Frontier Economics' recently advised a number of clients in relation to the Queensland Competition Authority's review of its approach to climate change related expenditure. Below are some highlights and commentary on our advice included in the final position paper.

ensure its framework for assessing the prudency and efficiency of climate change related expenditure is fit-for-purpose and capable of incentivising timely investment when such expenditure would promote the long-term interests of consumers; and

provide greater clarity and certainty to stakeholders—including consumers and regulated businesses—on how the QCA intends to assess future proposals related to climate adaptation and mitigation expenditure.

Economic regulators need to perform a difficult balancing act when assessing expenditure proposals related to managing climate change risks. The impact of climate change on regulated infrastructure (and, therefore, on users of that infrastructure) is fraught with uncertainty.

If regulators set a low threshold for the prudency of climate change related expenditure, then consumers may pay more than the efficient amount required to manage climate change risks effectively.

Conversely, if regulators are too conservative in their assessment of climate change related expenditure, that may imperil the reliability and safety of the infrastructure used to deliver regulated services. This, in turn, may expose consumers to significant economic losses.

Uncertainty over whether regulators will approve climate change related expenditure—or over whether recovery of such expenditure would be disallowed once it has been incurred—may deter regulated businesses from making prudent and efficient investments to improve the resilience of their networks.

Clear guidance about how proposals for climate change related expenditure will be assessed by regulators can help reduce this uncertainty and encourage prudent and efficient investments that may otherwise be foregone.

For this reason, other economic regulators, should conduct their own reviews and publish formal guidelines on how they intend to assess regulatory proposals for climate change related expenditure. The QCA’s guidelines are not specific to any particular industry or jurisdiction, so would be a relevant starting point for other regulators and regulated businesses beyond Queensland.

Managing climate uncertainty to invest prudently and efficiently in resilience

Of the many issues covered by the QCA’s review, our advice focussed on the development of a framework to assess the prudency and efficiency of climate change adaptation expenditure.

Below are some highlights:

We advised Aurizon Network that:

“In assessing prudent and efficient ex ante resilience expenditure the QCA should encourage regulated entities to pragmatically incorporate the uncertainty inherent in climate change related risks into their proposals for adaptation expenditure.”

In our report to DBI, we added:

“Climate-resilience should be a necessary condition to project prudency and efficiency. Investing in infrastructure that is vulnerable, by design, to an accepted range of climate-related risks is likely to be lower cost in the short term but higher cost in total over the life of the asset.”

We discussed the development of an upfront expenditure framework that could facilitate investment under uncertainty, providing advantages to both regulated infrastructure providers and their customers. That is, a framework which:

is ex-ante in nature;

relies on the justification for the proposed expenditure;

includes in its ex-post review mechanisms a consideration of uncertainties related to climate-related risk; and

is proactive in managing long-term demand uncertainty.

We considered that these elements together would promote regulatory certainty and facilitate investment in prudent and efficient levels of infrastructure resilience.

The Coal Effect – funding and financing approaches to address residual stranding risk

Fossil fuel exposed firms are exposed to transition risk, or risks arising from the process of adjusting towards a lower-carbon economy. This can impact forecasted demand, the value of assets and liabilities, and thereby the risk profile and viability of the regulated business.

A key driver of transition risk for coal exposed companies is policy change. Net zero targets, can reduce domestic demand for coal. However, targets vary in status, development and expected achievement date. This uncertainty, in combination with uncertainty around technological development and carbon abatement costs, makes future demand for coal similarly unclear.

We identified a scenario where Aurizon Network may support more adaptation expenditure to increase the resilience of the network (with the expenditure to go into the regulatory asset base). However, future customers may be unwilling or unable to continue to pay for past adaptation expenditure. These factors create asset stranding risk, which may disincentivise a regulated business from investing in network resilience today, even if the investments are supported by current customers.

We then considered options the QCA might adopt to address asset stranding risk. We discussed the merits of addressing an increased stranding risk associated with climate change via an uplift to the allowed rate of return (i.e., the ‘fair bet’ approach) that would be just sufficient to compensate investors for the increase in stranding risk.

Also considered was the use of accelerated depreciation, which has been used by regulators in Western Australia (ERAWA) and New Zealand (the Commerce Commission) to address the stranding risks faced by gas pipelines following the adoption of emissions targets that have shortened the expected economic life of those regulated assets.

In our advice, we recommended that the QCA should confirm clearly that:

its regulatory framework will continue to provide regulated businesses with a realistic opportunity to recover past prudent and efficient expenditure over the long term;

regulatory allowances will be set such that climate change related expenditure that is deemed to be prudent and efficient, based on information available at the time, may be recovered over the expected economic life of the assets; and

the expected economic life of the assets should be reassessed periodically as new information becomes available.

Overall, we identified the benefits in the QCA providing clear upfront guidance on the types of information and evidence it would require from regulated businesses, to demonstrate asset stranding risks and management responses.

This could include the QCA needing to take into consideration a larger range of plausible future scenarios, rather than focusing on just the expected future profile of demand at a given point in time, reflecting the long-term uncertainty faced by the coal industry.

Frontier Economics Pty Ltd is a member of the Frontier Economics network, and is headquartered in Australia with a subsidiary company, Frontier Economics Pte Ltd in Singapore. Our fellow network member, Frontier Economics Ltd, is headquartered in the United Kingdom. The companies are independently owned, and legal commitments entered into by any one company do not impose any obligations on other companies in the network. All views expressed in this document are the views of Frontier Economics Pty Ltd.

Transition support for the NSW native forest sector

With the Victorian government announcing an end to native forest logging by 1 January 2024, we revisit a recent report prepared for WWF–Australia (World Wide Fund for Nature Australia) in August last year. In it, Rachel Lowry, Acting CEO, WWF–Australia explains, “This report was not commissioned to ignite or exacerbate ‘forestry wars’. Instead, it is designed to inform and motivate critical solution-focussed discussions, ideally led by the NSW Government.”

The New South Wales (NSW) native forest sector has been contracting over a long period as publicly provided wood supply has fallen to more sustainable levels. The 2019–20 Black Summer fires compounded this trend, significantly reducing sustainable wood supplies, particularly in the South Coast and Tumut regions. This shock to the sector, economy and regional communities – combined with an increased recognition of the significantly higher value that standing native forests offer in comparison to logging– provides an opportunity to reconsider the best use of NSW’s native forest resource. Other states including Victoria and Western Australia facing similar issues have made the decision to end the native forest logging.

In this context, Frontier Economics was engaged by WWF–Australia to consider options for the design of appropriate structural adjustment arrangements that would accompany a decision to end public native forest logging in NSW. Our Report, Transition support for the NSW native forest sector, outlines a design and cost estimate of such structural adjustment supports.

The financial return and economic contribution of public native forestry is small

Our Report found that Forestry Corporation of NSW’s (FCNSW’s) native forest logging business appears to offer poor financial returns to NSW taxpayers, with some parts of the hardwood business unlikely to be covering costs. The Independent Pricing and Regulatory Tribunal of NSW (IPART) has also reported on the loss-making activities of FCNSW’s hardwood division.

There is also clear evidence that that value of the native forest would be higher as a standing resource.

The volume of wood supplied by FCNSW’s native forest business has been falling, and is unlikely to return to historic levels of production given the current state of the native forest after the Black Summer fires and the increasing impacts of climate change.

Employment and economic contribution have also fallen to modest levels, even when both hardwood and softwood, and private and public industry in NSW is accounted for. Direct employment associated with FCNSW’s hardwood business is in the order of 1,070 across the State – including those employed by FCNSW, harvest/haulage contractors and mills.

Designing a comprehensive structural adjustment support package

A comprehensive structural adjustment package should accompany the decision to cease the remaining native forest logging activity by FCNSW. This package would support impacted employees, firms and communities during the transition.

Across jurisdictions, there is a broad consistency in the design of public native forest logging structural adjustment packages, including:

Support for workers through redundancy top-up payments and resources for retraining,

Support for harvest/haulage contractors and mills through capital redundancy payments,

Wood supply contract buy-backs, and

Longer term funding to diversify local regional economies.

Structural adjustment packages are also often complimented with longer term support for increased investment in plantation resources.

Alongside a package of structural adjustment support, our Report finds there are likely to be alternative employment opportunities for displaced workers from the public native forestry sector, particularly in management of protected forest areas, recreation and tourism, plantation-based forestry work, fire and invasive species management and the management of carbon and biodiversity credits.

The estimated cost of structural adjustment support

The estimated cost of the government-funded structural adjustment is $302 million in total. This includes:

Up front structural adjustment funding of $244 million. This covers payments to support worker redundancies and retraining, capital redundancies and Wood Supply Agreement (WSA) buy-backs, and

Structural adjustment funding for regional economic diversification of $58 million, spent over a 10-year period.

Our Report developed these estimates along similar lines to those adopted in other jurisdictions. It is assumed the adjustment package would be implemented from 2028- 29 once the majority of the current WSAs with processors have expired.

The cost of the structural adjustment package is likely to be readily outweighed by a range of positive budgetary impacts including:

Avoided ongoing structural adjustment and bushfire support to the hardwood sector,

Avoided equity injections to FCNSW, and

The likelihood of increased dividends from FCNSW over time by avoiding the loss-making activities of the hardwood division.

FCNSW and plantation investment

Complementing a structural adjustment support package, the NSW Government may invest in increased plantation resources. The Victorian and West Australian governments have announced funding for plantations of $110 million and $350 million, respectively.

Alternatively, FCNSW may consider the investment opportunity to expand its hardwood plantation estate in the expectation of a long-term financial return.

The forestry sector would sensibly lead any plantation expansion in NSW based on its understanding of the best locations, appropriate size of expansion, plantation species and market needs.

View the full report commissioned by WWF-Australia here.

The economics of water security in Australia’s hydrogen transition

Hydrogen gas has been hailed as the next big clean energy source, and Australia, with its abundance of renewable energy potential, is seen as well positioned to lead the charge to net zero. Governments and utilities are increasingly turning their focus to how the potentially large but uncertain water requirements to support Australia’s hydrogen transition can be met.

The quantity and variability of Australia’s water resources compared with other continents is well known, as are the expected reductions in average groundwater and surface water supplies available for consumption. The challenge for Governments and utilities is how to plan for and deliver water services to meet growth in underlying demand as well as potentially large but uncertain growth in industrial water demand – including to support Australia’s hydrogen transition.

In this context, it is critical that a sound economic framework is utilised to evaluate supply and demand side measures to meet potential growth in water demand, and provide efficient price signals to water users relating to the economic, social and environmental cost of water supply. This bulletin explores how integrating the economics of water security early in the hydrogen planning process can support informed decisions about how this transition occurs, including the location of hydrogen assets and their water sources, and ensure investment in water supply occurs when and where it maximises value to the community.

Australia’s hydrogen transition could have significant water requirements

Demand for ‘clean’ or ‘green’ hydrogen is expected to dramatically increase over the next decade as it replaces other hydrocarbon-based energy sources, such as liquid fuels for vehicles and natural gas for electricity generation and heating. Australia appears well placed to take advantage of increasing global momentum for clean hydrogen with big ambitions to grow our domestic hydrogen sector, with the “aim to position our industry as a major global player by 2030.”[1] Significant resourcing including state and private funding is being committed to support this ambition.

Year-round access to a secure source of water is critical for the delivery of Australia’s hydrogen transition. The National Hydrogen Strategy notes that water required for a large-scale hydrogen production industry will be significant. Given uncertainty around the future growth of Australia’s hydrogen sector, estimates of future water demand vary, ranging from just under the current annual supply for the whole of Southeast Queensland,[2] to around one-third of the water currently used by the Australian mining industry.[3] While the water demand is uncertain, in either scenario, it is potentially significant.

The National Hydrogen Strategy acknowledges that “Australians will want the new jobs and growth of clean hydrogen to be achieved without compromising safety, cost of living, water availability, access to land or environmental sustainability”.[4]

It notes that Australia will therefore need to consider how to balance hydrogen’s demands with other water priorities.[5] Some of which “may have higher economic, social or cultural value.” [6]

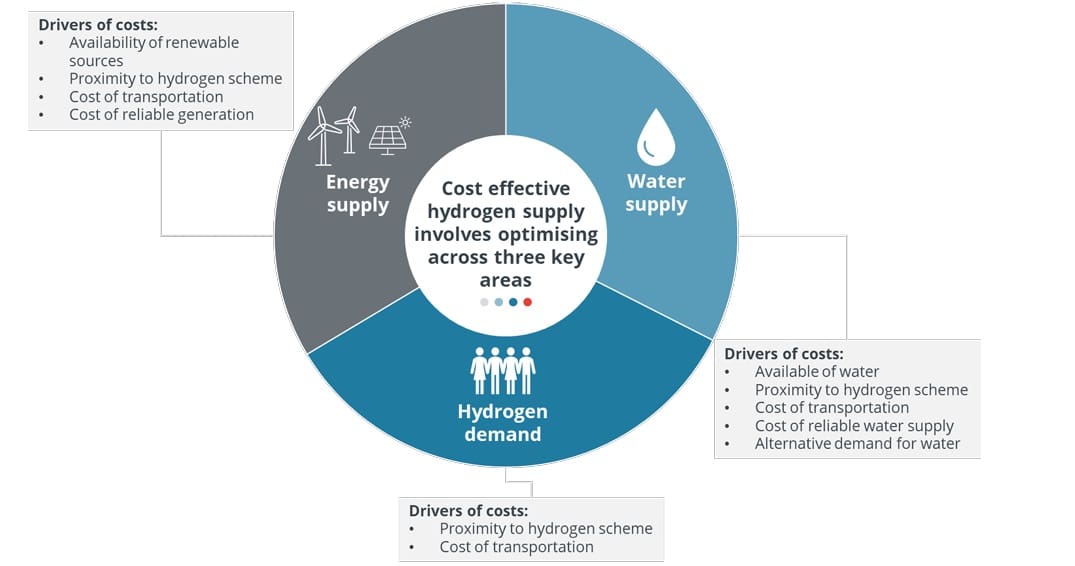

Delivering cost-effective hydrogen is likely to be a complex optimisation problem

The National Hydrogen Strategy states that “the most ideal sites for production facilities will have access to renewable electricity and water supplies”. [7]

Implicit within this is that there is a complex optimisation across numerous input and output/product markets – whether to transport energy, water and/or hydrogen.

For example, the Hunter Valley Hydrogen Hub on Koorangang Island was chosen as the location for a hydrogen hub based on its “proximity to high energy users, existing skilled workforce, existing energy infrastructure and land available for complementary businesses.”[8]

The Water Services Association of Australia states that: “For hydrogen production, 11% of Australia is suitable when considering energy needs only. This is reduced to only 3% when factoring water and transport infrastructure”.[9]

A key element when considering the cost of water in this optimisation is:

The financial cost of water supply which is driven by water availability and at what price;

Broader social, economic and cultural costs of accessing or transporting water;

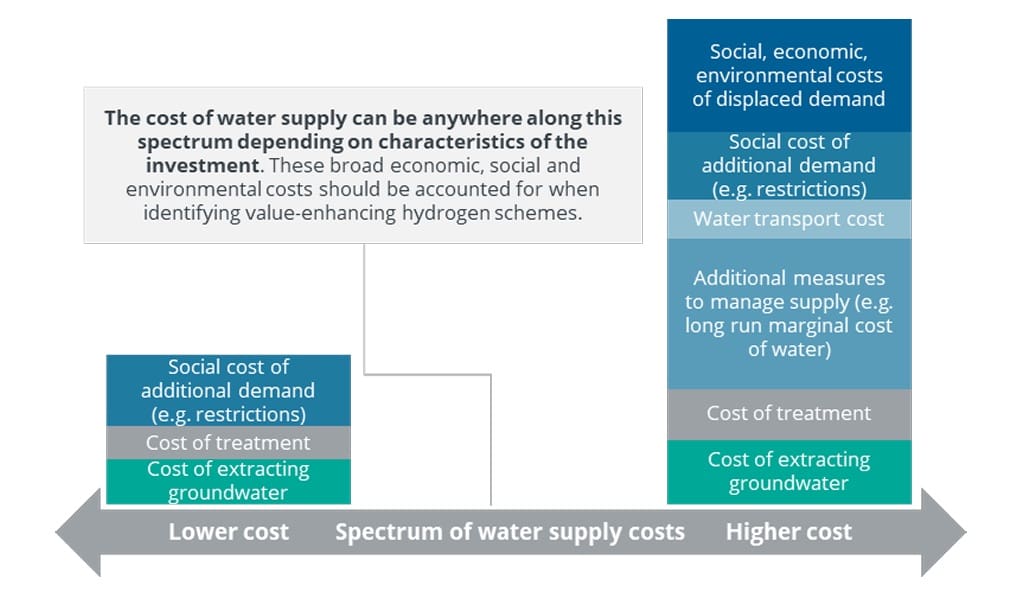

The costs of water supply are variable but in many places are already increasing

The challenges in providing water security in Australia are well known.

Australia has a highly variable climate and set of rainfall patterns. Changes to rainfall patterns, declining groundwater availability and changes to water allocation (in part related to increasing environmental considerations)—all increasingly exacerbated by climate change— are reducing the capacity of existing and primarily climate dependent systems to supply water to the community.

Alongside this, water demand particularly in many urban areas is expected to grow as result of population growth, increasing temperatures and evaporation rates and community expectations for irrigated ‘cool green’ communities.

For this reason, in many urban supply areas, water security is increasingly being met by climate independent sources of supply (such as desalination and recycling facilities) combined with water conservation and demand management. While often cost effective relative to investment in more traditional climate dependent sources (such as new dams), these measures are increasing water supply costs over time, reflected in higher water usage prices.[10] The era of low-cost water is over.

The National Hydrogen Strategy notes that other uses for water may have higher economic, social or cultural value.

However, the impact on availability of water and/or other users, will vary depending on site specific characteristics, such as the size of the hydrogen scheme, the supply and demand balance in the area and the other competing water uses.

In some cases, investment in a hydrogen scheme that displaces other water demand can deliver a net benefit to the community (i.e. where hydrogen displaces low-value demand).

Identifying and enabling investment in these value enhancing opportunities for hydrogen production requires identifying the range of economic, social and environmental costs and benefits of water supply.

In broad terms, in rural areas the cost will largely by the social and environmental costs of displacing current users. In metropolitan areas it could be the cost of measures to increase supply or where this is not possible, to manage demand.

Rural areas

Non-metropolitan areas are likely to be closer to the source of renewable energy and water supply, but further away from hydrogen demand (for example, export infrastructure).

In addition, while water licences can appear to be a relatively cheap source of water, without access to a high security access licence, water may not be available when it is needed.

In many rural regions, additional water supply options can be limited, which means that the cost of meeting the additional demand associated with the hydrogen scheme can be significant. Inland desalination can be prohibitively expensive, and many communities rely almost 100% on rainfall dependent water sources, which are becoming a less and less secure source of water.

In the instance where proponents can access a secure licence at a reasonable price, as most rural water systems are fully allocated, providing water to the hydrogen scheme is likely to displace current users, such as farmers and households.

This displacement of demand can generate a range of economic, social and environmental impacts and can present equity and socio-economic concerns, especially when the water is used to provide hydrogen for export to other countries.

Even in the instance where there are allocations available (the hydrogen scheme does not displace demand), at a minimum, the high reliability requirements of the hydrogen scheme would increase the risks and variability to other users.

This highlights the need for an economic model to help understand the socio-economic impacts of allocating water to a hydrogen scheme. This is similar to analysis that we undertook to help understand the impact of Basin Plan water recovery, that has significantly reduced water available to irrigators, industry and other water users, to improve environmental outcomes.[11]

Metropolitan areas

Alternatively, the hydrogen scheme could be located close to metropolitan areas, such as near Newcastle or Perth. This is likely to be located near the source of hydrogen demand (both domestic demand and export infrastructure for international demand) but can require transportation of the energy. It also presents unique water security challenges.

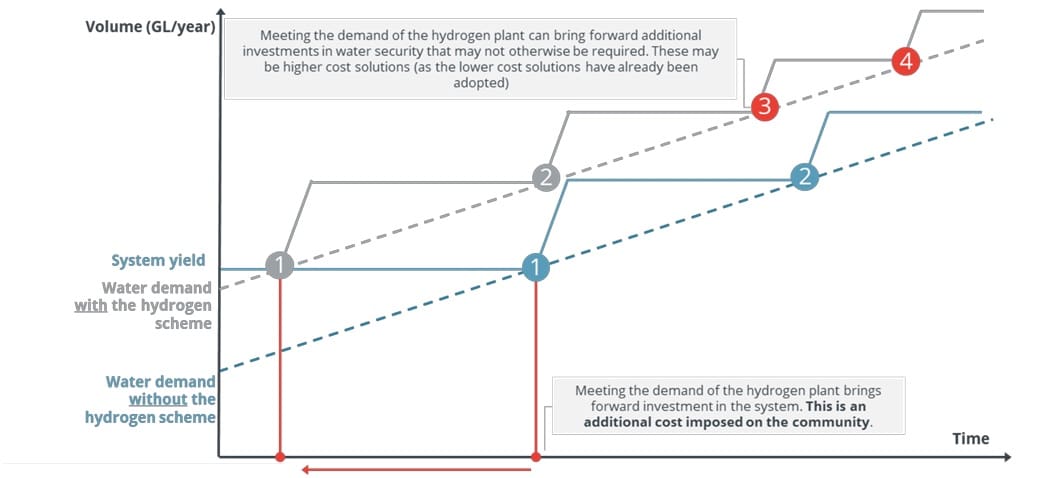

While connecting a hydrogen scheme to the existing water supply may seem like a simple solution (i.e. use what we already have), doing so will subject the plant to broader, complex water security rules, regulations and planning impacts, as a large customer in a bigger water supply system, which could have implications for secure hydrogen production (for example, hydrogen production may need to be subject to water restrictions).

As shown in the graphic below, connecting the hydrogen scheme to the existing water supply, is likely to bring forward investment by a number of years, and/or trigger additional investment, in water supply or demand measures. These additional measures often represent more costly water supply options, as the lower cost options, such as surface and groundwater, have been fully utilised. This means that even in the presence of cost reflective prices, water prices are likely to increase in future.

While wastewater recycling or stormwater harvesting are also possible options, recycling is not a costless source of water because there are competing uses for it. For example, any recycling supplied to a hydrogen plant, is recycling that cannot be used to meet other non-potable, and increasingly, potable, needs.[12] In other words, using recycling to meet demand is not necessarily a low economic cost option.

An alternative option that is regularly raised is the construction of a desalination or wastewater recycling scheme to directly supply a new hydrogen scheme. However, like other major industrial customers, it may be the case that these hydrogen schemes remain connected to the water supply grid (to allow potable ‘top-up’).

Even if the hydrogen plant itself is not subject to water restrictions, restricting other users water supply while maintaining supply to the hydrogen plant can, as above, present equity and socio-economic concerns. For example, should a desalination plant built to service a hydrogen plant be required to service the broader community during periods of extreme drought?

In every case mentioned above, water security planning must be undertaken in a way to appropriately manage the, albeit uncertain, hydrogen demand.

Regardless of the water supply option adopted, supplying water for hydrogen schemes is likely to add the cost of building more water supply infrastructure on top of several other investments in water security, wastewater and stormwater management that are already planned over the next thirty years.

This highlights the need to holistically plan across the water cycle and across various (competing) water demands, to identify and enable investment where and when hydrogen delivers a net benefit to the community.

A sound economic framework is critical to supporting Australia’s hydrogen transition

However, in many planning processes to date, there has been limited consideration of:

the additional water supply (or demand) measures that may be required to manage the potential for large but uncertain hydrogen related water requirements in addition to the existing supply and demand variables;

the impacts on the cost of supply and prices paid by all water customers resulting from the need for increasingly costly measures to manage water security.[13]

This may be because:

relative to other factors that drive grid supplied water demand, the hydrogen related component is either assumed to be small (as it could be directly supplied using purpose built desalinated seawater or wastewater facilities) or is highly uncertain and well off into the future – in terms of where and when it will occur, perhaps even at all.

there are opportunities to increase the overall availability of water supply for the community, including recycling and desalination.

However, without proactive planning and engagement – supported by a sound economic framework– there is a risk that:

a large-scale transition to hydrogen has the potential to exacerbate already competing demands for water resources (including wastewater and stormwater resources), particularly in regions that face significant water security challenges; and

potentiallyvalue enhancing opportunities for hydrogen production are foregone as a result of continued water use for low value activities.

These examples highlight that while the cost of water may appear to be a small proportion of the cost of a hydrogen scheme, there is a need to consider the site-specific value of hydrogen schemes, including any implications across the water cycle early in the planning process. This requires planning and collaboration across the hydrogen, energy and water sectors underpinned by:

An economic framework for understanding the broader economic, social and environmental costs and benefits of meeting the broad range of water demands, including the opportunity cost of water supply options. While groundwater or wastewater resources may seem a low-cost solution to providing water for hydrogen in some areas, consideration should be given to the impact on competing users and the opportunity cost of alternatives uses of these resources.

If the water or wastewater resource could be used by other users, meeting the demand of hydrogen schemes will bring forward investment in the broader water supply system, imposing costs on the community.

Planning that is adaptive and resilient under a range of risks and uncertainties. Depending on the location of hydrogen production some of supply costs may be incurred even if some of the hydrogen projects do not ultimately proceed, driven by the often large and lumpy investments required to provide water security. This suggests the need for decision-making to be aligned to adaptive planning processes, that is flexible to uncertainty, including climate change, uncertain demand and changing regulatory environments. Tools such as real options or adaptive pathways analysis enable decision-makers to understand the costs and benefits of resilient and adaptive decision making. This is similar to our analysis undertaken as part of the Lower Hunter Water Security Plan. [14]

Getting pricing right ensure that efficient signals are provided regarding the cost of water supply and ensure water use occurs when and where the benefits outweigh the costs. The absence of cost reflective pricing across many jurisdictions in Australia means these signals are not being provided to many users. This requires robust estimates of the cost of providing water, including estimates of long-run marginal costs of water and wastewater.

While these steps are not always easy and require collaboration across sectors and disciplines across the public and private sector (including engineers, planners, scientists and economists), they provide a robust framework to better identify, quantify, value and incorporate these costs and benefits into decisions.

To download this publication in full (including references), click the button below.DOWNLOAD FULL PUBLICATION

Frontier Economics and the Australian National University provided a comprehensive response.

Dr Venn has subsequently published a partial apology and amendment to his critique.

Building a business case to confidently manage climate-related risks and opportunities

Climate change impacts will continue to unfold across Australia with increasing severity in the years ahead. This will result in a set of complex and material financial implications for business. For Australian business to confidently rise to the challenge of systematically measuring, managing and mitigating risks and opportunities of climate change it will need a sound understanding of how climate change will most likely impact its finances. This Bulletin discusses Frontier Economics and Edge Environment’s approach to extending climate risk frameworks to build business cases for climate response against the inevitable, and potentially disorderly, climate transition ahead.

Australia is in the midst of cascading and compounding climate impacts

After centuries of relative climate stability, the world’s climate is changing. As average temperatures rise, acute hazards such as floods and fires and chronic hazards such as drought and sea level rise intensify. These hazards are categorised as the physical risks of climate change.

The frequency and severity of weather events in Australia is increasing and may further intensify as ecosystems are pushed beyond tipping points. Recent weather events in Australia such as the unprecedented rainfall and flooding in South-East Queensland, New South Wales and Victoria, extreme heat in Western Australia and the 2019–20 bushfires have resulted in highly significant financial losses for businesses and the communities they operate in.

Climate risk, however, remains an emerging discipline compared to other traditional risk areas. Climate risk management will necessarily grow in importance over coming years – recently, the Australian Prudential Regulation Authority (APRA) warned business around the need to prepare for “rapidly increasing expectations” on climate risk disclosure.

Against this backdrop, forward looking businesses are taking steps to understand, quantify and manage their climate risk exposures.The good news is we have the tools to address urban heat: integrated planning of our natural and built environment covering blue, green, and grey infrastructure.

TCFD is a lens to grapple with these risks

The Taskforce on Climate-related Financial Disclosures (TCFD) reporting framework has emerged as the global benchmark in climate risk reporting. It seeks to make businesses’ climate related disclosures comprehensive, consistent and transparent. TCFD enables effective investor analysis of a company’s demonstrated performance of incorporating climate related risks and opportunities into businesses’ risk management, strategic planning and decision making.

The TCFD was set up in 2017 by the Financial Stability Board – an international body of regulators, treasury officials and central banks – to provide voluntary recommendations on how business could voluntarily disclose the risks and opportunities from climate change (see Box 1).

Box 1: TCFD in brief

The purpose of TCFD is to provide a framework for organisations to make consistent and transparent climate-related financial disclosures. The TCFD framework document provides the following overview of the types of disclosures that it recommends:

Governance: Disclose the organisation’s governance around climate related risks and opportunities.

Strategy: Disclose the actual and potential impacts of climate-related risks and opportunities on the organisation’s businesses, strategy, and financial planning where such information is material.

Risk management: Disclose how the organisation identifies, assesses, and manages climate-related risks.

Metrics and targets: Disclose the metrics and targets used to assess and manage relevant climate-related risks and opportunities where such information is material.

It is recommended that the business provides its disclosures in their public annual reporting.

Source: Recommendations of the Task Force on Climate-related Financial Disclosures

Momentum in the market is growing and norms are being set

Since being first published in 2017, TCFD has been rapidly adopted by a broad range of organisations across the globe – the 2022 status report for TCFD points to TCFD “support” encompassing US$220 trillion of assets and US$26 trillion of combined company market capitalisation.

There is a trend towards mandating climate-related disclosures. Mandatory climate risk disclosures have been announced in jurisdictions including the UK, the EU, Hong Kong, Japan, Singapore and New Zealand. Significantly, the United States Securities and Exchange Commission has proposed rules to enhance climate-related risk disclosure drawing from the TCFD recommendations. Collectively, these actions will set norms and expectations for Australian businesses to develop their own disclosures.

In 2021 the New Zealand Government passed legislation mandating climate-related disclosures for around 200 financial entities. Further to impacting those covered by the introduction of this mandate, the move is widely expected to act as a catalyst for increased climate-related disclosures across businesses operating in the wider New Zealand economy.

Decision making under complexity needs tangible financial analysis

While TCFD is ultimately intended to support more informed capital allocation by investors, it can also be an important tool for organisations to respond to the risks and opportunities of climate change.

For an approach to inform practical decision making it needs to provide climate-related impacts in financial terms:

In the case of climate risks, the approach would allow for adaptation, mitigation and divestment intervention options to be directly compared to a “do nothing scenario”;

It would facilitate the valuation of climate-related opportunities, such as, product innovation, renewable energy generation, water recycling, resilient supply chains, and cost savings in energy or resource use; and

The approach will be flexible to recognise that risks and opportunities will vary depending on the region, market and industry that the business operates in.

Clearly this is a complex task, but it needn’t be daunting if we have the right tools and systematic approaches. Finding a solution requires assessing the changing climate exposure and vulnerabilities of an enterprise through time. A collaborative approach which brings together the key stakeholders across an enterprise provides the means to map the material climate impacts, their drivers and the likely financial consequences to the company. This collaborative approach also enables joint ownership of critical uncertainties to be addressed within business’ operations, financial reporting and data management. A structured approach is then required to cut through the uncertainty and deliver a clear path forward to adequately measure, manage and mitigate climate risks.

Frontier Economics and Edge Environment have partnered to combine our skills in financial analysis, ESG, risk management, climate science and sustainability to work through this complexity (see Box 2).

Box 2: Frontier Economics’ partnership with Edge Environment

Edge Environment and Frontier Economics have worked across a broad range of climate risk and resilience projects, mostly within the property, infrastructure and government sectors. Together, this partnership provides a unique opportunity to better understand both financial risks and opportunities of climate change for Australian and New Zealand businesses.

Edge is a specialist sustainability services company focused on Asia-Pacific and the Americas. Its teams are based in Australia, New Zealand, the United States and Chile. Edge exists to help its clients create value from tackling one of world’s most fundamental challenges: creating truly sustainable economies and societies. Edge does this by combining science, strategy and storytelling in a way that gives clients the confidence to take ambitious action, and do well by doing good.

Source: Frontier Economics

A collaborative approach is required to address this complexity

Confident climate-risk decision making requires a multi-disciplinary approach, incorporating climate science and financial analysis. However, deep technical expertise alone is not sufficient.

There is also a need for broad buy-in and engagement from within and across an organisation in order to access information, form granular insights, identify key operational climate-related impacts and quantify financial consequence. Organisations are encouraged to systematically look beyond the acute and direct impact of extreme events but also to the aggregated impacts of chronic and indirect effects of climate extremes.

Even with all these elements, it can be difficult to know where to start a climate-related financial analysis.

Frontier Economics and Edge have developed a practical approach

A useful starting point in analysing climate-related risk and opportunities is to assess the impacts of recent extreme climate events – such as the Eastern Australia bushfires and drought of 2019-20 and the extreme rainfall of 2021-22 – on a business’ operations and related cashflows.

This “looking back to look forwards” approach provides multiple advantages. It allows the:

development of logic maps, from climate drivers to asset and operational impacts;

identification of related notional financial consequences; and

engagement from across the business on climate-related risks and opportunities.

Shared understanding of the constraints and limitations in financial data management which may need to be addressed to enable the aggregated costs of climate impacts to be assessed with confidence

The logic mapping and notional financial consequences can then be tested and validated using actual operational and financial data to identify the impacts of recent extreme events.

This approach also clearly highlights any data gaps which limit the extent to which financial consequences can be isolated – providing insight to improve risk management systems.

This baseline analysis has standalone value as it provides a snapshot of the resilience of an organisation to recent climate change events which can be linked back to materiality thresholds in a firm’s enterprise risk framework. It is also vital in building a foundation for robust and defensible scenario analyses of the likely impacts of future climate extremes on an enterprise. It can be used to inform forward looking analysis of climate change impacts, which considers both cash flow and asset valuation risks and opportunities.

The approach taken by Frontier Economics and Edge Environment focusses on undertaking robust, transparent and actionable analysis. For example, we focus first on the short-term (to 2025) before extending analyses further into the future. A short-term lens reduces uncertainty and allows organisations to home in on impacts which require urgent action. It also allows for extensions such as cost-benefit analysis to support investment decisions around certain interventions.

Building the business case to confidently make decisions about managing your organisations climate risk is a journey – come and talk to us about getting started.

In September 1990, Scientific American published a special issue entitled ‘Energy for Planet Earth’. In this publication, Scientific American explored the sources of energy, the future for energy, made predictions on technological breakthroughs and suggested solutions for what they considered was an imminent energy crisis.

Many of these predictions by Scientific American were made for 2020. Given we have reached that date, we can look back and compare the predictions with what actually happened. In a three-part series, Frontier Economics compares actual outcomes to 2020 with the predictions made by Scientific American.

This comparison of actual versus predicted outcomes, especially where technological change is involved, can help us learn about the factors that have been determinative to the global community and provide guidance on how we can improve economic forecasts.

We focus on three areas where Scientific American made long term forecasts:

This is the third and final part of this series, examining the performance of Scientific American’s forecasts of emissions intensity.

Scientific American gets it right in Parts One and Two

In Part One - Energy demand we reviewed the performance of Scientific American’s long-term forecasts on primary energy demand. We found that, overall, Scientific American’s forecast was reasonably accurate. However, Scientific American did not perform as well on the growth performance by country. Most significantly, Scientific America materially underestimated the rapid and large increase in the growth of developing nations, such as China and India. That is, countries that were relatively poor in 1990 grew more quickly than expected, and they used energy to achieve this growth.

In Part Two - Energy intensity we reviewed the performance of Scientific American’s forecast of energy intensity. While Scientific American’s original historical depiction of energy intensity was stylised, it did accurately convey the historic profile of energy intensity – rising as countries develop, and then falling as economies mature. Given the size of the populations in developing countries in 1990, there was a genuine concern about the impact on energy demand (and resulting environmental problems) if these countries followed the same energy intensity profile as developed countries. However, Reddy and Goldemberg predicted that developing countries would benefit from improvements in materials science and energy efficiency innovations from developed nations. This technological transfer would avoid the high energy intensity peaks that occurred over the course of the previous 150 years of economic development of, now, developed economies. Reddy and Goldemberg were correct. The energy intensity of developing countries, while starting on the higher side of developed countries in 1990, quickly fell as they adopted the latest technologies. By 2015, developing countries had lower energy intensity than the developed countries originally analysed by Reddy and Goldemberg. In fact, by 2015, developing countries exceeded the most ambitious energy intensity decline forecast by Reddy and Goldemberg.

We conclude our three-part series by looking at Scientific America’s global projections for CO2 emissions from fossil fuels.

In September 1990, Scientific American published a special issue entitled ‘Energy for Planet Earth’. In this publication, Scientific American explored the sources of energy, the future for energy, made predictions on technological breakthroughs and suggested solutions for what they considered was an imminent energy crisis.

Many of these predictions by Scientific American were made for 2020. Given we have reached that date, we can look back and compare the predictions with what actually happened. In a three-part series, Frontier Economics will compare actual outcomes to 2020 with the predictions made by Scientific American.

This comparison of actual versus predicted outcomes, especially where technological change is involved, can help us learn about the factors that have been determinative to the global community and provide guidance on how we can improve economic forecasts.

We focus on three areas where Scientific American made long term forecasts:

Each of these is the subject of a separate note. This note examines the performance of Scientific American’s forecasts of energy intensity.

Scientific American gets it right in Part One

In Part One we reviewed the performance of Scientific American’s long-term forecasts on primary Energy Demand. We found that, overall, Scientific American’s forecast was reasonably accurate. However, Scientific American did not perform as well on the growth performance by country. Most significantly, Scientific America materially underestimated the rapid and large increase in the growth of developing nations, such as China and India. That is, countries that were relatively poor in 1990 grew more quickly than expected, and they used energy to achieve this growth.

In this second part of our three-part series, we assess the performance of Scientific American’s forecast of energy intensity.

To view the full report, download the publication via the button below.

The Australian Gas Industry Trust (AGIT) and Jemena have published a study undertaken by Frontier Economics on The role of gas in the transition to net-zero power generation. Our study was commissioned by AGIT and Jemena to understand the changing role that gas generation plays in today’s electricity markets, and how that role will continue to evolve as electricity markets transition to net-zero emissions.

Our study found that the requirement for flexible generation will continue to increase as the penetration of intermittent renewable generation increases and that gas generation will have an important ongoing role to play. These findings are consistent with what we observe in electricity markets around the world, including markets with a bigger share of intermittent renewable generation than Australia. In these markets, gas generation continues to play an important role by providing generation capacity that is both firm and flexible.

The NSW Government has recently announced a target of reducing the state’s emissions by 50% by 2030 on 2005 levels. Meeting this target while driving increased prosperity requires the realisation of the cheapest sources of abatement.

Consistent with this commitment, there is an opportunity to expand the role of forests in NSW’s climate strategy by stopping logging in state forests. Frontier Economics and Professor Andrew Macintosh of the Australian National University have prepared a report, Comparing the value of alternative uses of native forests in Southern NSW, that looks at the climate and economic outcomes of this strategy, based on a case study in the southern forests of NSW, covering the Southern and Eden Regional Forest Agreement (RFA) areas.

Based on conservative assumptions, the study found stopping native forestry in the Southern and Eden RFA areas would produce a net economic benefit to the state of approximately $60 million, while also reducing net greenhouse gas emissions by almost 1 million tonnes (Mt) per year over the period 2022-2041.

Once thought of as purely an environmental issue, climate change is now recognised as a major threat to economies and financial markets around the world. As a result, public and private sector organisations are being asked to provide public disclosures of how current and future climate risks will impact their operations.

Recognising the increased need for climate change impact reporting with a greater focus on financial analysis, Frontier Economics and sustainability services consultancy Edge Environment are very excited to be partnering with each other to offer clients advice that combines in-depth environmental expertise underpinned by solid economic analysis and modelling.

“The requirements for climate disclosure reporting have been increasing around the world in recent years. We have seen climate change shift from being primary an environmental or “green” issue to one with legal, governance and financial implications” said Dr Mark Siebentritt, Edge’s Commercial Director and one of its climate risk analysis experts.

“We are seeing many of our clients step up their analysis of climate risk. This is in response to commentary by financial regulators in Australia about the need for companies to address what is now regarded as a foreseeable and material risk. Change is also coming through international markets with some countries like England and New Zealand headed toward mandatory climate risk disclosure reporting.”

One of the key challenges of climate risk disclosure reporting aligned to frameworks like the Taskforce on Climate Related Financial Disclosures (TCFD), is the need to better understand the financial implications of climate change.

“The impacts of climate change on the financial statements of an organisation is complex. Companies can find it challenging to do this as there are many drivers that need consideration. For example, take the impact of extreme heat on a property portfolio. You first need to understand the risk of such extreme weather in different climate change scenarios. Then you need to understand the physical impacts of extreme heat, this may include increased energy costs, damage to the property and even consideration of whether the property is unhospitable in extreme heat. Finally, you need to place a financial value on these physical impacts. Climate risk specialists and financial experts working together can give companies these insights” said Ben Mason, economist at Frontier Economics.

“A key risk companies are often interested in is around energy supply transitioning to renewables and the impacts on energy prices. We have energy network models and have provided shadow carbon price advice to various clients.”

Building on our expertise in TCFD reporting, Frontier Economics is expanding into ESG related advice more broadly. Ensuring decisions are based on sound and rigorous economics is critical for companies navigating this complex area.

Background

Edge Environment and Frontier Economics have worked across a broad range of climate risk projects, including within the property, infrastructure and government sectors. Together, this partnership provides a unique opportunity to better understand both financial risks and opportunities for Australian and New Zealand businesses.

About Edge Environment

Edge is a specialist sustainability advisory company focused on Asia-Pacific and the Americas. Its teams are based in Australia, New Zealand, the United States and Chile. Edge exists to help its clients create value from tackling one of world’s most fundamental challenges: creating truly sustainable economies and societies. Edge does this by combining science, strategy and storytelling in a way that gives our clients the confidence to take ambitious action, and do well by doing good.

About Frontier Economics

For more than twenty years, Frontier Economics has contributed sound economics to many important debates and decisions in Australia, New Zealand and the Asia-Pacific. Governments, regulators and businesses use our economic advice to inform policy development, market design, regulation and investment. Frontier Economics prides itself on delivering quality, independent economic input that can lead to better decisions and better outcomes for our clients.

We use cookies to ensure that we give you the best experience on our website. By continuing on this site, you are agreeing to our use of cookies.OKPrivacy policy