Frontier Economics' recently advised a number of clients in relation to the Queensland Competition Authority's review of its approach to climate change related expenditure. Below are some highlights and commentary on our advice included in the final position paper.

ensure its framework for assessing the prudency and efficiency of climate change related expenditure is fit-for-purpose and capable of incentivising timely investment when such expenditure would promote the long-term interests of consumers; and

provide greater clarity and certainty to stakeholders—including consumers and regulated businesses—on how the QCA intends to assess future proposals related to climate adaptation and mitigation expenditure.

Economic regulators need to perform a difficult balancing act when assessing expenditure proposals related to managing climate change risks. The impact of climate change on regulated infrastructure (and, therefore, on users of that infrastructure) is fraught with uncertainty.

If regulators set a low threshold for the prudency of climate change related expenditure, then consumers may pay more than the efficient amount required to manage climate change risks effectively.

Conversely, if regulators are too conservative in their assessment of climate change related expenditure, that may imperil the reliability and safety of the infrastructure used to deliver regulated services. This, in turn, may expose consumers to significant economic losses.

Uncertainty over whether regulators will approve climate change related expenditure—or over whether recovery of such expenditure would be disallowed once it has been incurred—may deter regulated businesses from making prudent and efficient investments to improve the resilience of their networks.

Clear guidance about how proposals for climate change related expenditure will be assessed by regulators can help reduce this uncertainty and encourage prudent and efficient investments that may otherwise be foregone.

For this reason, other economic regulators, should conduct their own reviews and publish formal guidelines on how they intend to assess regulatory proposals for climate change related expenditure. The QCA’s guidelines are not specific to any particular industry or jurisdiction, so would be a relevant starting point for other regulators and regulated businesses beyond Queensland.

Managing climate uncertainty to invest prudently and efficiently in resilience

Of the many issues covered by the QCA’s review, our advice focussed on the development of a framework to assess the prudency and efficiency of climate change adaptation expenditure.

Below are some highlights:

We advised Aurizon Network that:

“In assessing prudent and efficient ex ante resilience expenditure the QCA should encourage regulated entities to pragmatically incorporate the uncertainty inherent in climate change related risks into their proposals for adaptation expenditure.”

In our report to DBI, we added:

“Climate-resilience should be a necessary condition to project prudency and efficiency. Investing in infrastructure that is vulnerable, by design, to an accepted range of climate-related risks is likely to be lower cost in the short term but higher cost in total over the life of the asset.”

We discussed the development of an upfront expenditure framework that could facilitate investment under uncertainty, providing advantages to both regulated infrastructure providers and their customers. That is, a framework which:

is ex-ante in nature;

relies on the justification for the proposed expenditure;

includes in its ex-post review mechanisms a consideration of uncertainties related to climate-related risk; and

is proactive in managing long-term demand uncertainty.

We considered that these elements together would promote regulatory certainty and facilitate investment in prudent and efficient levels of infrastructure resilience.

The Coal Effect – funding and financing approaches to address residual stranding risk

Fossil fuel exposed firms are exposed to transition risk, or risks arising from the process of adjusting towards a lower-carbon economy. This can impact forecasted demand, the value of assets and liabilities, and thereby the risk profile and viability of the regulated business.

A key driver of transition risk for coal exposed companies is policy change. Net zero targets, can reduce domestic demand for coal. However, targets vary in status, development and expected achievement date. This uncertainty, in combination with uncertainty around technological development and carbon abatement costs, makes future demand for coal similarly unclear.

We identified a scenario where Aurizon Network may support more adaptation expenditure to increase the resilience of the network (with the expenditure to go into the regulatory asset base). However, future customers may be unwilling or unable to continue to pay for past adaptation expenditure. These factors create asset stranding risk, which may disincentivise a regulated business from investing in network resilience today, even if the investments are supported by current customers.

We then considered options the QCA might adopt to address asset stranding risk. We discussed the merits of addressing an increased stranding risk associated with climate change via an uplift to the allowed rate of return (i.e., the ‘fair bet’ approach) that would be just sufficient to compensate investors for the increase in stranding risk.

Also considered was the use of accelerated depreciation, which has been used by regulators in Western Australia (ERAWA) and New Zealand (the Commerce Commission) to address the stranding risks faced by gas pipelines following the adoption of emissions targets that have shortened the expected economic life of those regulated assets.

In our advice, we recommended that the QCA should confirm clearly that:

its regulatory framework will continue to provide regulated businesses with a realistic opportunity to recover past prudent and efficient expenditure over the long term;

regulatory allowances will be set such that climate change related expenditure that is deemed to be prudent and efficient, based on information available at the time, may be recovered over the expected economic life of the assets; and

the expected economic life of the assets should be reassessed periodically as new information becomes available.

Overall, we identified the benefits in the QCA providing clear upfront guidance on the types of information and evidence it would require from regulated businesses, to demonstrate asset stranding risks and management responses.

This could include the QCA needing to take into consideration a larger range of plausible future scenarios, rather than focusing on just the expected future profile of demand at a given point in time, reflecting the long-term uncertainty faced by the coal industry.

Frontier Economics Pty Ltd is a member of the Frontier Economics network, and is headquartered in Australia with a subsidiary company, Frontier Economics Pte Ltd in Singapore. Our fellow network member, Frontier Economics Ltd, is headquartered in the United Kingdom. The companies are independently owned, and legal commitments entered into by any one company do not impose any obligations on other companies in the network. All views expressed in this document are the views of Frontier Economics Pty Ltd.

Building a business case to confidently manage climate-related risks and opportunities

Climate change impacts will continue to unfold across Australia with increasing severity in the years ahead. This will result in a set of complex and material financial implications for business. For Australian business to confidently rise to the challenge of systematically measuring, managing and mitigating risks and opportunities of climate change it will need a sound understanding of how climate change will most likely impact its finances. This Bulletin discusses Frontier Economics and Edge Environment’s approach to extending climate risk frameworks to build business cases for climate response against the inevitable, and potentially disorderly, climate transition ahead.

Australia is in the midst of cascading and compounding climate impacts

After centuries of relative climate stability, the world’s climate is changing. As average temperatures rise, acute hazards such as floods and fires and chronic hazards such as drought and sea level rise intensify. These hazards are categorised as the physical risks of climate change.

The frequency and severity of weather events in Australia is increasing and may further intensify as ecosystems are pushed beyond tipping points. Recent weather events in Australia such as the unprecedented rainfall and flooding in South-East Queensland, New South Wales and Victoria, extreme heat in Western Australia and the 2019–20 bushfires have resulted in highly significant financial losses for businesses and the communities they operate in.

Climate risk, however, remains an emerging discipline compared to other traditional risk areas. Climate risk management will necessarily grow in importance over coming years – recently, the Australian Prudential Regulation Authority (APRA) warned business around the need to prepare for “rapidly increasing expectations” on climate risk disclosure.

Against this backdrop, forward looking businesses are taking steps to understand, quantify and manage their climate risk exposures.The good news is we have the tools to address urban heat: integrated planning of our natural and built environment covering blue, green, and grey infrastructure.

TCFD is a lens to grapple with these risks

The Taskforce on Climate-related Financial Disclosures (TCFD) reporting framework has emerged as the global benchmark in climate risk reporting. It seeks to make businesses’ climate related disclosures comprehensive, consistent and transparent. TCFD enables effective investor analysis of a company’s demonstrated performance of incorporating climate related risks and opportunities into businesses’ risk management, strategic planning and decision making.

The TCFD was set up in 2017 by the Financial Stability Board – an international body of regulators, treasury officials and central banks – to provide voluntary recommendations on how business could voluntarily disclose the risks and opportunities from climate change (see Box 1).

Box 1: TCFD in brief

The purpose of TCFD is to provide a framework for organisations to make consistent and transparent climate-related financial disclosures. The TCFD framework document provides the following overview of the types of disclosures that it recommends:

Governance: Disclose the organisation’s governance around climate related risks and opportunities.

Strategy: Disclose the actual and potential impacts of climate-related risks and opportunities on the organisation’s businesses, strategy, and financial planning where such information is material.

Risk management: Disclose how the organisation identifies, assesses, and manages climate-related risks.

Metrics and targets: Disclose the metrics and targets used to assess and manage relevant climate-related risks and opportunities where such information is material.

It is recommended that the business provides its disclosures in their public annual reporting.

Source: Recommendations of the Task Force on Climate-related Financial Disclosures

Momentum in the market is growing and norms are being set

Since being first published in 2017, TCFD has been rapidly adopted by a broad range of organisations across the globe – the 2022 status report for TCFD points to TCFD “support” encompassing US$220 trillion of assets and US$26 trillion of combined company market capitalisation.

There is a trend towards mandating climate-related disclosures. Mandatory climate risk disclosures have been announced in jurisdictions including the UK, the EU, Hong Kong, Japan, Singapore and New Zealand. Significantly, the United States Securities and Exchange Commission has proposed rules to enhance climate-related risk disclosure drawing from the TCFD recommendations. Collectively, these actions will set norms and expectations for Australian businesses to develop their own disclosures.

In 2021 the New Zealand Government passed legislation mandating climate-related disclosures for around 200 financial entities. Further to impacting those covered by the introduction of this mandate, the move is widely expected to act as a catalyst for increased climate-related disclosures across businesses operating in the wider New Zealand economy.

Decision making under complexity needs tangible financial analysis

While TCFD is ultimately intended to support more informed capital allocation by investors, it can also be an important tool for organisations to respond to the risks and opportunities of climate change.

For an approach to inform practical decision making it needs to provide climate-related impacts in financial terms:

In the case of climate risks, the approach would allow for adaptation, mitigation and divestment intervention options to be directly compared to a “do nothing scenario”;

It would facilitate the valuation of climate-related opportunities, such as, product innovation, renewable energy generation, water recycling, resilient supply chains, and cost savings in energy or resource use; and

The approach will be flexible to recognise that risks and opportunities will vary depending on the region, market and industry that the business operates in.

Clearly this is a complex task, but it needn’t be daunting if we have the right tools and systematic approaches. Finding a solution requires assessing the changing climate exposure and vulnerabilities of an enterprise through time. A collaborative approach which brings together the key stakeholders across an enterprise provides the means to map the material climate impacts, their drivers and the likely financial consequences to the company. This collaborative approach also enables joint ownership of critical uncertainties to be addressed within business’ operations, financial reporting and data management. A structured approach is then required to cut through the uncertainty and deliver a clear path forward to adequately measure, manage and mitigate climate risks.

Frontier Economics and Edge Environment have partnered to combine our skills in financial analysis, ESG, risk management, climate science and sustainability to work through this complexity (see Box 2).

Box 2: Frontier Economics’ partnership with Edge Environment

Edge Environment and Frontier Economics have worked across a broad range of climate risk and resilience projects, mostly within the property, infrastructure and government sectors. Together, this partnership provides a unique opportunity to better understand both financial risks and opportunities of climate change for Australian and New Zealand businesses.

Edge is a specialist sustainability services company focused on Asia-Pacific and the Americas. Its teams are based in Australia, New Zealand, the United States and Chile. Edge exists to help its clients create value from tackling one of world’s most fundamental challenges: creating truly sustainable economies and societies. Edge does this by combining science, strategy and storytelling in a way that gives clients the confidence to take ambitious action, and do well by doing good.

Source: Frontier Economics

A collaborative approach is required to address this complexity

Confident climate-risk decision making requires a multi-disciplinary approach, incorporating climate science and financial analysis. However, deep technical expertise alone is not sufficient.

There is also a need for broad buy-in and engagement from within and across an organisation in order to access information, form granular insights, identify key operational climate-related impacts and quantify financial consequence. Organisations are encouraged to systematically look beyond the acute and direct impact of extreme events but also to the aggregated impacts of chronic and indirect effects of climate extremes.

Even with all these elements, it can be difficult to know where to start a climate-related financial analysis.

Frontier Economics and Edge have developed a practical approach

A useful starting point in analysing climate-related risk and opportunities is to assess the impacts of recent extreme climate events – such as the Eastern Australia bushfires and drought of 2019-20 and the extreme rainfall of 2021-22 – on a business’ operations and related cashflows.

This “looking back to look forwards” approach provides multiple advantages. It allows the:

development of logic maps, from climate drivers to asset and operational impacts;

identification of related notional financial consequences; and

engagement from across the business on climate-related risks and opportunities.

Shared understanding of the constraints and limitations in financial data management which may need to be addressed to enable the aggregated costs of climate impacts to be assessed with confidence

The logic mapping and notional financial consequences can then be tested and validated using actual operational and financial data to identify the impacts of recent extreme events.

This approach also clearly highlights any data gaps which limit the extent to which financial consequences can be isolated – providing insight to improve risk management systems.

This baseline analysis has standalone value as it provides a snapshot of the resilience of an organisation to recent climate change events which can be linked back to materiality thresholds in a firm’s enterprise risk framework. It is also vital in building a foundation for robust and defensible scenario analyses of the likely impacts of future climate extremes on an enterprise. It can be used to inform forward looking analysis of climate change impacts, which considers both cash flow and asset valuation risks and opportunities.

The approach taken by Frontier Economics and Edge Environment focusses on undertaking robust, transparent and actionable analysis. For example, we focus first on the short-term (to 2025) before extending analyses further into the future. A short-term lens reduces uncertainty and allows organisations to home in on impacts which require urgent action. It also allows for extensions such as cost-benefit analysis to support investment decisions around certain interventions.

Building the business case to confidently make decisions about managing your organisations climate risk is a journey – come and talk to us about getting started.

Today Austroads, with the assistance of Frontier Economics, released a Regulatory Impact Statement seeking feedback on proposed reforms to Heavy Vehicle drive licensing.

With a growing freight task and changing vehicle fleet, Australia needs a lot of well-trained and capable heavy vehicle drivers. Because of this transport Ministers requested Austroads look for ways to improve the National Heavy Vehicle Driver Competency Framework (NHVDCF) which informs state and territory heavy vehicle driver licensing arrangement.

Today Austroads, with the assistance of Frontier Economics, released a Consultation Regulatory Impact Statement (CRIS) seeking feedback on proposed reforms which include:

Introducing eligibility criteria that limits drivers with serious driving offences from applying to be a heavy vehicle driver.

Strengthening the skills, knowledge and competencies taught and assessed, in particular to recognise the extra skill needed to drive the most complex vehicles.

Requiring minimum behind-the-wheel time pre-licence and/or supervised driving sessions post-licence.

Introducing options that enable drivers who can demonstrate driving and work experience to obtain a licence to driver more complex vehicles more rapidly.

The C-RIS is available here and is out for comment until 28 October.

Frontier Economics regularly advises clients on a range of policy and regulatory matters in the freight sector.

Frontier Economics is pleased to announce that Alexus van der Weyden has been appointed a director of Frontier Economics Pty Ltd.

Alexus joined Frontier Economics in 2015. He is responsible to the board for Urban Economics and Water and has been instrumental in growing this practice area into a dynamic and innovative team with a strong roster of clients. Our work in urban economics and water applies economics to policy, regulation and investment planning projects across our urban environment, including place-based decisions covering water, liveability, open spaces and sustainable communities.

“Alexus is a strong economist. The growth and spread of our work in urban economics is testament to how much clients enjoy working with him and the results for them that he and the team have achieved together. ” said Danny Price, managing director of Frontier Economics. “I’m delighted that he’s come onto the board and look forward to working with him in this new chapter of his career”.

Alexus joins fellow directors Stephen Gray (chairman) and Andrew Harpham on the board, alongside Danny. “I’m excited about the challenge and being part of Frontier Economics’ future” said Alexus.

The Federal Court has declared by consent that Tasmanian Ports Corporation Pty Ltd (TasPorts) had breached section 46 of the Competition and Consumer Act by imposing a new port access charge on one of its customers, Grange Resources Ltd, after Grange notified TasPorts that it was going to switch to Engage Marine Tasmania Pty Ltd, a new provider of towage and pilotage services.

TasPorts is a corporation wholly owned by the State of Tasmania. It owns and operates the majority of ports in Tasmania and performs a range of port and marine operations at ports around Tasmania. Before Engage Marine entered the market, TasPorts was the sole supplier of pilotage and towage services at all major ports in Tasmania. TasPorts does not own Port Latta; it is owned by Grange, which operates the Savage River iron ore mine and exports iron ore from Port Latta in northern Tasmania. Grange was dissatisfied with the quality of service and the prices charged by TasPorts for towage and pilotage services; and it decided to purchase these services from Engage. TasPorts responded by imposing new port access charges on Grange.

The Australian Competition and Consumer Commission (ACCC) retained Frontier Economics to advise on the economic issues of the case. The ACCC lodged the expert testimony of Philip Williams of Frontier Economics (and a Statement in Reply to the testimony lodged by TasPorts) with the Court.

How real options analysis improves decision making

Standard techniques used to appraise commercial and government investments often ignore the value of flexibility to adapt investment strategies as circumstances change. Misvaluation of this kind can result in suboptimal investments being chosen. This problem can be particularly acute for infrastructure projects, which typically involve large sunk costs and uncertainty over long asset lives. Real options analysis addresses this shortcoming by valuing flexibility explicitly, thereby promoting better decision-making.

Making decisions under uncertainty

The 6th of June 1944 marked the beginning of the Battle of Normandy, a decisive turning-point in World War II that led to the liberation of Western Europe. Under General Dwight D. Eisenhower’s bold plan, 160,000 Allied troops would cross the English Channel under cover of darkness, land on several beaches in Northern France and push deep into German-held territory. The Normandy landings remain the largest seaborne invasion ever recorded, and one of the most successful Allied campaigns during World War II. However, the whole endeavour was nearly scuppered by the most mundane of things: bad weather.

The landings were originally planned for the 5th of June. However, it became clear by the 4th that heavy winds and rough seas would make the audacious landings impossible. Meteorologists advising Eisenhower forecast that conditions would improve sufficiently by the 6th for the invasion to proceed. The Allied Commander wisely heeded the advice to delay, changed plans that had taken months of meticulous preparation—and the rest, as they say, is history.

Flexibility when making decisions is valuable not just in military strategy. All of us adjust our plans in response to changing circumstances and new information—whether that entails taking a different route home from the usual one to avoid traffic, or more life-changing choices, like whether to buy a house when the outlook for the property market is highly uncertain.

Commercial and public investment decisions are no exception. Businesses and governments making major investment choices often do so in the face of significant uncertainty about the future. Rarely are the investment choices completely fixed. Investment plans can often be adapted—for example, by waiting to see what happens rather than taking a decision now, or by pursuing a different investment strategy—when confronted with new information that affects the value of the investment.

Bizarrely, even though many investors do in practice change their behaviour in response to new information, the techniques typically used to value investments ignore this flexibility. For example, standard Net Present Value (NPV) analysis used in commercial investment appraisals and cost-benefit analysis (CBA) used to assess the net public benefits of government investments generally assume fixed investment plans that cannot be revised, regardless of how circumstances change.

If the flexibility to change investment strategies is valuable—and it can be materially so in many situations—then standard NPV analysis and CBA will understate the value of investments. Investors who realise this often resort to ad hoc, qualitative judgment in order to take account of the value of flexibility—usually an excellent way to make bad decisions.

Worse still, what happens if two competing investment options are being considered side-by-side, but one presents the investor with more (or different kinds of) flexibility than the other? How are those two options to be compared on a like-for-like basis? Unless the flexibility is valued quantitatively, there is every chance that the two investment opportunities will not be compared on a level playing field, and the wrong (i.e., value-destroying) investment may inadvertently be selected.

The value of flexibility: a simple example

Figure 1 presents a simple example, which shows that when faced with uncertainty, flexibility to respond to new information can increase the value of an investment.

Consider two investment options available to an investor.

Under Option 1, the investor can invest at Time 0 at a cost of $10 million. The investment will provide a guaranteed cash flow of $1.25 million at Time 1. However, the cash flows at Time 2 (and thereafter) are uncertain: with equal probability they will either rise to $2 million, or fall to $0.5 million. This uncertainty resolves only at Time 1. Under Option 1, this occurs after the investment decision has been. If the investor takes Option 1, the expected NPV of the investment (at a constant discount rate of 10%) would be $2.5 million.

Note that the expected NPV represents the average outcome, given that there is a 50/50 chance of cash flows from Time 2 onwards increasing or falling significantly. If the investor is unlucky and cash flows drop, then the actual NPV of the investment would be -$6.59 million. The investment would have turned out to be a very bad one.

Under Option 2, the investor could—in recognition of uncertainty about the future—wait until Time 1 and choose to invest only if the cash flow at each point in time increases to $2 million. This would mean giving up a guaranteed cash flow of $1.25 million at Time 1. However, in exchange, the investor can avoid an outcome where the cash flow drops significantly and forever to $0.5 million, producing a loss-making investment. If the investor takes Option 2, the expected NPV of the investment would be $4.55 million—significantly higher than under Option 1, where the investment would occur immediately regardless of future uncertainty. By selecting Option 2, the worst the investor can do is avoid losses by not investing if the cash flows decline.

The difference in the NPVs under Options 1 and 2, $2.05 million, represents the economic value of flexibility (the ‘option value’) to change the investment strategy in response to new information.

Real options analysis

Real options analysis (ROA) is a technique that allows the systematic quantification of the economic value of flexible decision-making. Unlike standard NPV analysis or CBA, ROA recognises that investors can alter the way a project is rolled out as circumstances change and calculates the value of the project under different possible investment strategies rather than a single, fixed strategy.

Examples of flexibility in decision-making that ROA can account for include the options to:

delay investment until uncertainty is resolved;

roll the investment out sequentially to see how each stage pans out before progressing to the next;

change course, expand or downsize as new opportunities and risks crystallise; and

abandon/exit if conditions turn unfavourable.

ROA has two main advantages over standard NPV analysis and CBA:

Firstly, ROA can provide a more accurate valuation of potential projects by accounting explicitly for the fact that the investment strategy can be modified in response to changing circumstances. This removes the need to account for the value of flexibility qualitatively and reduces the risk of selecting a suboptimal investment.

Secondly, ROA allows the identification of the value-maximising investment strategy. This is because ROA involves mapping out all the feasible future pathways for an investment, in response to changing circumstances, and then finds the pathway that would maximise the value of the investment. This value-maximising pathway represents the optimal investment strategy, given the present understanding of how the future might unfold.

When is flexibility valuable?

A key insight from the ROA literature is that the value of flexibility can be particularly large if:

There is significant uncertainty over the future payoffs (e.g., cash flows, social costs/benefits) from the investment. If future outcomes are easy to anticipate, then planning would be straightforward, and there would be little need to modify the investment strategy over time. In this context, uncertainty refers to the variability of possible future outcomes. The larger the range of possible future outcomes, the greater the uncertainty faced by investors, and the greater will be the value of flexibility.

The investment decision is irreversible (or is very costly to reverse). If investment decisions can be undone easily, then investors could simply withdraw from the investment without incurring a significant loss. However, if the cost of the investment is sunk once made, then investors cannot exit without suffering a loss. Generally, the larger the sunk cost involved, the greater will be the value of flexibility.

This means ROA can be particularly useful when valuing infrastructure investments—such as: roads, rail lines, ports, airports, water networks, desalination plants, water recycling plants, telecommunications networks, mining and exploration assets, gas pipelines, electricity grids and power stations.

This is because infrastructure investments tend to be long-lived (so economic conditions can change materially over the life of such assets), and typically involve billions in sunk costs.

The NBN: an application of ROA

With a forecast peak funding requirement of $51 billion, the National Broadband Network (NBN) represents the largest infrastructure project ever undertaken in Australia.

Given the size of the project, it is astonishing that the Rudd Labor government, which pledged to deliver the NBN, refused to conduct a CBA to assess its merits. Indeed, the Federal Communications Minister at the time argued that the benefits of the NBN to Australia were self-evident, and that conducting a CBA would be a “waste of time, waste of effort, waste of money.”

The most contentious aspect of Labor’s NBN plan was a commitment to deliver fibre to the premises to 93% of the population with broadband speeds of up to 100 megabits per second. The ambitious choice to build fibre to the premises was intended to deliver a network with sufficient capacity to last for generations, but also involved the highest construction costs.

The decision to roll out fibre to the premises was particularly controversial because it was unclear in 2009, when the plan was first announced, that there would be sufficient future demand to justify the broadband speeds and build costs associated with a fibre to the premises network. Whether fibre to the premises would be truly worthwhile depended on what sort of applications would emerge, and how consumers would choose to use broadband services, in future. However, the government of the day pressed on with its plans for a “Rolls-Royce” NBN as though such speeds would definitely be required, regardless of the uncertainty over future demand. No account was taken of the option to delay or to build gradually.

When Labor lost the 2013 general election, the incoming Coalition government commissioned a CBA of the project. That study assessed the net benefits to taxpayers of three options for rolling out the NBN. It concluded that, against the base case scenario of halting the project immediately:

A rollout using hybrid-fibre coaxial and fibre to the node to 93% of premises, without any government subsidy, would provide the highest incremental net benefit of $24 billion;

A multi-technology mix rollout using a combination of fibre to the premises, fibre to the node, hybrid-fibre coaxial, fixed wireless and satellite solutions would deliver incremental net benefits of approximately $18 billion; and

A fibre to the premises rollout to 93% of premises (per the original Labor plan) would deliver incremental net benefits of less than $2 billion.

The study suggested that Labor had picked the worst of all rollout options.

A commendable aspect of the CBA—which made it stand out compared to most other government CBAs—was that it made some effort to account for optionality. The CBA recognised that a key uncertainty was the extent of future growth in demand for high-speed broadband. The study concluded that whilst a multi-technology mix rollout would offer slower speeds than a fibre to the premises rollout, it would allow the NBN to be upgraded at a later date, if demand turned out to be higher than anticipated.

The authors of the CBA modelled the net benefits of having the ability to upgrade later if required, under a multi-technology mix rollout, instead of building full fibre to the premises capability upfront. Figure 2 presents the value of the multi-technology mix rollout over and above the fibre to the premises rollout if:

the network was never upgraded, even if consumers’ willingness to pay for high-speed broadband were to increase over time (the black curve); and

the network was upgraded in response to growing willingness to pay (the dashed red curve).

This analysis demonstrated two important things:

Firstly, once the flexibility to upgrade the network in response to demand growth had been accounted for, the multi-technology mix rollout looked unambiguously better than the fibre to the premises option. Had this flexibility been ignored, a multi-technology mix build would have appeared a worse option than fibre to the premises under a high willingness to pay scenario (i.e., the black curve eventually drops below an NPV of $0), when in fact it was not.

Secondly, it is possible to extend standard CBA using ROA to quantify the value of flexibility. The red curve represents the value to be gained from following the most flexible investment strategy. This allows decision-makers to understand in dollar terms what society would be giving up if a less flexible strategy (i.e., a fibre to the premises rollout) were adopted instead, given uncertainty about the future.

Based on these results, the CBA concluded that:

Overall the [multi-technology mix ] MTM scenario has significantly greater option value than the [fibre to the premises] FTTP scenario. The MTM scenario leaves more options for the future open because it avoids high up‐front costs while still allowing the capture of benefits if, and when, they emerge. It is, in that sense, far more ‘future proof’ in economic terms: should future demand grow more slowly than expected, it avoids the high sunk costs of having deployed FTTP. On the other hand, should future demand grow more rapidly than expected, the rapid deployment of the MTM scenario allows more of that growth to be secured early on, with scope to then upgrade to ensure the network can support very high speeds once demand reaches those levels.

Making us better off

John Maynard Keynes is often credited with saying “When the facts change, I change my mind. What do you do, sir?” In fact, the actual source of this quote was not Keynes, but Paul Samuelson, another famous economist.

Regardless of who actually said the words, the sentiment behind them makes intuitive sense to most of us. We do not go through life following a perfect linear path, regardless of what life throws at us. We adapt our plans as circumstances change because doing so makes us better off.

Commercial and government investment decisions are much the same. Yet, standard NPV analysis and CBAs used to appraise such investments typically ignore the value that can be gained from changing the investment strategy in response to new information. This can result in the value of investments—particularly those that are long-lived, exposed to significant future uncertainty and involving large sunk costs—being mis-estimated. This, in turn, can lead to suboptimal investments being selected, at significant cost to shareholders or taxpayers.

ROA addresses this problem by quantifying explicitly the value of flexibility, and allowing identification of optimal investment strategies, thereby improving decision-making.

To download this publication in full (including references), click the button below.DOWNLOAD FULL PUBLICATION

The Heavy Vehicle National Law regulates the use of heavy vehicles on roads. Its purpose is to ensure that heavy vehicles and their drivers are safe and that they operate on suitable routes to minimise public safety risks.

The reforms being considered aim to improve heavy vehicles’ access to roads, vehicle roadworthiness and safety and the management of driver fatigue. Refinements to the supporting assurance regime and regulatory tools are being considered along with reforms to enable greater use of technology and data for compliance purposes.

The National Transport Commission is now seeking formal submissions on the Consultation regulatory impact statement. They aim to finalise the policy options for ministers’ decision in the first half of 2021.

Frontier Economics assisted the National Transport Commission to draft the consultation regulatory impact statement and assess the impact of the policy reform options being considered.

Frontier Economics advises clients in the transport sector on a range of economic issues.

Shirley the government can't be serious?

Economists are usually sceptical of governments getting into the business of owning and running commercial firms. Governments face complex and competing objectives, and this rarely leads to good outcomes. The experience of Air New Zealand in the 2000s, however, suggests that bad outcomes are not a given. If the Queensland Government acquires a stake in Virgin Australia, could it learn from the nationalisation of Air New Zealand? And could those insights have any broader relevance to Australia in the wake of the COVID-19 pandemic?

Grounded

On 21 April 2020, Virgin Australia—Australia’s second-largest airline—announced that it was entering voluntary administration. It was dubbed “Australia’s first big casualty of the coronavirus pandemic.”[1] Whilst it was true that the economic and travel shutdowns caused by the COVID-19 crisis had a devastating impact on its revenue streams, in reality Virgin Australia had been in trouble for some time. The company had posted large losses of $90 million or more in every year since 2013, and by 2020 was groaning under the burden of over $5 billion in debt.

In late March 2020, Virgin Australia had approached the Federal Government for a $1.4 billion loan but was rebuffed. Its major shareholders—many of whom were themselves airlines facing financial strain as a result of the global pandemic—also refused to inject new capital into the business. By early April, as it became clear that the airline was nearing collapse, many urged the Federal Government to take an ownership stake in the company to rescue the failing airline. The main arguments for doing so were firstly to maintain a viable competitor to Australia’s largest carrier, Qantas, and secondly to save thousands of jobs.

Whilst the Federal Government showed no interest in nationalising Virgin Australia, on 13 May 2020 the Queensland Government announced its intention to bid for a direct stake in the company via the Queensland Investment Corporation (QIC). Whilst the Queensland Government has indicated that its ownership of Virgin Australia would be at arm’s length through QIC, it has also made clear that its interest in the airline is motivated in part by wider policy considerations. For instance, the Queensland Treasurer has stated that:[2]

My number one focus as Treasurer is to retain and create jobs for Queenslanders, particularly as we move beyond the COVID-19 crisis.

We have been very clear. Two sustainable, national airlines are critical to Australia's economy. We have an opportunity to retain not only head office and crew staff in Queensland, but also to grow jobs in the repairs, maintenance and overhaul sector and support both direct and indirect jobs in our tourism sector.

Partial or total government ownership of airlines around the world is not rare. Some of those carriers are very successful commercially—Emirates and Singapore Airlines, to name just two. Others, however, have lamentable track records of safety and financial performance. For example, Air India, which is currently 50% publicly-owned, has accumulated losses over the past decade topping an eye-watering AU$14 billion (Rs696 billion).[3] When the Indian Government tried to sell its stake in the airline in 2018, not a single bid was received.[4]

Taking a broader view of costs and benefits

A benefit of public investment is that the government can take into account broader social costs and benefits. In the short-term, there might be some (net) benefits if investment can (i) deliver short-term financial stability (ii) preserve competition or (iii) maintain transport links that would otherwise be severed if a major airline were to fail. Transport links are essential to economic activity and losses of links can be very detrimental to communities.[5]

A key issue here is the counterfactual (the state of the world without the government investment). It might be possible to create a positive net impact on economic activity, particularly if the counterfactual is no service at all. In the short-term, this might require capital injections and financial stability, which only the government may be able or willing to provide in a time of crisis.

The benefit of government investment can also be its greatest weakness. By introducing objectives other than purely commercial objectives, it can destroy rather than create economic value—by allowing inefficiency to creep in. This means that taxpayers, who did not have a direct say in whether their money should be invested in the enterprise, may not get the best return on that investment.

Such problems may be manageable in the short run. However, the longer the government remains an investor, the greater the risk that such conflicting (and vested) interests may arise.

So, if the Queensland Government is serious about taking an ownership in Virgin Australia, how can it ensure that its investment delivers the potential benefits outlined above, rather than the disadvantages?

The Kiwi that learned to fly

One standout success story of government investment and ownership of an airline is Air New Zealand. In 2001, like Virgin Australia, New Zealand’s national carrier was on the brink of collapse. It had expanded aggressively throughout the 1990s into Asia and Australia, culminating in the full acquisition of Australia’s second-largest airline at the time, Ansett Airlines, in 2000.

Ansett was a larger company than Air New Zealand and required significant equity injections to upgrade the safety of its fleet. Ansett also faced growing competition from Qantas and Virgin Australia (which was known as Virgin Blue at the time). Unable to control ballooning costs, Ansett folded in September 2001. Air New Zealand posted a loss of NZ$1.425 billion for the year to June 2001, including an asset write-down of NZ$1.32 billion relating to Ansett. This led to Air New Zealand’s credit rating being downgraded to ‘junk’ status,[6] and its share price fell by over 80% between late August and late September 2001.

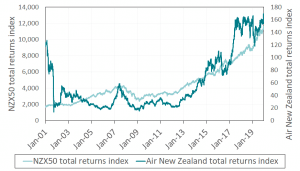

In October 2001, the New Zealand Government took an 82% ownership stake in the company at a cost of NZ$885 million. Over the next decade, Air New Zealand set about reorganising and improving its business model. The company returned to profitability in 2003, and posted a net profit after tax of NZ$290 million in 2019. Between October 2001 and December 2019, the total returns delivered by Air New Zealand stocks increased by nearly 12%, outperforming the New Zealand stock market (see Figure 1). In November 2013, the Government sold a 20% stake in the company, gaining NZ$365 million, leaving it with a 53% share.[7]

Figure 1: Air New Zealand and NZX50 total returns

The secret of Air New Zealand’s success

By almost any measure, the New Zealand Government’s intervention to bail out Air New Zealand has, with hindsight, turned out to be a success. The injection of much-needed capital stabilised the business. Moreover, knowledge that an investor with very deep pockets was now standing behind the airline gave other investors, including lenders, greater confidence in the company.

However, the real secret to Air New Zealand’s recovery was a change in the way the business was managed and governed.

Good governance

A new Board and management team was appointed, following the public acquisition of Air New Zealand. The new CEO, Ralph Norris, accepted the role on a number of conditions. The first of those was that the Government should stay out of operational decisions. Norris has stated that:[8]

We can't divorce business from the community. But that doesn't mean we should be any more obligated than any other commercial organisation in the country.....My job is to get on and run the business commercially - not as an arm of social policy. I wouldn't have taken the role if I'd seen Air NZ as an arm of Government. I'm here to steer this company around and I believe the relationship between management and the board will be good one.

This freedom from government interference allowed Air New Zealand’s management team to overhaul the company’s business model. The company adopted a low-cost airline model for domestic and trans-Tasman flights, relaunched a more focussed long-haul business and invested heavily in improving customer service.

The new management also reduced staff numbers significantly, and negotiated lower pay for remaining staff, in order to bring costs under control and return the company to profitability.[9] It seems unlikely that such restructuring would have been possible if the Government allowed itself to intervene in operational decisions.

Owner’s incentives

The Government was explicit when it took an ownership stake in Air New Zealand that it did not intend to remain a long-term investor in the business. For example, the Finance Minister at the time, Dr Michael Cullen, stated in parliament that:[10]

…any investment by the New Zealand government in Air New Zealand will ensure that there is effective control for a period in time but it will be subject to a clear message that the government does not see itself the long term shareholder in the company.

This meant that the Government was motivated to ensure that Air New Zealand would return to profitability quickly, and deliver as high a commercial return to taxpayers’ investment as possible. This clear objective made it possible for the Government to step back and allow the business to be run commercially. This appears to have been a successful approach even though the Government has ended up being a longer-term shareholder.

Market discipline

Another ingredient in Air New Zealand’s winning formula was that it remained a publicly-listed company. One of the most important benefits of being a publicly-listed firm is the availability of a stock price that embodies the market’s sentiment about the value of the business. If the market considers that the firm is performing well, the price will increase. However, if the market thinks that the firm is performing badly, the price will fall.

In Air New Zealand’s case, the availability of a share price would have given the Government a clear idea of what it could sell its shares for. But it also provided an important market discipline: Government intervening in the operations of the business in ways that may destroy value would be clearly visible.

Moreover, many of the owners of Air New Zealand’s listed shares were mum and dad investors, who also happened to be voters. Any meddling by the Government that destroyed value to those investors would not have been viewed favourably, come the next election. This was perhaps another factor that helped restrain any temptation by the Government to intervene in a non-commercial way.

Lessons for Australia

The COVID-19 pandemic has created unprecedented economic challenges for businesses in Australia and elsewhere. Now more than ever, governments may feel pressure to intervene by taking stakes in struggling firms that are viewed as somehow essential to the public interest. The airlines industry—and the story of Air New Zealand in particular—shows that government intervention of this kind need not destroy economic value.

The benefit that government investment or ownership brings, apart from major capital injections, is the ability to restore confidence to other investors that standing with them is a large, well-resourced investor who also has some skin in the game. This can be invaluable in restoring stability during a crisis.

The big risk with government investment is that this new, large investor will be motivated by considerations other than maximising returns—such as winning the next election—and that this investor will use its clout within the business to pursue non-commercial objectives that ends up destroying value.

The Air New Zealand case shows that if a government:

treats its investment as temporary

can provide the business with clear, unambiguous commercial objectives and

can restrain itself from meddling in the day-to-day affairs of the business

then public investment can produce outcomes that benefit taxpayers as well as other investors. While there are no guarantees of success, the Queensland Government may well be serious…and don’t call them Shirley!

[1] BBC, Virgin Australia slumps into administration, 21 April 2020.

[2] Financial Review, 'Project Maroon': Queensland breaks cover in Virgin race, 13 May 2020.

[3] Business Today, Air India net loss at all-time high of Rs 8,550 crore in FY19, says aviation minister, 5 December 2019.

[4] The Hindu, Now, govt goes for 100% stake sale of Air India, 28 January 2020.

[6] CNN, Air NZ hits back over Ansett collapse, 17 September 2001.

[7] Sydney Morning Herald, NZ government sells 20% of Air New Zealand for $324 million, 20 November 2013.

[8] Management New Zealand, Unfinished business: Why Ralph Norris is flying Air NZ, 4 April 2002.

[9] It was estimated at the time that 800 of Air New Zealand’s 9,300 staff would need to be made redundant in the first round of restructuring. New Zealand Herald, Job losses likely to hit 800 in Air NZ cutbacks, 9 October 2001.

[10] Response to parliamentary questions by Dr Michael Cullen, 3 October 2001.

On 6 May 2020, the Full Court of the Federal Court dismissed the appeal by the Australian Competition and Consumer Commission (ACCC) against Aurizon Holdings Limited (Aurizon) and Pacific National Pty Ltd (Pacific National).

On 14 August 2017, Aurizon announced its intention to exit its intermodal business by selling various assets to Pacific National. The ACCC opposed the sale and, as a result, some of the proposed arrangements were changed. However, the sale of the Acacia Ridge rail terminal remained a major issue. The dispute went to trial before the Federal Court where the judge found that the sale would have been illegal but for an undertaking for access to the terminal that the Pacific National produced towards the end of the trial.

The ACCC appealed this decision to the Full Court of the Federal Court. The Full Court dismissed the appeal. It found that that there was no need for the undertaking as a constraint, because barriers to entry were so high that entry in the future without the acquisition was no more than a ‘mere possibility.’ Frontier Economics advised the ACCC in their case prior to the trial and Philip Williams gave expert testimony at the trial.

Frontier Economics advises clients globally on transport and competition matters.

Four years ago, then Federal Senator Nick Xenophon and Frontier Economics jointly made the case in the mainstream press for the Reserve Bank of Australia (RBA) to end the fixation with inflation targeting and instead move to targeting nominal GDP. A Frontier Economics bulletin at the time explained nominal GDP targeting in more detail. Instead, the RBA continued on with its single minded approach. Not only did the RBA undershoot its inflation target over the ensuing period, it also presided over rising unemployment in the 12 months prior to the country being devastated with the COVID-19 pandemic.

Australia could have avoided much economic pain had it shifted its position on inflation targeting years ago. This shift away from inflation targeting is now being supported by others in a recent op-ed in the Australian Financial Review. Now is the time for the RBA to move on.