The case for developer charges: fair water infrastructure contributions promote better development outcomes and reduce infrastructure costs to the community

Developer groups have opposed Sydney Water and Hunter Water’s planned reintroduction of infrastructure contributions (or ‘developer charges’). These charges to developers help recover the area-specific, development-contingent costs of providing or upgrading the water, wastewater and stormwater drainage networks to serve new development.

However, such contributions have never been more important to the community. These charges signal to developers the costs of providing infrastructure in different areas, and thus promote socially optimal development decisions – i.e., development in locations where the benefits to the community exceed the costs. They also minimise price increases to customers’ water bills (helping to reduce cost of living pressures), and they allow some of the land value uplift generated by rezoning to fund much needed infrastructure.

Cost-reflective infrastructure contributions can also be an efficient and fair funding source for infrastructure provided by local councils to serve new developments, including much needed public open space, transport (eg, local roads) and local stormwater infrastructure.

The reintroduction of water and wastewater developer charges

The term ‘rent-seeking’ was first used to describe the wasting of resources by entrepreneurs to fight for artificially created wealth transfers. This is an apt description for the time spent in recent years by developers seeking to convince the NSW Government to resist the reintroduction of cost-reflective water, wastewater and stormwater infrastructure contributions (or ‘developer charges’) in Sydney and the Hunter.

Following a review by the NSW Productivity Commission in 2020, the NSW Government committed to reform the infrastructure contributions system, with a key element being the phased reintroduction of developer charges for Sydney Water and Hunter Water’s water, wastewater and stormwater services. This follows over a decade of these charges being set to zero (set by Ministerial direction in 2008). The consequence has been that Sydney Water and Hunter Water’s additional costs to provide water infrastructure to service new developments has not been recovered from developers, but from all water, wastewater and stormwater customers via their quarterly bills.

Under the methodology set by the NSW Independent Pricing and Regulatory Tribunal (IPART), these infrastructure contributions would recover Sydney Water and Hunter Water’s costs of providing water, wastewater and stormwater services to new development areas that are above and beyond the retail price revenue the water utilities will receive from servicing customers in the new development areas over time.[1]

Developers have long opposed paying these infrastructure contributions, arguing these costs should be borne by the wider community. They have suggested a broader revenue base (i.e., anyone but them) for infrastructure funding is needed, and that there is limited public benefit to infrastructure contributions.

Given concerns about housing affordability, the community is naturally interested in the key supply-side and demand-side drivers of house prices. Seeing an opportunity, developer groups have sought to re-prosecute their case opposing the developer charges as they claim they increase development costs and house prices.[2]

However, given the incentives at play, this requires closer scrutiny. Do these charges really increase development costs and house prices? What are the implications to the broader community and water customers if these infrastructure contributions are not reintroduced?

A cost to whom?

Infrastructure contributions may be a new cost to developers, but not to society. That is, infrastructure contributions do not create costs, they just represent a way of recovering them.

Since 2008, the costs of providing development-contingent water infrastructure have been paid by all water, wastewater and stormwater customers across Sydney Water and Hunter Water’s areas of operation through their regulated prices. IPART, with responsibility for setting maximum charges levied by Sydney Water and Hunter Water, explicitly accounts for these when setting the charges that are levied on customers via their quarterly bills. This decade old subsidy from water customers (including households) to developers has added billions of dollars to water bills of households and businesses, directly impacting the affordability of these essential services.

In 2019, IPART estimated that by 2029, Sydney Water’s average customer would be paying an additional $140 per year for their water, wastewater and stormwater services if infrastructure contributions were to continue to be set to zero.[3]

Despite the overwhelming current media focus on the cost of living, this impact on the affordability of water is one of the few areas that has escaped public scrutiny.

Re-introducing cost-reflective infrastructure contributions would simply reallocate these costs back to developers, who are creating the need to incur them and benefitting from them. This is in line with the “impactor pays” principle, enshrined in the Council of Australian Government’s National Water Initiative Pricing Principles, which were designed to increase the efficiency of Australia's water resources and infrastructure assets. This principle also underpins funding for a range of other critical services.

The reintroduction of infrastructure contributions would provide bill relief to all water customers, which will be increasingly important as major metropolitan centres in Greater Sydney and the Hunter continue to grow, and households face cost of living pressures.

Supporting planning objectives and efficient development

Cost-reflective infrastructure contributions also support planning objectives, by signalling to developers the costs of providing water infrastructure to different areas in Sydney and the Hunter – with some areas being higher cost and others lower cost to service, and these variations being ideally reflected in infrastructure contributions.

This price signal would encourage efficient development decisions. Currently, without such cost-reflective infrastructure contributions, developers do not need to consider the different cost of providing water infrastructure to different areas in Sydney. This means there is a risk they develop in areas where the costs to the community of providing such infrastructure exceeds the benefits of the development.

Smearing development-contingent costs across all water customers risks diluting one of the key signals related to the cost of development between locations, which in turn can contribute to inefficient investment in relatively high-cost areas.

As the NSW Premier and Productivity Commission have recently said, we need to improve how we plan and develop Sydney to minimise stretching of infrastructure services, including building more housing in infrastructure corridors to enhance amenity, lower infrastructure costs and improve housing affordability.[4]

Water infrastructure contributions and house prices

Provided developers have sufficient line of sight of infrastructure contributions (i.e., they are aware of these contributions before they purchase developable land), the economics of housing supply tells us that these costs are not necessarily passed through to homeowners through higher house prices.

As observed through numerous studies across multiple jurisdictions and the NSW Productivity Commission (see Box 1 in PDF Bulletin), they are likely to be factored into the prices developers pay for developable land – resulting in a lower than otherwise price to the landowner, who may still receive significant windfall gains by virtue of their land being rezoned or deemed developable.

That is, infrastructure contributions can allow some of the land value uplift generated by rezoning to fund much needed infrastructure.

If there are occasions where this means the landowner is not willing to sell to the developer, this would indicate that the benefits of the potential development in that location (as measured by what the developer is willing to pay for the land) does not exceed its costs to the community. However, this is unlikely to be common, as in an environment of increasing population, the value of developable land in and surrounding cities often exceeds its opportunity cost in alternative uses (e.g., for industrial use or agricultural production).

This key conclusion – that housing affordability is not exacerbated by infrastructure contributions, provided developers are aware of these contributions before they purchase developable land – is also backed up by empirical literature. Abelson (1999)[5], Ruming, Gurran and Randolph (2011)[6], Davidoff and Leigh (2013)[7] and Murray (2018)[8] all found that the incidence of development contributions likely falls on developers or landowners rather than home buyers.

The most reliable Australian evidence is consistent with this view; with little credible evidence to the contrary.[9]

The NSW Productivity Commission has observed that, as a policy to increase housing supply, setting Sydney Water and Hunter Water’s infrastructure contributions to zero has been ineffective and costly, predominantly resulting in a transfer of wealth from water customers to owners of developable land, “including those that would have developed land regardless”.[10]

Where to from here?

Cost-reflective infrastructure contributions can help to fund infrastructure more fairly, reduce pressure on water bills to residential and non-residential customers, and support better planning and development outcomes.

The focus should not be on whether these contributions should be reintroduced, but rather how to:

ensure water, wastewater and stormwater infrastructure solutions and services provided by Sydney Water and Hunter Water meet the community’s expectations and needs, including in relation to enhanced environmental, amenity and liveability outcomes;

set infrastructure contributions to ensure they reflect the efficient costs of development-contingent water, wastewater and stormwater infrastructure to various areas within Greater Sydney and the Hunter; and

phase in and administer these charges to provide sufficient line of sight and certainty to developers to enable them to consider and respond to these important price signals, for the benefit of the community.

Resources spent on doing these well, rather than “rent-seeking”, will deliver value to the whole community, including developers.

Importantly, for the same reasons as outlined above, cost reflective infrastructure contributions can be an efficient and equitable funding source for infrastructure provided by local councils to serve new development – including public open space, transport (such as local roads) and stormwater infrastructure.

[1] Retail prices to customers reflect network-wide average costs (i.e., all customers face the same prices, regardless of their location within the utility’s network). Infrastructure contributions therefore recover the difference between the costs of servicing a specific development area and network-wide average costs.

[2] Daily Telegraph, Water torture for new housing, May 12, 2023.

[3] IPART, Prices for Sydney Water from 1 July 2020, Issues Paper, September 2019, p 29.

[4]NSW Premier Chris Minns puts Sydney NIMBYs on notice, 15 May 2023; Sydney Morning Herald, Sydney’s richest suburbs need to be higher, denser to solve housing crisis, 31 May 2023.

[5] Abelson, P, 1999, ‘The real incidence of imposts on residential land development and building’, Economic Papers, vol. 8, no. 3.

[6] Ruming, K, Gurran, N, & Randolph, B, 2011, ‘Housing Affordability and Development Contributions: New Perspectives from Industry and Local Government in New South Wales, Victoria and Queensland’, Urban Policy and Research, vol. 29, no. 3, pp. 257–274.

[7] Davidoff, I & Leigh, A, 2013, ‘How do Stamp Duties Affect the Housing Market’, Economic Record, vol. 89, no.286.

[9] Bryant (2017) finds a substantial impact on house prices however there are a number of concerns with the empirical approach taken. UQ Economist Cameron Murray’s paper, in response to the work of Bryant, is more convincing, having applied a clear empirical strategy exploiting unanticipated changes to the developer charge regime to identify the impact of these developer charges, finding no impact on house prices and therefore house buyers. Even more illustrative is the replication of the results of Bryant (2017) when ignoring the mechanical relationship between house characteristics and developer charges.

[10] NSW Productivity Commission, Review of Infrastructure Contributions in New South Wales, Final Report, November 2020, p 101.DOWNLOAD FULL PUBLICATION

Transition support for the NSW native forest sector

With the Victorian government announcing an end to native forest logging by 1 January 2024, we revisit a recent report prepared for WWF–Australia (World Wide Fund for Nature Australia) in August last year. In it, Rachel Lowry, Acting CEO, WWF–Australia explains, “This report was not commissioned to ignite or exacerbate ‘forestry wars’. Instead, it is designed to inform and motivate critical solution-focussed discussions, ideally led by the NSW Government.”

The New South Wales (NSW) native forest sector has been contracting over a long period as publicly provided wood supply has fallen to more sustainable levels. The 2019–20 Black Summer fires compounded this trend, significantly reducing sustainable wood supplies, particularly in the South Coast and Tumut regions. This shock to the sector, economy and regional communities – combined with an increased recognition of the significantly higher value that standing native forests offer in comparison to logging– provides an opportunity to reconsider the best use of NSW’s native forest resource. Other states including Victoria and Western Australia facing similar issues have made the decision to end the native forest logging.

In this context, Frontier Economics was engaged by WWF–Australia to consider options for the design of appropriate structural adjustment arrangements that would accompany a decision to end public native forest logging in NSW. Our Report, Transition support for the NSW native forest sector, outlines a design and cost estimate of such structural adjustment supports.

The financial return and economic contribution of public native forestry is small

Our Report found that Forestry Corporation of NSW’s (FCNSW’s) native forest logging business appears to offer poor financial returns to NSW taxpayers, with some parts of the hardwood business unlikely to be covering costs. The Independent Pricing and Regulatory Tribunal of NSW (IPART) has also reported on the loss-making activities of FCNSW’s hardwood division.

There is also clear evidence that that value of the native forest would be higher as a standing resource.

The volume of wood supplied by FCNSW’s native forest business has been falling, and is unlikely to return to historic levels of production given the current state of the native forest after the Black Summer fires and the increasing impacts of climate change.

Employment and economic contribution have also fallen to modest levels, even when both hardwood and softwood, and private and public industry in NSW is accounted for. Direct employment associated with FCNSW’s hardwood business is in the order of 1,070 across the State – including those employed by FCNSW, harvest/haulage contractors and mills.

Designing a comprehensive structural adjustment support package

A comprehensive structural adjustment package should accompany the decision to cease the remaining native forest logging activity by FCNSW. This package would support impacted employees, firms and communities during the transition.

Across jurisdictions, there is a broad consistency in the design of public native forest logging structural adjustment packages, including:

Support for workers through redundancy top-up payments and resources for retraining,

Support for harvest/haulage contractors and mills through capital redundancy payments,

Wood supply contract buy-backs, and

Longer term funding to diversify local regional economies.

Structural adjustment packages are also often complimented with longer term support for increased investment in plantation resources.

Alongside a package of structural adjustment support, our Report finds there are likely to be alternative employment opportunities for displaced workers from the public native forestry sector, particularly in management of protected forest areas, recreation and tourism, plantation-based forestry work, fire and invasive species management and the management of carbon and biodiversity credits.

The estimated cost of structural adjustment support

The estimated cost of the government-funded structural adjustment is $302 million in total. This includes:

Up front structural adjustment funding of $244 million. This covers payments to support worker redundancies and retraining, capital redundancies and Wood Supply Agreement (WSA) buy-backs, and

Structural adjustment funding for regional economic diversification of $58 million, spent over a 10-year period.

Our Report developed these estimates along similar lines to those adopted in other jurisdictions. It is assumed the adjustment package would be implemented from 2028- 29 once the majority of the current WSAs with processors have expired.

The cost of the structural adjustment package is likely to be readily outweighed by a range of positive budgetary impacts including:

Avoided ongoing structural adjustment and bushfire support to the hardwood sector,

Avoided equity injections to FCNSW, and

The likelihood of increased dividends from FCNSW over time by avoiding the loss-making activities of the hardwood division.

FCNSW and plantation investment

Complementing a structural adjustment support package, the NSW Government may invest in increased plantation resources. The Victorian and West Australian governments have announced funding for plantations of $110 million and $350 million, respectively.

Alternatively, FCNSW may consider the investment opportunity to expand its hardwood plantation estate in the expectation of a long-term financial return.

The forestry sector would sensibly lead any plantation expansion in NSW based on its understanding of the best locations, appropriate size of expansion, plantation species and market needs.

View the full report commissioned by WWF-Australia here.

Building a business case to confidently manage climate-related risks and opportunities

Climate change impacts will continue to unfold across Australia with increasing severity in the years ahead. This will result in a set of complex and material financial implications for business. For Australian business to confidently rise to the challenge of systematically measuring, managing and mitigating risks and opportunities of climate change it will need a sound understanding of how climate change will most likely impact its finances. This Bulletin discusses Frontier Economics and Edge Environment’s approach to extending climate risk frameworks to build business cases for climate response against the inevitable, and potentially disorderly, climate transition ahead.

Australia is in the midst of cascading and compounding climate impacts

After centuries of relative climate stability, the world’s climate is changing. As average temperatures rise, acute hazards such as floods and fires and chronic hazards such as drought and sea level rise intensify. These hazards are categorised as the physical risks of climate change.

The frequency and severity of weather events in Australia is increasing and may further intensify as ecosystems are pushed beyond tipping points. Recent weather events in Australia such as the unprecedented rainfall and flooding in South-East Queensland, New South Wales and Victoria, extreme heat in Western Australia and the 2019–20 bushfires have resulted in highly significant financial losses for businesses and the communities they operate in.

Climate risk, however, remains an emerging discipline compared to other traditional risk areas. Climate risk management will necessarily grow in importance over coming years – recently, the Australian Prudential Regulation Authority (APRA) warned business around the need to prepare for “rapidly increasing expectations” on climate risk disclosure.

Against this backdrop, forward looking businesses are taking steps to understand, quantify and manage their climate risk exposures.The good news is we have the tools to address urban heat: integrated planning of our natural and built environment covering blue, green, and grey infrastructure.

TCFD is a lens to grapple with these risks

The Taskforce on Climate-related Financial Disclosures (TCFD) reporting framework has emerged as the global benchmark in climate risk reporting. It seeks to make businesses’ climate related disclosures comprehensive, consistent and transparent. TCFD enables effective investor analysis of a company’s demonstrated performance of incorporating climate related risks and opportunities into businesses’ risk management, strategic planning and decision making.

The TCFD was set up in 2017 by the Financial Stability Board – an international body of regulators, treasury officials and central banks – to provide voluntary recommendations on how business could voluntarily disclose the risks and opportunities from climate change (see Box 1).

Box 1: TCFD in brief

The purpose of TCFD is to provide a framework for organisations to make consistent and transparent climate-related financial disclosures. The TCFD framework document provides the following overview of the types of disclosures that it recommends:

Governance: Disclose the organisation’s governance around climate related risks and opportunities.

Strategy: Disclose the actual and potential impacts of climate-related risks and opportunities on the organisation’s businesses, strategy, and financial planning where such information is material.

Risk management: Disclose how the organisation identifies, assesses, and manages climate-related risks.

Metrics and targets: Disclose the metrics and targets used to assess and manage relevant climate-related risks and opportunities where such information is material.

It is recommended that the business provides its disclosures in their public annual reporting.

Source: Recommendations of the Task Force on Climate-related Financial Disclosures

Momentum in the market is growing and norms are being set

Since being first published in 2017, TCFD has been rapidly adopted by a broad range of organisations across the globe – the 2022 status report for TCFD points to TCFD “support” encompassing US$220 trillion of assets and US$26 trillion of combined company market capitalisation.

There is a trend towards mandating climate-related disclosures. Mandatory climate risk disclosures have been announced in jurisdictions including the UK, the EU, Hong Kong, Japan, Singapore and New Zealand. Significantly, the United States Securities and Exchange Commission has proposed rules to enhance climate-related risk disclosure drawing from the TCFD recommendations. Collectively, these actions will set norms and expectations for Australian businesses to develop their own disclosures.

In 2021 the New Zealand Government passed legislation mandating climate-related disclosures for around 200 financial entities. Further to impacting those covered by the introduction of this mandate, the move is widely expected to act as a catalyst for increased climate-related disclosures across businesses operating in the wider New Zealand economy.

Decision making under complexity needs tangible financial analysis

While TCFD is ultimately intended to support more informed capital allocation by investors, it can also be an important tool for organisations to respond to the risks and opportunities of climate change.

For an approach to inform practical decision making it needs to provide climate-related impacts in financial terms:

In the case of climate risks, the approach would allow for adaptation, mitigation and divestment intervention options to be directly compared to a “do nothing scenario”;

It would facilitate the valuation of climate-related opportunities, such as, product innovation, renewable energy generation, water recycling, resilient supply chains, and cost savings in energy or resource use; and

The approach will be flexible to recognise that risks and opportunities will vary depending on the region, market and industry that the business operates in.

Clearly this is a complex task, but it needn’t be daunting if we have the right tools and systematic approaches. Finding a solution requires assessing the changing climate exposure and vulnerabilities of an enterprise through time. A collaborative approach which brings together the key stakeholders across an enterprise provides the means to map the material climate impacts, their drivers and the likely financial consequences to the company. This collaborative approach also enables joint ownership of critical uncertainties to be addressed within business’ operations, financial reporting and data management. A structured approach is then required to cut through the uncertainty and deliver a clear path forward to adequately measure, manage and mitigate climate risks.

Frontier Economics and Edge Environment have partnered to combine our skills in financial analysis, ESG, risk management, climate science and sustainability to work through this complexity (see Box 2).

Box 2: Frontier Economics’ partnership with Edge Environment

Edge Environment and Frontier Economics have worked across a broad range of climate risk and resilience projects, mostly within the property, infrastructure and government sectors. Together, this partnership provides a unique opportunity to better understand both financial risks and opportunities of climate change for Australian and New Zealand businesses.

Edge is a specialist sustainability services company focused on Asia-Pacific and the Americas. Its teams are based in Australia, New Zealand, the United States and Chile. Edge exists to help its clients create value from tackling one of world’s most fundamental challenges: creating truly sustainable economies and societies. Edge does this by combining science, strategy and storytelling in a way that gives clients the confidence to take ambitious action, and do well by doing good.

Source: Frontier Economics

A collaborative approach is required to address this complexity

Confident climate-risk decision making requires a multi-disciplinary approach, incorporating climate science and financial analysis. However, deep technical expertise alone is not sufficient.

There is also a need for broad buy-in and engagement from within and across an organisation in order to access information, form granular insights, identify key operational climate-related impacts and quantify financial consequence. Organisations are encouraged to systematically look beyond the acute and direct impact of extreme events but also to the aggregated impacts of chronic and indirect effects of climate extremes.

Even with all these elements, it can be difficult to know where to start a climate-related financial analysis.

Frontier Economics and Edge have developed a practical approach

A useful starting point in analysing climate-related risk and opportunities is to assess the impacts of recent extreme climate events – such as the Eastern Australia bushfires and drought of 2019-20 and the extreme rainfall of 2021-22 – on a business’ operations and related cashflows.

This “looking back to look forwards” approach provides multiple advantages. It allows the:

development of logic maps, from climate drivers to asset and operational impacts;

identification of related notional financial consequences; and

engagement from across the business on climate-related risks and opportunities.

Shared understanding of the constraints and limitations in financial data management which may need to be addressed to enable the aggregated costs of climate impacts to be assessed with confidence

The logic mapping and notional financial consequences can then be tested and validated using actual operational and financial data to identify the impacts of recent extreme events.

This approach also clearly highlights any data gaps which limit the extent to which financial consequences can be isolated – providing insight to improve risk management systems.

This baseline analysis has standalone value as it provides a snapshot of the resilience of an organisation to recent climate change events which can be linked back to materiality thresholds in a firm’s enterprise risk framework. It is also vital in building a foundation for robust and defensible scenario analyses of the likely impacts of future climate extremes on an enterprise. It can be used to inform forward looking analysis of climate change impacts, which considers both cash flow and asset valuation risks and opportunities.

The approach taken by Frontier Economics and Edge Environment focusses on undertaking robust, transparent and actionable analysis. For example, we focus first on the short-term (to 2025) before extending analyses further into the future. A short-term lens reduces uncertainty and allows organisations to home in on impacts which require urgent action. It also allows for extensions such as cost-benefit analysis to support investment decisions around certain interventions.

Building the business case to confidently make decisions about managing your organisations climate risk is a journey – come and talk to us about getting started.

Integrated planning, economics and quantifying the value of urban cooling

The costs of excessive urban heat are significant and lead to negative consequences for the health of our communities, environments and infrastructure. Increasingly, integrated planning of our natural and built environment covering blue, green and grey infrastructure is recognised as a force to reduce urban heat. This bulletin describes how mainstream evaluation practice can incorporate economic tools to identify, quantify and integrate urban cooling into decision-making frameworks in order to quantify benefits and support better decisions.

Excessive urban heat is a growing economic problem for our cities

Australia is particularly exposed to the physical risks of climate change, including heatwaves. In 2019 and 2020, Australia experienced the two hottest summers on record, with major metropolitan areas, as well as regional towns, experiencing catastrophic bushfires.

Across the coming decades, global temperatures are expected to rise more than 2.4⁰C above pre-industrial levels, the consequences of which are likely to disproportionally fall on our urban spaces.

Cities are more vulnerable to temperature rises because vegetation, open space and tree canopy is often replaced with concrete, roads and other heat-absorbing materials that radiate the heat they absorb during the day and through the night.

Our cities are already paying the price of excessive urban heat. These costs include increased pressure on our water and energy infrastructure as the infrastructure manages the consequences of increasing average and maximum urban temperatures. These also include increased likelihood of heat-related illness which put pressure on our healthcare sectors. Of all natural hazards, heatwaves currently represent the biggest cause of death in Australia.

However excessive urban heat can create longer-term costs associated with inactivity and mental health related illness as a result of reduced opportunities for passive and active outdoor recreation. Many of these costs accrue slowly over time.

At the same time, mainstream approaches to the provision of infrastructure and services are often blind to these costs, or struggle to rigorously recognise and incorporate them into decision making.

The good news is we have the tools to address urban heat: integrated planning of our natural and built environment covering blue, green, and grey infrastructure. This includes integrating the provision of:

Tree canopy and open green space throughout the development (‘green infrastructure’)

The use of water in the landscape such as water features, rivers and waterways (‘blue infrastructure’)

The use of ‘cooler’ building materials such as green roofs, insulation, white paint for roofs and external shading including awnings, vertical fins and horizontal eaves (‘grey infrastructure’).

Blue, green and grey infrastructure provides the potential to use existing and any new infrastructure more efficiently and create cool, liveable communities and environments. In many respects, these investments can have public good related characteristics with benefits accruing to a range of beneficiaries, some beyond the local environment.

Blue, green and grey infrastructure provide proven urban cooling benefits, but are not always well integrated into decision-making

It is increasingly recognised that blue, green and grey infrastructure plays an integral role in the provision of cool, green, liveable cities. Despite this, historically the benefits of reduced urban heat have not been well integrated into infrastructure investment decisions.

In our experience, this is because the site-specific, dispersed nature of urban heat means for integrated blue, green and grey infrastructure investments (compared to more traditional investments), it can be more difficult to:

identify the full range of benefits associated with a reduction of urban heat − which can involve economic, social and environmental changes − the magnitude of which vary significantly with the project and location, and so require robust place-based analysis

measure and value the full range of benefits when they typically have no observable market price (i.e., non-market benefits such as reduced urban heat-related disease burden) requiring specialist economic valuation techniques, and

engage with beneficiaries and securing co-funding. For example, beneficiaries can go beyond those who live and work in the area and include the broader community, governments, energy utilities and the health sector. The dispersed nature of beneficiaries means that it can often be difficult to secure co-funding from those who benefit from these investments.

securing financing to cover what are often larger upfront investment costs for larger ongoing benefits (or cost savings). However, with growing investor appetite for green and sustainable investment opportunities, the potential for new and favourable funding opportunities have arisen for projects backed by a robust business case.

Economics is the key to integrating the value of urban cooling into decision-making

Too often these barriers have led to sub-optimal consideration of the benefits of reducing urban heat and risks inefficient allocation of scarce community resources and funding. This is especially pressing given that the current scale of urban development across Australia presents time-limited window of opportunity to avoid locking in our historical urban development paradigm for the long-run. Our decisions made today cannot be easily reversed.

The question then is, how do we embed active consideration of these urban cooling benefits into our decision-making process?

While government policy could mandate investment in blue and green infrastructure, prescribing a one-size-fits-all approach does not guarantee smart investments. In some circumstances, the expense of setting up and maintaining blue, green and grey infrastructure will be more than outweighed by its benefits.

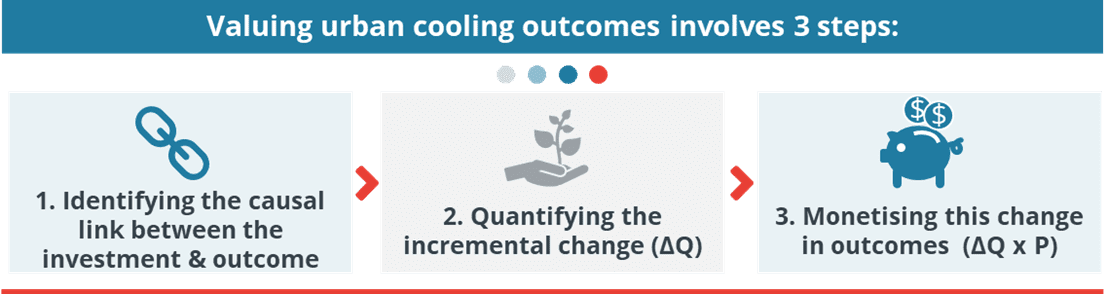

Economic evaluation frameworks such as cost benefit analysis (CBA) provide the means to identify value-enhancing urban-cooling investments through incorporating and monetising these broader costs and benefits. This requires 3 steps:

Identifying the causal link between the blue, green or grey investment and urban-cooling related outcomes (such as reduced energy demand, reduced heat related illness or increased inactivity related disease).

Quantifying the incremental change (ΔQ), which can be challenging and often requires site-specific scientific or engineering analysis. For example, properly assessing the urban cooling mitigation impact of an urban heat mitigation option might require establishing the change in urban temperature attributable to water investments alone.

Monetising this change in outcomes. (ΔQ x P), which can require undertaking primary research or the application of economic techniques such as benefit transfer.

While these steps are not always easy and can require collaboration across sectors and disciplines, they provide a robust and defensible framework for identifying where and when blue and green investments can cost-effectively manage urban heat.

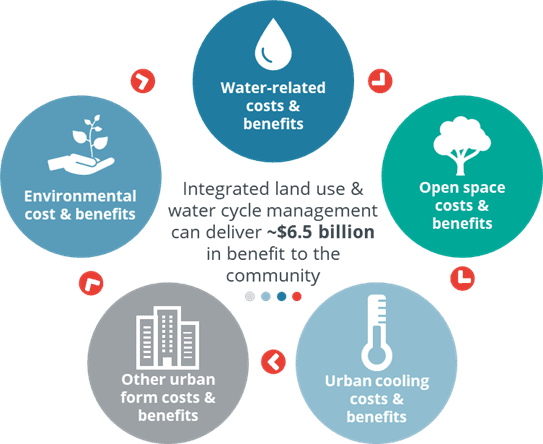

We know this approach works: The $6.5 billion opportunity in Sydney’s Western Parkland City

The Western Parkland City is a priority growth area located in one of the hottest and driest parts of Greater Sydney. To draw people and businesses to the area, the City will need to offer a ‘cool and green’ environment. This means creating attractive urban communities and appealing places to live, work and play.

However, this urbanisation will place major pressure on the health of Wianamatta South Creek, its tributaries and the local environment and pose significant challenges in meeting a much higher community demand for water-related services. Water will also be needed to increase the urban tree canopy, maintain shaded, open and green space and support water features

Infrastructure NSW and Frontier Economics’ strategic options business case for the Western Parkland City (South Creek Catchment) found that, in the face of these challenges, integrated land use and water cycle management in the City can deliver significant economic, social and environment benefits.

The framework developed to monetise these economic, social and environmental impacts, found that integrated land use and water cycle management can deliver around $6.5 billion in benefits to the local, Greater Sydney and broader NSW communities.[1]

A key driver of these benefits was related to urban cooling related investments, which could lead to a reduction of up to 2.2°C in forecast maximum summer daily temperatures across the Western Parkland City. This reduction in urban temperature, in turn, was found to lead to associated reductions in energy consumption, peak demand, and heat-related deaths and healthcare costs.

Our analysis showed that quantifying these values in dollar figures enables effective policy, regulatory and investment decision-making, and ultimately leads to more attractive, liveable and productive places.

Further, as a result of our work with INSW, Infrastructure Australia designated blue-green infrastructure in the Western Parkland City as a national priority initiative.[1] It is a rare example of a non-traditional infrastructure project on the list.

Where to from here?

There is often only one chance to get urban spaces truly right, and now is the time to integrate the benefits of urban cooling into our urban infrastructure choices. It becomes harder and more costly to rectify the outcomes of poor past decisions.

Failure to address the resilience of cities to urban heat − including the role of blue, green and grey infrastructure − as a part of decision-making exposes the community to growing risks, which if were to crystalise would impose significant and broad economic, social and environmental costs.

Decision-makers should approach and incorporate economic, planning, design and development decisions.

Basing infrastructure decisions on good economics that draws on scientific, ecological, planning and engineering expertise and properly factors in economic, social and environmental outcomes into the ultimate investment decision is critical to delivering cool, green, liveable and resilient cities today and for decades to come.

This will require collaboration between economists, scientists, planners across the public and private sector to better identify, quantify, value and incorporate these benefits into decision-making.

Infrastructure Australia today released the 2021 Australian Infrastructure Plan, which provides Australia’s green, grey and blue infrastructure sector with a 15 year roadmap to drive economic growth, maintain and enhance our standard of living and improve the resilience and sustainability of Australia’s essential infrastructure.

The 2021 Plan provides Infrastructure Australia’s reform pathway to respond to the 180 infrastructure challenges and opportunities identified in the 2019 Australian Infrastructure Audit. There are a number of key themes in the plan. We highlight and discuss several of these below.

The inclusion of waste and social infrastructure (such as green and blue infrastructure) for the first time, alongside energy, transport, telecommunications and water.

The need for place-based decision-making, including the need to holistically plan blue, green and grey infrastructure.

The report recognises that the analysis Frontier Economics did alongside Infrastructure NSW is an example of how early incorporation of water management into land-use planning can enhance liveability and deliver over $6.5 billion in benefits to the community. This opportunity for integrated water cycle management in South Creek is a priority initiative on the 2021 Infrastructure Priority List (see page 443 of the plan).

The need to embed sustainability and resilience into infrastructure decision-making, including the importance of a consistent all-hazards, systems approach to resilience planning and quantification of the costs, impacts and benefits of resilience investment.

Recognition of the need for clear management and governance of the water cycle, including stormwater and waterways.

For the next stage of planning for the South Creek area, via the South Creek Sector Review, Frontier Economics is assisting the NSW Department of Planning, Industry and Environment to consider stormwater and waterway governance.

The need to remove targets, mandates and subsidies for certain types of water, including recycled water. (For a look at how to encourage uptake of recycled water initiatives, and barriers, Frontier Economics undertook a review for Infrastructure NSW.)

It is a comprehensive plan addressing all aspects of infrastructure. It puts forth a compelling vision of Australia in 2036, that includes liveable, attractive and resilient communities with social infrastructure supporting a strong, healthy and prosperous nation.

The urban economics team at Frontier Economics advises across these areas. For more information or to discuss a project, please contact us.

Specifying required outcomes is key to unlocking green infrastructure funding

A clear view of the outcomes we want in our urban landscape is key to unlocking funding for green infrastructure. COVID-19 has highlighted, more than ever, the importance of green infrastructure and open space – as for many of us these features of our urban environment have been an important source of refuge during the challenges we’ve faced over the last year. Green infrastructure (or blue-green infrastructure) refers to the tree canopy, parks, waterways, vegetation, wetlands and lakes in our cities. It delivers enormous benefits to our community, and it is much more than just pleasant ‘greening’. Green infrastructure can make our cities cooler, healthier, more ecologically sustainable and attractive places to live and work.

Given the rate of development in our cities, the pressures on our urban environments and the adjacent natural environments, and the importance of integrating green infrastructure with other forms of infrastructure early in the development process, there is an urgency to improve the provision of green infrastructure. This requires a step-up in funding.

In a previous bulletin, Greening our cities: from vision to value, we observed that we need to actively embed consideration of green infrastructure into our planning and decision-making processes, and that a key element of this is identifying and accurately valuing the costs and benefits of green infrastructure.

This bulletin explores why greater clarity about the specific green outcomes (or standards) we need as a community is a key step in securing efficient and sustainable sources of funding for green infrastructure. As much as possible, policy and funding certainty for green infrastructure needs to be in place ahead of the growth and development that is occurring across major metropolitan areas.

There’s value in green

In high-level strategic plans for cities and urban areas, governments are now recognising urban nature as genuine infrastructure that delivers valuable services to the community and which merits policy and planning priority. They recognise that the natural green (and blue) assets of a city can deliver real public benefits, including mitigating the urban heat island effect, protecting and restoring ecological health, promoting active lifestyles, and providing beautiful places to live, work and play.

A clear government policy vision for green infrastructure is a good (and necessary) start. To transfer this vision into reality, however, requires:

clarity around the specific green outcomes or standards we as a community require

the integration of these required outcomes into planning instruments and, where applicable, other legislative and regulatory requirements

a step-up in funding of green infrastructure, to ensure required outcomes can be delivered and funded over time.

The clock is ticking. With climate change, higher levels of population and development, and increasing urban encroachment on the natural environment, there is an urgent need to improve the supply of green infrastructure in many cities. In particular, it needs to be planned, delivered and truly integrated with development and other forms of infrastructure, rather than being supplied as an afterthought (as often seems to be the case).

Western Sydney, for example, is continuing to undergo significant development via the Western Parkland City initiative. Green infrastructure is critical to ensuring this new region is productive, liveable and sustainable. Failure to adequately plan, integrate, fund and deliver green infrastructure would consign future generations of people living and working in the Western Parkland City to missing out on the substantial benefits that flow from green infrastructure.

Below we outline some important steps for turning the vision for green, highly liveable urban areas into reality.

Providing certainty that there are enduring and sustainable funding frameworks ahead of investment occurring is crucial

A range of stakeholders including developers, utilities and various levels of government will be involved in planning, funding and delivering critical green investments in our cities.

Providing certainty to these stakeholders ahead of investment and development occurring that there are sustainable frameworks for funding green infrastructure is crucial for ensuring this infrastructure is delivered effectively and efficiently.

Clear and certain funding frameworks can ensure that:

Efficient signals are sent as to the cost of providing these services ahead of development occurring, creating certainty for developers, landowners and affected communities.

Investments occur in a way and/or timeframe that gets the best value from existing and new infrastructure (say by preserving corridors, integrating green infrastructure with other forms of infrastructure, or by making higher cost investments today that are more resilient over the longer-term).

Local governments are in a position to retain and enhance the capabilities required to deliver much of this investment, as well as monitor performance outcomes.

Funding pathways meet community expectations that impacts are fair, equitable, consistent and create competitive growth areas.

We need to be more specific in defining required green outcomes

Government policies and city plans often set out general or high-level objectives or targets for amenity and improved environmental outcomes. However, greater clarity is often required about the specific environmental, amenity and other green outcomes we want and need as a community.

Such green outcomes (or standards) should be set after robust analysis of their economic, social and environmental costs and benefits, and the costs and benefits of alternative outcomes.

The Australian Productivity Commission’s 2020 Research Paper on Integrated Water Management – why a good idea seems hard to implement

The Commission noted that City Plans recognise the importance of green open spaces for community health, well-being and urban cooling, but they often only include high-level ‘motherhood statements’.

It cited a lack of clear and precise objectives (and subsequent allocation of responsibility and accountability) for urban amenity and enhanced environmental outcomes as a key impediment to investment in integrated water cycle management.

It stated that until high-level aspirations are turned into more precise objectives, there is not a strong basis for normal project (and hence funding) assessment processes. These processes typically begin by identifying a specific problem that needs to be solved or objective that needs to be achieved, and then involve identifying and evaluating options to solve this problem or achieve the required objective at least net cost or greatest net benefit.

The NSW Productivity Commission’s 2020 Review of Infrastructure Contributions in NSW

The NSW PC found that, in terms of local infrastructure for new development areas, roads and drainage often take precedence over amenity and open space when funding is short. This is because the former are often considered ‘essential’ to unlock development. The implication being the latter is often considered discretionary.

The NSW PC also found that current open space standards for new development are outdated.

In Australia, both the NSW and Australian Productivity Commissions have recently recognised that a lack of clarity around required green outcomes can act as a significant impediment to adequate funding of green infrastructure and hence achievement of green outcomes.

Greater clarity around required green outcomes would focus attention on how we as a community achieve these outcomes, including the specific governance, regulatory and funding arrangements that are required. In particular:

who is responsible for achieving these outcomes

how these outcomes are best achieved

who should pay for these outcomes.

Integrate specific green outcomes into planning and regulatory instruments

Once required green outcomes have been determined, they should be integrated into relevant policy documents, planning instruments and, where applicable, other legislative and regulatory requirements.

This should assist in putting green infrastructure on an equal footing with traditional or ‘grey’ infrastructure and help to ensure that green infrastructure is considered upfront and integrated with development and other forms of infrastructure rather than provided as an afterthought.

This upfront consideration of required green outcomes, and hence integration of green infrastructure with other forms of essential infrastructure (e.g., transport, water) can be particularly important for efficiently achieving amenity and environmental outcomes.

The Australian Productivity Commission has noted that water infrastructure, for instance, can offer opportunities for enhancing urban amenity and environments (in addition to the traditional water and wastewater services that it provides). For example:

stormwater management assets can provide recreational lakes or wetland habitat

water easements and natural waterways can become corridors for recreation and habitat

water systems can provide fit-for-purpose water to support greenery and open space (such as providing recycled wastewater or harvested stormwater to irrigate public open space).

Similarly, the NSW Productivity Commission has observed that more efficient delivery of open space “will be achieved by shifting to performance-based benchmarks and a requirement to consider efficient land needs during the strategic planning process. This could, for example, include the dual use of land around creeks for both drainage and passive open space.”

Establishing sustainable funding sources for green infrastructure

There are strong economic efficiency and equity reasons for allocating the costs required to achieve green outcomes to those in the community that create the need to incur the expenditure (i.e., ‘impactors’) and/or those that benefit from this expenditure (‘beneficiaries’). In some instances, however, it may not be possible or practical to recover costs from specific groups of impactors or beneficiaries, in which case the broader community (taxpayers or ratepayers) may have to pay.

Clarity about required green outcomes is an important step in determining who is creating the need to achieve, or benefiting from, these outcomes, and therefore in establishing secure and sustainable sources of funding for green infrastructure.

If, for example, specific green outcomes are required to service or accommodate a new development (e.g., in relation to open space, waterways management, etc), which would not be required in the absence of that development, the local council should have a mandate to require developers to fund the capital costs of supplying green infrastructure for the development to achieve these outcomes– along with other essential infrastructure routinely funded or provided by developers for new development.

Similarly, if a water utility whose prices are regulated was required by its operating licence or similar regulatory instrument to meet specific green outcomes (e.g., in terms of stormwater and waterways management), then it should have assurance that it would be able to recover its costs, via its prices to its customers or charges to developers, of delivering servicing solutions that efficiently achieve these green outcomes. Notably, it would not likely have the same level of assurance, and hence funding certainty, if its statutory green objectives/requirements were less well defined.

Where it is appropriate for government to fund green infrastructure (on behalf of the broader community), greater clarity about required green outcomes can:

provide a stronger impetus for such funding – to ensure the outcomes are achieved

enhance transparency around the effectiveness and efficiency of such funding, and

help ensure that such funding is targeted to achieve the specific required outcomes, so that the taxpayer gets the ‘biggest green bang for his or her buck’.

Greater clarity about required green outcomes can also enable us to better assess the adequacy of existing funding mechanisms in meeting the scale and pace of development and investment required.

Where to from here?

Providing greater clarity about required green outcomes (or standards) can be challenging. However, it is important for improving governance, regulatory and funding arrangements for green infrastructure, and necessary if these green outcomes are to be achieved.

Along with best-practice regulatory design principles, valuation of the full costs and benefits to society of the environment and amenity outcomes related to green infrastructure can play an important role in both setting these outcomes and in assessing the range of options available to achieve them. As we discussed in a previous bulletin, there are a range of techniques that can be employed to undertake such valuation.

Thermal waste-to-energy involves converting residual waste into electricity, typically through direct combustion or high temperature gasification. It promises to put rubbish to good use – reducing greenhouse gas emissions by diverting waste from landfill and offsetting electricity generation from the grid. However the reality is not that simple.

The analysis of thermal waste-to-energy emissions is often assumption driven, and fails to accurately account for extensive energy capture at modern landfills and major changes already underway in the waste and electricity sectors. Well intentioned policy, supported by inaccurate analysis, risks unneccesarily locking in high emissions in the waste sector for decades to come.

In this bulletin, we explore the drivers of waste to energy emissions and consider how the trade offs between landfill energy and thermal waste-to-energy will likely change over the next ten years.

To download this publication, click the button below.

Thermal waste‑to‑energy is the process of converting rubbish into electricity, typically through direct combustion. It promises to reduce emissions by killing two birds with one stone – diverting waste from landfill and offsetting high emissions electricity generated in the grid.

Several large waste‑to‑energy projects have been supported recently, partially based on their promised emissions reductions.

Unfortunately, it isn’t that simple. Frontier Economics recently investigated the potential emissions from thermal waste‑to‑energy, looking closely at two recently approved projects in Western Australia and Victoria. We found that the analysis of thermal waste‑to‑energy emissions often depends on three faulty assumptions:

That waste‑to‑energy will forever offset electricity produced by the highest emissions alternative – either black or brown coal

That the alternative to thermal waste‑to‑energy is to dispose waste in a landfill with poor gas capture and zero energy recovery

That the composition of waste won’t change over time, despite plans for widespread introduction of green waste diversion.

These assumptions aren’t true today, and will become even less accurate over time.

We found that thermal waste-to-energy risks locking in unnecessarily high emissions for the long‑term despite changes in the electricity and waste sectors that should make emissions reductions possible. Well intentioned policy, supported by faulty analysis, can easily lead to poor environmental outcomes.

Ensuring secure, reliable & cost-effective management of the water cycle is critical to support economic growth & to meet community’s growing expectations for liveable & healthy environments.

Urban population growth, climate change and interdependencies between infrastructure systems are placing significant pressure on ageing water-related infrastructure, and the health of our waterways, environment, and people. However, their impact and the appropriate policy, regulatory and investment response is uncertain.

In this context, a challenge for decision-makers is to identify resilient and flexible decision-making pathways, which are well placed to respond to uncertainty and change. Economic tools and techniques such as adaptive pathways (or real options) analysis builds on cost benefit analysis to value this flexibility, by modelling costs and benefits of responding (or not responding) to new information in future. Decision-makers can then compare the value of flexibility to the cost of the investment, and more importantly, accurately compare the costs and benefits of different options. This is extremely valuable information when making critical decisions about significant infrastructure investments.

While engineering and planning expertise in adaptive infrastructure already exists across the sector, robust approaches to placing an economic value on that flexibility and using economic analysis to explore maximum value infrastructure pathways under uncertainty is an underutilised decision-making tool.

The Australian Government is currently implementing a mandatory news media bargaining code. This will fundamentally change the commercial relationships between digital platforms and certain news organisations. It will require that digital platforms - initially Google and Facebook - bargain with news media over remuneration for news content on Google and Facebook’s services.

In this bulletin, we consider some of the complexities of the code, and the challenges in finding the kind of bargains the Government is hunting for.

The news bargaining code will soon become law

The mandatory code follows from a lengthy, detailed ACCC Digital Platforms Inquiry and from the follow-on consultation processes by Government (Figure 1). The code’s bargaining framework is on track to become operational in March 2021.

The code is built around bargaining and compulsory arbitration provisions, but also provides for contracting “around” the code through individual negotiations and standard agreements.

Intervention is based on differences in bargaining power

The ACCC in its Inquiry recommended a code (initially voluntary) to address bargaining power imbalances between major digital platforms and media businesses. The imbalance is said to stem from these platforms being “unavoidable trading partners” for news publishers.

Figure 1: Progress of reforms on news media and digital platforms

(Download full report below for larger image)

Digital platforms use news content by linking (or allowing links) to news items on their services, including previews or snippets. This allows digital platforms to maintain the attention of their users, and so increases their ability to sell “eyeballs” to advertisers. Historically, the digital platforms had not paid the content generators in Australia (i.e. the Australian news media) for the use of these links.

The ACCC’s interpretation was that news media lacked the bargaining power to seek payment. The lack of power comes from the different consequences from news media withholding supply of news. Withholding hurts both parties, because it makes the digital platforms less useful and reduces click-throughs to news media sites. However, the argument is that withholding makes individual news media entities relatively worse off than the larger digital platforms because those platforms have a wide variety of sources for news links.

The argument then goes that this inability to seek payment has reduced news media’s ability to fund the production of news. The Government has supported the ACCC’s position - and identified it as a particular problem - because news has special public interest characteristics in a democracy.

Designated digital platforms

The responsible Minister will designate digital platforms and services to which the mandatory code applies. The stated intention is to designate Google’s search services and Facebook’s news feed service. Apple, through its News platform, is the next most obvious candidate.

The designation provisions have two main points of interest.

The first point of interest is that there is only one criterion against which platforms are to be assessed. This is whether the Minister considers there to be a significant bargaining power imbalance between Australian news businesses and the digital platform.

Because the bargaining code imposes compulsory participation for platforms, the bargaining code is quite different from the hotly-contested Part IIIA access regime process for the declaration of nationally-significant infrastructure services. The criteria in the Part IIA access regime (Figure 2) are challenging to satisfy, facilitating compulsory access only where declared services use a natural monopoly facility and access would promote competition in a dependent market.

The second point of interest is that there are no substantive rights of appeal on application of the provisions. Again, this is at odds with other forms of economic regulation such as Part IIIA. However, this lack of rights to appeal is – unfortunately – becoming an all too common feature of economic regulation in Australia.

Figure 2: Comparison of criteria for mandatory bargaining and mandatory access to services under Part IIIA

(Download full report below for larger image)

The designation provisions also take a different approach to that which is to be applied in regulation of digital platforms in Europe and the United Kingdom. These proposals – which are not directed at bargaining with the news media specifically – focus on designating platforms through either quantitative criteria relating to business size (EC) and/or the presence of entrenched market power (UK).

Challenges of numerating news remuneration

The proposed bargaining code requires bargaining over the supply of news content to a digital platform. The code does not require any particular payment, but provides a framework for negotiation for payments.

If parties cannot agree on a payment, it is backed by access to "final offer" arbitration. The arbitral panel must accept one of the two offers, unless it considers that the final offers are not in the public interest, in which case the arbitral panel may amend the more reasonable of the two offers.

The economic issue of suitable compensation is a particularly thorny one.

Economics tells us that voluntary exchanges create value to the buyer and seller. How the value is divided between the parties that create it is a function of their bargaining power. The price that is agreed determines how this division of value occurs.

The current system effectively has a zero price - that is, the platforms use links to news content at no charge. That sounds like the digital platforms have all the bargaining power.

However, there is no fundamental rule that the price agreed in the absence of bargaining power would always be positive. That is, a publisher might pay a platform to host a link if the platform is highly valued – publishers pay so that consumers can click through the link to the publisher's website which is then monetised via advertising, subscription or other commercial purposes.[i] It is also conceivable that platforms and news both create value for each other (Figure 3) – which leaves an arbitral panel to determine the “net” flow of value between the parties.

Figure 3: Who pays whom?

(Download full report below for larger image)

The code guides the arbitral panel “to consider the outcome of a hypothetical scenario where commercial negotiations take place in the absence of the bargaining power imbalance.” Modelling hypothetical scenarios is very complex, and in similar circumstances, price-setters typically look for benchmarks for prices.[ii] But are there any benchmarks where prices have been agreed without (a strong degree of) bargaining power?

Digital discord

Google and Facebook’s arguments against the code vary. Google has stated that it supports the principle of a code and has deployed its own news contribution model outside of the code which has signed up publishers in Australia and overseas[iii], but has three key issues with the current proposals:

the uncertainty over the broadness and vagueness of the definition of news

the arbitration process, which Google suggests is one sided and encourages unreasonable offers

requirements to notify news publishers of changes to algorithms, which are not provided to other parties.

Facebook has stated that the code compels it to pay for news content in a way that is not connected to commercial reality, including encouraging ambit claims. Facebook suggests it is effectively compelled to acquire all news content at whatever price is determined.

Agreement or arbitration?

It is difficult to predict how the bargaining code is likely to perform in practice, and, in particular, how well it will achieve its main goal of encouraging commercial negotiations to increase the flow of funds to Australian news media.

There are certainly significant penalties for not bargaining in good faith – as much as 10% of annual turnover. However, as with any new law of this kind, significant uncertainties remain. For example, it appears that the code allows for compulsory price determination without actually requiring digital platforms to provide access to their platforms at all. This has raised the spectre of Google removing search functions and Facebook removing news links posted on its platforms.

The Government has remained unmoved by such possibilities, maintaining faith that bargains will be struck, and has made significant provision for those bargains to occur outside of the code itself.

In our experience, firms do not like the risks associated with (highly) uncertain arbitration outcomes. This would favour settling. On the other hand, the uncertainty in the law may favour one side thinking it can get a bargain in arbitration.

At the time of publication, the situation is by no means settled. The forthcoming weeks and months will be closely watched by digital platforms, news media and policy makers alike.

Postscripts

Update– 18/2/21

Google’s and Facebook’s activities in the last few days have revealed very different approaches to the forthcoming parliamentary assent of the mandatory news code.

Google has settled payments with most of the larger Australian news media organisations, including a global deal with News Corporation. These deals are not subject to the mandatory code, but have been struck with knowledge of the major provisions as drafted.

Facebook has elected to prevent users including news media from sharing local and international news content on its website. Facebook has again reiterated its key concerns with the code, and identified the difference between itself and Google: that Google Search is inextricably intertwined with news and publishers do not voluntarily provide their content. Facebook suggests that publishers willingly choose to post news on Facebook, as it allows them to sell more subscriptions, grow their audiences and increase advertising revenue.

In terms of Figure 3, Google appears to be accepting that it is closer to the left end– that content keeps the user on Google’s services and helps it sell advertising (platform pays publisher). Facebook sees itself as more to the right, in that it helps publishers at least as much as Facebook benefits (meaning no payment, or publisher pays platform).

The early signs are that the code has delivered on its promise of a significant shake up in the funding of news in Australia – but not necessarily delivered all of the bargains the Government was hunting.

Update – 24/2/21

The Government has now moved amendments that address some of Facebook’s concerns with the code. This includes that the Minister’s designation decision should take account of whether the platform has made a significant contribution to the sustainability of the Australian news industry; that there be a compulsory mediation process prior to arbitration; and that more notice be given of a platform designation.

In exchange for the changes to the code, Facebook will restore links to Australian news content. Facebook has committed to entering into good faith negotiations with Australian news media businesses and seeking to reach agreements to pay for content. Seven West Media became the first Australian media group to agree to a commercial arrangement with Facebook.

The effect of the changes to designation makes it more difficult for the Minister to designate a platform service. Potentially, a platform could use the existence of a number of agreements with news businesses to argue against designation where a platform is in dispute with a single news business. However, the additional designation criterion offers little in the form of a clear or quantitative threshold.

Notes:

[i] For example, ad-based content recommendation platforms Taboola and Outbrain work in this fashion.

[ii] At least in concept, similar issues of value have arisen in disputes around copyright and in retransmission of free-to-air broadcasting signals that benefit both television networks and pay TV providers. In Australia, the Australian Copyright Tribunal has made a number of determinations on the equitable remuneration that pay TV supplier Foxtel should pay to free-to-air networks for retransmission of broadcasts. The Tribunal adopts the hypothetical bargain approach but this has not led to simple or agreed methods of price determination. See Audio-Visual Copyright Society Limited v Foxtel Management Pty Limited [2012] ACopyT 1.

[iii] Google has struck agreements with smaller publishers including the Conversation and Crikey, and has announced agreement with Seven West Media on 15 February 2021. Google also recently announced an agreement with French publishers.

We use cookies to ensure that we give you the best experience on our website. By continuing on this site, you are agreeing to our use of cookies.OKPrivacy policy