The Australian offices of Frontier Economics will be closed from 5pm Monday 24 December 2018 and will re-open at 9am on Wednesday 2 January 2019.

The Singapore office of Frontier Economics will be closed for the public holidays of Tuesday 25 December 2018 and Tuesday 1 January 2019.

We wish you all a Merry Christmas and hope you enjoy the festivities of the holiday season.

For more information, please contact:

Contact Us

The Australian Energy Council (AEC) published a report prepared by Frontier Economics consultant, Rajat Sood, on the impact of a range of changes to electricity technology, market architecture and supporting infrastructure on the structure and competitiveness of the NEM.

The report found that these developments are likely to:

- Help smooth wholesale price volatility in both the short term and in the medium to longer term

- Reduce the advantages of the vertically-integrated ‘gentailer’ business model and

- Encourage more competitive behaviour in the NEM wholesale market, leading to more efficient and cost-reflective dispatch and pricing outcomes.

Accordingly, these changes should address many of the concerns that have recently been raised by policy-makers and regulators about competition in the wholesale market and hence avoid the need for the policy and regulatory changes presently being considered.

The report is available on the AEC website.

For more information, please contact:

Contact Us

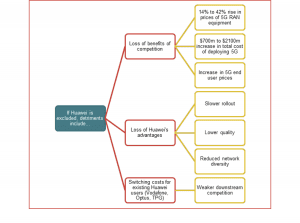

In August 2018, the Australian Government determined that Huawei would not be allowed to participate in procurements to supply 5G network equipment to Australia’s mobile network operators.

Prior to this decision, Frontier Economics was engaged by Huawei to consider the economic impact of excluding Huawei from these procurements.

We found that the cost to industry and consumers of reduced competition from excluding Huawei will be high. We estimate that the exclusion of Huawei will increase the cost of 5G radio access network (RAN) deployment in Australia by up to (AUD) $2.1 billion, which will be recovered from consumers through higher retail prices. Further, for networks already using Huawei for 3G and 4G equipment, additional switching costs could add several billion dollars and materially delay 5G deployments.

Competition drives consumer benefits

Competition between Australia’s mobile network operators has produced a vibrant and dynamic market for mobile services. Prices for mobile phone services have fallen by an average of 4.2 per cent annually since 1997–98, while Australia ranks in the top 5 in the OECD for mobile penetration. The exceptional outcomes for Australian mobile users have been underpinned by competition between global equipment vendors to supply network equipment – through the various generations of mobile services.

While competition in the global market for supplying radio access network (RAN) equipment is intense, the market is highly concentrated, comprising three large equipment makers (Huawei, Nokia and Ericsson), and a smaller competitive fringe. This is because the scale of R&D spending required to continually improve performance is very large – globally, Huawei spent almost USD$12 billion on R&D in 2016/17 (substantially more than both Nokia, approximately USD$5.6 billion, and Ericsson, approximately USD$3.8 billion (USD).

Excluding Huawei or other vendors will lessen competition and create other detriments

Competition between network equipment vendors produces lower equipment prices, better quality and, ultimately, better services for end users.

Excluding Huawei - or other vendors - from the supply chain would create very material risks of uncompetitive procurements for Australian networks. The concentrated market means there are few alternative vendors with the necessary expertise and scale to provide 5G network equipment. This reduction in competition would substantially increase network procurement costs and retail prices, to the disadvantage of Australian consumers.

There would also be other costs from excluding Huawei. This includes the loss of its particular quality attributes, and additional switching costs for mobile networks that have to change vendors where Huawei has been a key supplier. The detriments are summarised in the figure below.

Detriments arising from excluding Huawei from Australia's 5g network deployment

For more information, please contact:

Contact Us

A gap remains between Federal Coalition Government and Federal Labor ambitions for emissions reductions. Labor is attempting to bridge the divide (or wedge the Government) by adopting the mechanism that the Government developed and then abandoned: the National Energy Guarantee (NEG). We project that Labor’s 45% emissions reduction target will result in prices that are about the same as the Federal Government’s current policy of achieving an emissions reduction of 26% by 2030. Importantly, we also find that the Government’s costly Snowy 2.0 proposal does not deliver any price or emissions benefit. It is a waste of money.DOWNLOAD FULL PUBLICATION

Voodoo Economics gets a run

The post-GFC period has witnessed the emergence of a new 'school' of heterodox macroeconomic thinking known as Modern Monetary Theory, or 'MMT'. While conventional macroeconomics has focused on refining existing policy frameworks to better account for recent experience and contemporary conditions, MMT purports to overturn the conventional wisdom altogether. While it offers a seemingly irresistible intuitive appeal, MMT unfortunately has little to offer that is new or helpful to policy-makers and much that is harmful.

To access the briefing, click below.

DOWNLOAD FULL PUBLICATION

On Wednesday 7 November 2018, Frontier Economics is co-hosting a seminar with the Melbourne School of Government at the University of Melbourne. Gus O'Donnell, Chairman of Frontier Economics Ltd (our sister company headquartered in the UK) will be presenting a public seminar on "Changing Behaviour in the Public and Private Sectors".

This seminar looks at the challenges in applying behavioural insights to alter behaviour in both the public and private sectors.

Gus O'Donnell served three Prime Ministers as the UK’s Cabinet Secretary and head of the British Civil Service between 2005 and 2011. After stepping down as Cabinet Secretary, he was made a life peer of the House of Lords. He has held senior roles at the UK Treasury (including as Permanent Secretary of the Treasury between 2002 and 2005), the British Embassy in Washington, International Monetary Fund and the World Bank. Before joining the British Civil Service in 1979, Gus was a lecturer in economics at the University of Glasgow. He has written and spoken extensively on the use of behavioural economics in policymaking.

Date: Wednesday 7 November

Time: 1.00 - 2.15 pm, followed by light lunch

Venue: Terrace Lounge, Melbourne School of Government, Walter Boas Building

Enquiries: msog-events@unimelb.edu.au

For more information, please contact:

Contact Us

In 2018, the Productivity Commission has been examining airports regulation in Australia. The inquiry, the third since the move to a price monitoring framework in 2002, has attracted submissions from airports, airlines, other airport users and other regulators. There were 68 initial submissions made to the inquiry.

Frontier Economics prepared submissions on behalf of Airlines for Australia and New Zealand, and for Australian Finance Industry Association (on behalf of car rental operators). Our submissions covered market power, airport profitability, the costs and benefits of regulatory reform and weaknesses in the existing regime (including the impact of changes in the Part IIIA National Access Regime).

We have also reviewed the Australian Competition and Consumer Commission's (ACCC) submission with interest. As the long-time monitor of airports’ conduct, its submission is likely to hold particular weight.

Frontier Economics comments on the ACCC submission

The ACCC’s submission to the Productivity Commission’s 2018 review of airports regulation was recently published.

As the long-term monitor of the four major Australian international airports (Sydney, Melbourne, Brisbane and Perth), the ACCC’s submission might be expected to hold significant weight for the review. Given its monitoring role, the ACCC’s submission can draw on a substantial body of evidence relating to its monitoring activities. However, the submission is also an opportunity for the ACCC to submit on the merits of the regulatory regime.

The ACCC’s overall message is largely unchanged from 2011. In fact, even the media release headlines are all but identical! (“Effective airport regulation needed”).

The ACCC’s reasoning is that monitoring of airports has not proved to be an effective constraint on market power. Nor is Part IIIA an effective constraint on airports’ behaviour, particularly given the recent amendment to criterion (a) that has raised the declaration threshold. As an alternative, the ACCC argues that a negotiate-arbitrate model for aeronautical services would deliver better outcomes – at least for the airlines.

Aside from its recommendations on the overall effectiveness of the regime, there are two parts of the submission which caught our attention; what the ACCC said about monitoring, and what form of regulation should apply to non-aeronautical services.

On monitoring, the ACCC submission maintains its position that it cannot readily use monitoring data to assess profits and whether the airports have exercised their market power. In other words, the ACCC believes that airports have exercised market power (hence the call for effective regulation), but primarily supports this call with a structural analysis of market power rather than direct evidence of excessive profits. In part, this seems to be because it is directed to monitor the aeronautical activities of the airports and the reported returns on the value of airport aeronautical assets are not obviously high (for example, at Figure 3.5).

- In the context of the Productivity Commission review, even though its monitoring data is limited, our view is that the ACCC could do more with the data it has to estimate the degree to which different airports have exercised market power. The ACCC (rightly) notes the limitations of using accounting data to estimate economic returns, associated with the exercise of market power. This is particularly so given past asset revaluations which have deflated observed returns. However, the ACCC holds detailed information on cash flows that covers up to 20 years for the monitored airports. These can be used to derive rates of return across the airport’s operations – not just limited to aeronautical activities. To the extent that high airport returns are ‘hidden’ in non-aeronautical services, it might have been useful to have brought that out.

- To take an example of how the data can be used: Melbourne Airport’s assets were valued by purchasers at a little over $1.25 billion at sale in 1998, and the current reported value of assets (2016-17) is a little over $5 billion. Calculating the economic (internal) rate of return using cash flows and those opening and closing values indicates a return to owners of over 14% (calculated on a pre-tax, nominal basis).

- The ACCC’s monitoring data does not estimate what a reasonable rate of return on assets would be for the monitored airports. An analysis of profits must take into account a benchmark return reflecting the risk associated with investing in the business. Estimating a cost of capital is controversial, but it remains unclear why the ACCC’s monitoring does not include benchmark returns.

On non-aeronautical activities, the ACCC does not consider more regulation would be justified. This is notwithstanding that the ACCC also believes monitored airports have market power over these services, and have used it (see page 44). The ACCC supports monitoring and that advising consumers of different options might be a better approach. In our view, this sits somewhat uncomfortably with earlier suggestions that monitoring has not effectively constrained behaviour.

This comment is available as a PDF.

For more information, please contact:

Contact Us

Philip Williams, Frontier Economics, presented at the Federal Court Judges Competition Law Conference today. Philip's paper examines the relevance of economic efficiency to the new language in s46. He puts forward two propositions.

- The first is that there is a long history of recognising that one aspect of competition in the context of competition law is a notion of socially useful competition.

- The second proposition is that this notion of socially useful competition is particularly relevant to monopolisation cases of the kinds that will appear under our new s 46.

Philip leads the legal and competition practice at Frontier Economics.

For more information, please contact:

Contact Us

The Australian Competition and Consumer Commission (ACCC) announced today that it has cleared two proposed acquisitions in the out-of-home advertising sector: the acquisition of APN Outdoor Group Limited by JCDecaux SA and the proposed acquisition of Adshel Street Furniture Pty Ltd by oOh!media Limited.

All four companies provide outdoor advertising, however there were crucial differences between the type of outdoor advertising. Frontier Economics (Asia-Pacific) was retained by lawyers for JCDecaux to provide economic advice. The operations of JCDecaux were essentially restricted to small format street furniture, a segment in which APN Outdoor had no presence. As a consequence, there had been limited competition between the two parties, both in the supply of outdoor advertising and the acquisition of sites. Similarly, Adshel and oOh!media operated in complementary segments. The absence of competition between the merging parties led the ACCC to conclude that “neither of the proposed deals is likely to substantially lessen competition”.

Frontier Economics regularly undertakes empirical analysis for clients in competition matters.

For more information, please contact:

Contact Us

Chief Scientist Alan Finkel reached into Stalin’s drawer of economic planning tools many times when he made recommendations to the state about how to improve the power system. Like collectivism, in practice, Finkel’s recommendations do not seem to be going well.

One of Finkel’s signature recommendations was the development of an integrated grid plan “..to facilitate the efficient development and connection of renewable energy zones across the National Electricity Market”. The Australian Energy Market Operator (AEMO) renamed Finkel’s integrated grid plan the Integrated System Plan (ISP). AEMO states that its “… first ISP delivers a strategic infrastructure development plan, based on sound engineering and economics”, the latter part of this quote being a favourite energy mantra of Prime Minister Malcolm Turnbull.

No doubt Finkel had in mind that such a plan could be useful for policy makers if it was undertaken professionally and free of politics. AEMO states that its ISP is “a cost-based engineering optimisation plan” and that the ISP modelling “applied technology-neutral analysis to identify the required level and likely fuel type of supply investments required to meet future needs.” (AEMO, Integrated System Plan, July 2018, page 3.)

However, the modelling undertaken for the ISP requires the exercise of judgement, and there are some areas in which this judgement appears to be made to support certain conclusions. This note highlights several modelling and forecasting assumptions, that are hard to justify on an objective basis, which have skewed the final results. This raises serious questions about the usefulness of the ISP for policy makers and about the independence of AEMO itself.

Fuel prices

Between AEMO’s original release of its ISP modelling assumptions (in March 2018) and its release of the modelling results in the ISP report (in July 2018), AEMO substantially increased its assumed long-term coal price forecast:

- AEMO’s initial assumptions had a coal price for new generation in NSW and QLD that averaged $2.01/GJ during the 2020s and 2030s.

- AEMO’s final modelling had a coal price for new generation that averaged $3.77/GJ during the 2020s and 2030s.

- This reflects an increase of almost 90%.

No other fuel prices were updated during this time.

AEMO states that these updates were to reflect the coal price forecasts from the Department of Industry’s June 2018 release of its Resources and Energy Quarterly report. But the long-term coal price forecast from this report was only 5% higher than the equivalent forecast from the December 2017 release of the report. This doesn’t seem to justify a 90% increase in assumed coal prices.

Were these coal price assumptions updated to ensure that no new coal plant was part of the future generation mix in the ISP?

In the same Resources and Energy Quarterly reports from the Department of Industry, the long-term gas price forecast increased by 10-15% between the December 2017 report and the December 2018 report. Given that the Department of Industry made a larger upward revision to gas price forecasts than coal price forecasts, why did AEMO not update its assumed gas price forecast at the same time that it updated its assumed coal price?

Emissions trajectory

The emissions trajectory modelled in the ISP is the trajectory to meet a 28% reduction in carbon emissions on 2005 levels by 2030 (consistent with the Paris agreement). Beyond 2030, the ISP models an acceleration of the emissions reduction trajectory to achieve a 70% reduction in 2005 levels by 2050.

This accelerated target is not current policy. Was this emissions trajectory chosen to ensure that the future generation mix is in the ISP is made up almost solely of renewable and storage?

Implications

In a future in which coal prices are not as high as AEMO forecast, and the emissions reduction trajectory beyond 2030 does not accelerate as AEMO has assumed, is investment in coal part of the least cost mix of new generation? Did AEMO model its original, lower, coal prices while developing the ISP?

What are the implications of this for the views AEMO put forward in the ISP? Would there be less investment in renewables? Would there be less need for development of transmission investment to support renewable energy zones?

For more information, please contact:

Contact Us