCC may be concerned about market concentration, it is helpful that the ACCC has not looked to tie its proposals directly to that concern – as is being pursued in the United States. While further debate on changes to the legal test is justified, we expect the ACCC’s proposed changes have reasonable prospects of improving competition and economic welfare.

[4] Remarks of FTC Chair Lina M. Khan, Economic Club of New York, July 24, 2023, p.3.

[5] The Agencies have amended the guidelines several times since the first guidelines were released in 1968, including in 1982, 1984, 1992, 1997, 2010, and 2020.

[6] Remarks of Chair Lina M. Khan, Economic Club of New York, July 24, 2023, p.2.

[7]United States v. Philadelphia Nat. Bank, 374 US 321, 363 (1961).

[8] Draft Guidelines, p. 17: “If the foreclosure share is above 50 percent, that factor alone is a sufficient basis to conclude that the effect of the merger may be to substantially lessen competition, subject to any rebuttal evidence.”

[10] For example, in oligopoly settings, common market features such as cost asymmetry between firms or economies of scale can reverse the standard intuition that increasing concentration reduces economic performance.

[11] The ACCC suggests that the increased costs of errors will be borne by the merger parties rather than the public. That would only be true if the merger produced no efficiencies or did not otherwise benefit competition.

Frontier Economics Pty Ltd is a member of the Frontier Economics network, and is headquartered in Australia with a subsidiary company, Frontier Economics Pte Ltd in Singapore. Our fellow network member, Frontier Economics Ltd, is headquartered in the United Kingdom. The companies are independently owned, and legal commitments entered into by any one company do not impose any obligations on other companies in the network. All views expressed in this document are the views of Frontier Economics Pty Ltd.

Once thought of as purely an environmental issue, climate change is now recognised as a major threat to economies and financial markets around the world. As a result, public and private sector organisations are being asked to provide public disclosures of how current and future climate risks will impact their operations.

Recognising the increased need for climate change impact reporting with a greater focus on financial analysis, Frontier Economics and sustainability services consultancy Edge Environment are very excited to be partnering with each other to offer clients advice that combines in-depth environmental expertise underpinned by solid economic analysis and modelling.

“The requirements for climate disclosure reporting have been increasing around the world in recent years. We have seen climate change shift from being primary an environmental or “green” issue to one with legal, governance and financial implications” said Dr Mark Siebentritt, Edge’s Commercial Director and one of its climate risk analysis experts.

“We are seeing many of our clients step up their analysis of climate risk. This is in response to commentary by financial regulators in Australia about the need for companies to address what is now regarded as a foreseeable and material risk. Change is also coming through international markets with some countries like England and New Zealand headed toward mandatory climate risk disclosure reporting.”

One of the key challenges of climate risk disclosure reporting aligned to frameworks like the Taskforce on Climate Related Financial Disclosures (TCFD), is the need to better understand the financial implications of climate change.

“The impacts of climate change on the financial statements of an organisation is complex. Companies can find it challenging to do this as there are many drivers that need consideration. For example, take the impact of extreme heat on a property portfolio. You first need to understand the risk of such extreme weather in different climate change scenarios. Then you need to understand the physical impacts of extreme heat, this may include increased energy costs, damage to the property and even consideration of whether the property is unhospitable in extreme heat. Finally, you need to place a financial value on these physical impacts. Climate risk specialists and financial experts working together can give companies these insights” said Ben Mason, economist at Frontier Economics.

“A key risk companies are often interested in is around energy supply transitioning to renewables and the impacts on energy prices. We have energy network models and have provided shadow carbon price advice to various clients.”

Building on our expertise in TCFD reporting, Frontier Economics is expanding into ESG related advice more broadly. Ensuring decisions are based on sound and rigorous economics is critical for companies navigating this complex area.

Background

Edge Environment and Frontier Economics have worked across a broad range of climate risk projects, including within the property, infrastructure and government sectors. Together, this partnership provides a unique opportunity to better understand both financial risks and opportunities for Australian and New Zealand businesses.

About Edge Environment

Edge is a specialist sustainability advisory company focused on Asia-Pacific and the Americas. Its teams are based in Australia, New Zealand, the United States and Chile. Edge exists to help its clients create value from tackling one of world’s most fundamental challenges: creating truly sustainable economies and societies. Edge does this by combining science, strategy and storytelling in a way that gives our clients the confidence to take ambitious action, and do well by doing good.

About Frontier Economics

For more than twenty years, Frontier Economics has contributed sound economics to many important debates and decisions in Australia, New Zealand and the Asia-Pacific. Governments, regulators and businesses use our economic advice to inform policy development, market design, regulation and investment. Frontier Economics prides itself on delivering quality, independent economic input that can lead to better decisions and better outcomes for our clients.