Efficient Pricing Structures For NGN Access Services

The Australian Government has commenced the roll-out of a national wholesale-only high-speed broadband access network, and is considering the regulatory arrangements that should apply to this network. In this bulletin we draw on economic theory and outcomes in competitive markets to provide some thoughts on the challenges facing regulators and next generation fixed access network (NGN) operators in structuring wholesale customer access charges.

NGNs will enable the simultaneous delivery of quality voice, high-speed data, video and television services to end customers, and potentially open up a range of new applications using these services. But they will be expensive to build, and the focus of debate so far in Australia has been how to ensure that services provided over its NGN are affordable. The role of price structure in maximising take-up and efficient utilisation of NGNs has been largely overlooked. However, it is significant: poorly designed and inflexible price structures could prevent an NGN investment from delivering on its promises.

What considerations might be relevant for designing the structure of prices for an NGN? The most obvious feature of NGNs is that their physical costs of construction are colossal (the Australian Government has estimated A$43 billion for its NGN), and these do not vary greatly with either take-up or usage of the NGN. This means that regardless of whether the take-up of services is 20% or 80% of premises passed, and whether the average consumer usage is high or low, the total cost of the NGN will be broadly the same.

On the surface, a simple response to this cost feature of a NGN might be to charge a price for wholesale access to the ‘last mile’ of the network that reflects the capacity sought, and not the usage of that capacity. For example, the NGN operator could set a monthly charge per unit of capacity required (rather than the current trend of charging for usage in the form of data downloaded). This charge would apply for access to each end customer connected. Reflecting that average infrastructure costs per customer also vary by factors such customer density and distance, one might expect some granularity in capacity charges to reflect these features as well.

Such a pricing structure for NGN wholesale access seems intuitively appealing for two reasons. First, it accords with how NGN costs will be incurred. Second, as usage charges would be minimised, it should encourage maximum usage of the network – critical to ensuring that the social benefits of widespread broadband adoption are achieved. However, two closely related questions that need to be asked about it are: is such a structure necessarily economically efficient; and is it a structure that a competitive market for NGN access services would likely arrive at? These questions are explored in turn below.

ECONOMIC THEORY

Economic theory tells us that in perfectly competitive markets with marginal costs that increase with output, economic efficiency is achieved as firms will set prices equal to marginal cost. This kind of pricing model is problematic in the NGN (and broader communications) access pricing context, because the market in which the NGN will operate will be far from perfectly competitive. An NGN is better characterised as a natural monopoly service with large fixed and common costs and average costs that fall with the level of output. This means an efficient pricing structure must take account of the need for the NGN provider to charge something more than its marginal costs (net of any public subsidy).

The conventional economic answer to this pricing problem is the use of ‘multi-part’ tariffs. The price of wholesale access would consist of a fixed fee independent from consumption, and a usage charge per unit of consumption. The levels of these tariff components will be governed chiefly by factors including the responsiveness of demand for access and usage to changes in their respective prices, and the responsiveness of the demands of each of these services to the prices of the other.

This simple answer overlooks at least two further pricing issues that might give the NGN operator cause for concern. The first is ensuring that prices capture ‘network effects’. These effects may justify pricing to some users at ‘below cost’. This could be efficient if there are benefits gained by other users from connecting new users, and part of this can be appropriated by the NGN operator.

The second issue is the social issue of promoting equitable access to broadband. This will be particularly pertinent if the government – as in Australia – finances much of the construction cost. High fixed charges may well deter take-up in locations that are expensive to serve, or by lower socio-economic groups.

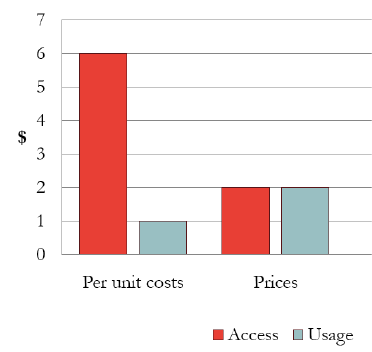

What is clear from economic theory is that the structure of prices will only be closely tied to cost causation under very strict conditions. Other structures could well be more efficient and more equitable. The figure to the right illustrates an example of that kind of pricing outcome. It shows a case where usage prices are marked-up to help recover the losses on the pricing of access. At four units of usage and one unit of access, the NGN operator will just recover its costs – and take-up may well be higher.

OBSERVED MARKET OUTCOMES

The mobile communications market provides a particularly good example of how firms can adapt pricing structures to reflect complexity on both the supply and demand sides. Mobile services charges commonly comprise both fixed and usage charges, as predicted by the basic economic theory, but these have evolved in interesting ways. Until recently, it had been very common for the fixed costs of access, such as the handset, to be primarily recovered through call charges, even though the cost of the handset is unrelated to usage. However more recently, fixed subscription pricing (in the form of monthly minimum but capped spends) has become a key feature of pricing plans that tend to diminish the role of usage charges as a means of recovering handset and other fixed costs of access.

Innovative forms of pricing are also common in other industries where consumers are sensitive to high up-front charges. A good example is the partial recovery of the cost of printers in the price of printer-specific ink cartridges.

These examples illustrate that reasonably competitive unregulated markets do in fact come up with pricing structures that reflect evolving consumer preferences, rather than simply reflecting the nature of costs.

IMPLICATIONS FOR A NGN ACCESS PRICING FRAMEWORK

What does all of this mean for the NGN operator and for regulators? Regulators are becoming acutely aware of the challenges posed by NGN regulation, and are keen not to be seen as a roadblock to the NGN superhighway. In that light, two of the principles proposed by the British communications regulator, Ofcom, for wholesale NGN pricing are particularly noteworthy:

- pricing approaches should take into account the level of demand uncertainty; and

- flexibility in pricing is desirable, allowing experimentation.

In our view an additional important principle is that access services and prices should not discriminate among access seekers (retail providers). This maximises the scope for ‘competition on the merits’ in downstream markets.

We caution that these principles could, however, prove difficult to reconcile. On the one hand, we want to allow NGN operators pricing flexibility for their wholesale services to deal with uncertainty and evolving consumer preferences. On the other, we want to maximise the opportunity for access seekers to enter the market on equal terms, and to be able to differentiate their products in order to promote innovative retail competition.

Finally, we note that moves to increase the vertical separation between network and retail functions mean that it is retail providers – not NGN operators and regulators – that will have direct access to information on how much consumers are willing to pay. That will make them best able to design the appropriate retail pricing structures, based on end-customer characteristics and preferences. The danger arises from a possible disconnection between what consumers will pay and what the NGN operator will offer.

CONCLUSION

Regulators and operators of NGNs will face some difficult decisions regarding price structures for wholesale NGN services. The fixed nature of NGN costs, increased levels of uncertainty over consumers’ willingness to pay for NGN retail services, and the trend towards vertical separation of network from retail functions, creates the real possibility of a disconnection between consumers, retailers and the NGN operator. This will have a fundamental impact on the commercial viability of the NGN and could potentially undermine the wider economic and social benefits that NGNs offer.DOWNLOAD FULL PUBLICATION