The Independent Pricing and Regulatory Tribunal (IPART) has released its draft determination on electricity prices for New South Wales recommending increases of up to 62% (including inflation) by 2013. These increases were driven by increased network costs and the assumption of an emissions trading scheme being implemented in Australia.

Frontier (Australia) undertook detailed modelling to quantify the impact of an emissions trading scheme on the wholesale electricity market and NSW regulated customers.

The Australian Competition and Consumer Commission (ACCC) today issued its view objecting to Australia Post's draft proposal to increase the prices of the letter services over which it has a statutory monopoly. The three-year pricing proposal included an increase in the basic postage rate by 5c to 60c. The ACCC’s review of the proposal highlighted concerns with Australia Post’s demand and input cost forecasts. The demand forecasts were not transparently derived and were not therefore amenable to a critical review. Input costs were forecast to rise even though volumes were projected to fall, and this discrepancy was not adequately explained by Australia Post.

Frontier (Australia) was engaged by the ACCC to critically assess Australia Post’s demand and cost input forecasts used in its notification. Frontier’s report is available here.

The Australian Competition and Consumer Commission (ACCC) has announced that it will oppose the proposed acquisition of Mobil Oil Australia’s retail assets by Caltex Australia Limited. The ACCC gave two reasons for its decision. The first was that the local competition around 53 Mobil retail sites would be likely to be reduced as a result of the acquisition. Graeme Samuel, the chairman of the ACCC, has stated that removing these sites from the deal would not be sufficient for the deal to gain approval from the ACCC. This is because of the second problem that the ACCC identified. This was that the acquisition would increase Caltex’s share of retail sites in the wider Metropolitan areas of Brisbane, Sydney, Melbourne and Adelaide; and, in the opinion of the ACCC, this would increase the stability of the weekly price cycles compared with a situation in which some or all of the sites were acquired by more maverick or aggressive retailers.

Frontier (Australia) was retained by solicitors for Caltex to undertake detailed empirical analysis of the impact on the retail prices of Caltex of concentration in local retail areas.

On 18 October, the Coalition (Australia) put forward a set of amendments to the Australian Commonwealth Government's proposed Carbon Pollution Reduction Scheme (CPRS). In response, on 24 November, the Government put forward a Revised Offer to the Coalition. Frontier (Australia) analysed the Revised Offer, using the same model as the Commonwealth Government. This analysis focused on the effects of the CPRS on non-carbon related Government tax revenues and expenditures.

Frontier's analysis shows that the Revised Offer, when compared with the Coalition's original proposals, would result in an emission trading scheme that:

increases the fiscal impact (from introducing the CPRS) to a deficit of AUS$3.7bn compared with a surplus of AUS$2.1bn;

reduces net tax revenue by AUS$11.8bn due to a less vibrant economy. This is principally due to the lower income and company tax revenues that would be observed with GDP of around AUS$50bn lower (over 20 years); and

reduces average annual wages by around AUS$800 per person.

Frontier undertook this work on its own behalf. Earlier this year Frontier advised the Coalition, and the independent Senator Nick Xenophon, on how to implement the CPRS.

The Australian National Water Commission has released its second biennial assessment of progress in the implementation of the National Water Initiative. The report titled Australian Water Reform 2009 provides a comprehensive assessment of progress by the Commonwealth, states, and territories in meeting commitments in areas including water planning, water accounting and water data, environmental water, addressing overallocation, water markets, water pricing, and urban water.

Frontier (Australia) provided the Commission with consultancy advice and support for the development of the biennial assessment.

The Australian states of Victoria and New South Wales both impose volumetric limits on inter-regional trade in water access entitlements.

Frontier (Australia) recently completed a report on these volumetric trading limits for the Australian Competition and Consumer Commission (ACCC), as an input in the ACCC's position paper on water trade rules for the Murray-Darling Basin. The paper was released on 10 September 2009.

Volumetric limits on inter-regional trade have been designed to manage the pace of community adjustment. However, Frontier's analysis in this paper suggests that these limits are likely to compromise the achievement of both efficiency and equity objectives.

Frontier found that efficiency losses due to the limits are not so much to do with the inability to move water to higher-valued uses in response to seasonal conditions (as this can still be done via allocations trading), but instead relate to longer-term considerations such as foregone ability to:

invest in new enterprises or divest from non-viable enterprises;

manage risk efficiently;

adjust to alternative forms of dryland or less intensive irrigated agriculture.

Volumetric constraints also result in a number of other unintended and detrimental distributional or equity impacts

Frontier's analysis suggests that the volumetric restrictions on trading of water entitlements have significant potential to, and increasingly in practice do, have an adverse impact on the achievement of the Basin water market and trading objectives of the Commonwealth Water Act 2007.

There is no doubt that adapting to climate change will be one of the most important and complex policy challenges facing all levels of government over the next few decades.

Frontier (Australia) recently completed a report for the Victorian Department of Treasury and Finance on adaptation responses to climate change. The report developed a decision framework - the first of its kind in Australia - to help assess the economic benefits of various adaptation proposals. Amar Breckenridge and Chris Olszak conducted the study.

Discussions surrounding adaptation are not new, but tend to suffer from a variety of drawbacks. For a start, many neglect the scope for autonomous adaptation, and the need for governments to ensure that policy interventions facilitate adaptation mediated through markets. Climate change increases the costs of existing distortions (particularly those induced by government policies implemented for other reasons) and increases the returns from reforms.

The decision framework that Frontier has developed provides a road map for systematically working through these, and other issues, in order to contribute to socially beneficial adaptation policies.

Efficient Pricing Structures For NGN Access Services

The Australian Government has commenced the roll-out of a national wholesale-only high-speed broadband access network, and is considering the regulatory arrangements that should apply to this network. In this bulletin we draw on economic theory and outcomes in competitive markets to provide some thoughts on the challenges facing regulators and next generation fixed access network (NGN) operators in structuring wholesale customer access charges.

NGNs will enable the simultaneous delivery of quality voice, high-speed data, video and television services to end customers, and potentially open up a range of new applications using these services. But they will be expensive to build, and the focus of debate so far in Australia has been how to ensure that services provided over its NGN are affordable. The role of price structure in maximising take-up and efficient utilisation of NGNs has been largely overlooked. However, it is significant: poorly designed and inflexible price structures could prevent an NGN investment from delivering on its promises.

What considerations might be relevant for designing the structure of prices for an NGN? The most obvious feature of NGNs is that their physical costs of construction are colossal (the Australian Government has estimated A$43 billion for its NGN), and these do not vary greatly with either take-up or usage of the NGN. This means that regardless of whether the take-up of services is 20% or 80% of premises passed, and whether the average consumer usage is high or low, the total cost of the NGN will be broadly the same.

On the surface, a simple response to this cost feature of a NGN might be to charge a price for wholesale access to the ‘last mile’ of the network that reflects the capacity sought, and not the usage of that capacity. For example, the NGN operator could set a monthly charge per unit of capacity required (rather than the current trend of charging for usage in the form of data downloaded). This charge would apply for access to each end customer connected. Reflecting that average infrastructure costs per customer also vary by factors such customer density and distance, one might expect some granularity in capacity charges to reflect these features as well.

Such a pricing structure for NGN wholesale access seems intuitively appealing for two reasons. First, it accords with how NGN costs will be incurred. Second, as usage charges would be minimised, it should encourage maximum usage of the network – critical to ensuring that the social benefits of widespread broadband adoption are achieved. However, two closely related questions that need to be asked about it are: is such a structure necessarily economically efficient; and is it a structure that a competitive market for NGN access services would likely arrive at? These questions are explored in turn below.

ECONOMIC THEORY

Economic theory tells us that in perfectly competitive markets with marginal costs that increase with output, economic efficiency is achieved as firms will set prices equal to marginal cost. This kind of pricing model is problematic in the NGN (and broader communications) access pricing context, because the market in which the NGN will operate will be far from perfectly competitive. An NGN is better characterised as a natural monopoly service with large fixed and common costs and average costs that fall with the level of output. This means an efficient pricing structure must take account of the need for the NGN provider to charge something more than its marginal costs (net of any public subsidy).

The conventional economic answer to this pricing problem is the use of ‘multi-part’ tariffs. The price of wholesale access would consist of a fixed fee independent from consumption, and a usage charge per unit of consumption. The levels of these tariff components will be governed chiefly by factors including the responsiveness of demand for access and usage to changes in their respective prices, and the responsiveness of the demands of each of these services to the prices of the other.

This simple answer overlooks at least two further pricing issues that might give the NGN operator cause for concern. The first is ensuring that prices capture ‘network effects’. These effects may justify pricing to some users at ‘below cost’. This could be efficient if there are benefits gained by other users from connecting new users, and part of this can be appropriated by the NGN operator.

The second issue is the social issue of promoting equitable access to broadband. This will be particularly pertinent if the government – as in Australia – finances much of the construction cost. High fixed charges may well deter take-up in locations that are expensive to serve, or by lower socio-economic groups.

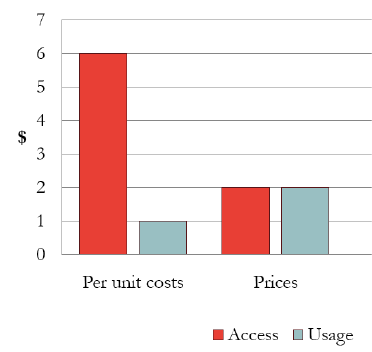

What is clear from economic theory is that the structure of prices will only be closely tied to cost causation under very strict conditions. Other structures could well be more efficient and more equitable. The figure to the right illustrates an example of that kind of pricing outcome. It shows a case where usage prices are marked-up to help recover the losses on the pricing of access. At four units of usage and one unit of access, the NGN operator will just recover its costs – and take-up may well be higher.

OBSERVED MARKET OUTCOMES

The mobile communications market provides a particularly good example of how firms can adapt pricing structures to reflect complexity on both the supply and demand sides. Mobile services charges commonly comprise both fixed and usage charges, as predicted by the basic economic theory, but these have evolved in interesting ways. Until recently, it had been very common for the fixed costs of access, such as the handset, to be primarily recovered through call charges, even though the cost of the handset is unrelated to usage. However more recently, fixed subscription pricing (in the form of monthly minimum but capped spends) has become a key feature of pricing plans that tend to diminish the role of usage charges as a means of recovering handset and other fixed costs of access.

Innovative forms of pricing are also common in other industries where consumers are sensitive to high up-front charges. A good example is the partial recovery of the cost of printers in the price of printer-specific ink cartridges.

These examples illustrate that reasonably competitive unregulated markets do in fact come up with pricing structures that reflect evolving consumer preferences, rather than simply reflecting the nature of costs.

IMPLICATIONS FOR A NGN ACCESS PRICING FRAMEWORK

What does all of this mean for the NGN operator and for regulators? Regulators are becoming acutely aware of the challenges posed by NGN regulation, and are keen not to be seen as a roadblock to the NGN superhighway. In that light, two of the principles proposed by the British communications regulator, Ofcom, for wholesale NGN pricing are particularly noteworthy:

pricing approaches should take into account the level of demand uncertainty; and

flexibility in pricing is desirable, allowing experimentation.

In our view an additional important principle is that access services and prices should not discriminate among access seekers (retail providers). This maximises the scope for ‘competition on the merits’ in downstream markets.

We caution that these principles could, however, prove difficult to reconcile. On the one hand, we want to allow NGN operators pricing flexibility for their wholesale services to deal with uncertainty and evolving consumer preferences. On the other, we want to maximise the opportunity for access seekers to enter the market on equal terms, and to be able to differentiate their products in order to promote innovative retail competition.

Finally, we note that moves to increase the vertical separation between network and retail functions mean that it is retail providers – not NGN operators and regulators – that will have direct access to information on how much consumers are willing to pay. That will make them best able to design the appropriate retail pricing structures, based on end-customer characteristics and preferences. The danger arises from a possible disconnection between what consumers will pay and what the NGN operator will offer.

CONCLUSION

Regulators and operators of NGNs will face some difficult decisions regarding price structures for wholesale NGN services. The fixed nature of NGN costs, increased levels of uncertainty over consumers’ willingness to pay for NGN retail services, and the trend towards vertical separation of network from retail functions, creates the real possibility of a disconnection between consumers, retailers and the NGN operator. This will have a fundamental impact on the commercial viability of the NGN and could potentially undermine the wider economic and social benefits that NGNs offer.DOWNLOAD FULL PUBLICATION

The Australian Government has commenced the roll-out of a national wholesale-only high-speed broadband access network. A host of commercial and regulatory issues are still to be resolved and, in this bulletin, Frontier Economics (Australia) looks at one of these; efficient pricing structures for wholesale access services.

We draw on economic theory and outcomes in competitive markets to provide some thoughts on the challenges facing regulators and next generation fixed access network operators in structuring these charges.

Frontier (Australia) has released a report that provides independent modelling of the Government’s proposed Carbon Pollution Reduction Scheme (CPRS), and which models an alternative set of policy options. Frontier’s work was commissioned by the Coalition and by the Independent Senator for South Australia Nick Xenophon to consider whether an Emissions Trading Scheme (ETS) could be implemented in a manner that maintained or increased unconditional reductions in carbon output, was more efficient and less costly, and reduced the expected negative impact on employment across Australia.DOWNLOAD FULL PUBLICATION

We use cookies to ensure that we give you the best experience on our website. By continuing on this site, you are agreeing to our use of cookies.OKPrivacy policy