Whilst road pricing has been a hot topic in recent months in various states across Australia, the evolution of charging commuters for roads across Australia’s has been a long series of developments. With many challenges to defining how to charge commuters – including competing priorities and governance, and new technology such as EV’s, we unpack this topic below.

The challenges to tackling road pricing

Road pricing has made its way into the news recently for a number of different reasons.

Firstly, in 2021 the Victorian government introduced the Zero and Low Emission Vehicle (ZLEV) charge which levied electrical vehicle owners 2.8c for each kilometre they travelled. The intent was to charge EV users for the costs they impose on Victoria’s road network.

However, in October the High Court of Australia ruled the charge invalid, as it amounted to an excise duty, which under the Constitution, can only be levied by the Commonwealth.

Secondly, in the last year the NSW Government also announced the Independent Toll Review. This has come about because of emerging public concerns about the affordability of current tolls on Sydney motorways, particularly given the rising cost of living. Concerns have been accentuated by the inequities in tolling, whereby some motorists on their daily commute face quite significant charges, while other motorists in Sydney, pay very little.

The Independent Review has released a discussion paper which considers the efficiency and fairness of existing tolling arrangements that are set out in PPP contracts with road concessionaires.

The challenges posed by toll roads are merely a subset of the broader issues in road user charging. Whilst governments think that users should pay more directly for roads, developing a comprehensive set of road prices that applies across Australia’s road network is challenging.

Frontier Economics’ has been providing economic consulting advice in the transport sector – and on the development of road user charges – for many years. Here, we unpack the challenges of road pricing and discuss a possible path forward.

Why is pricing road use challenging?

Our Local, State and Federal governments are entering into a challenging space when it comes to the pricing roads. There are multiple reasons why pricing road use is challenging:

Firstly, there are multiple objectives to consider when pricing roads which are sometimes conflicting. Road charges can:

Fund the development or expansion of a new motorway – as is the case with tolls.

Be used to recover the ongoing costs of maintaining or operating the road network more generally – by accounting for the wear and tear vehicles impose on the road pavement, or

Help manage congestion and reduce emissions – by encouraging better decision making when it comes to reducing vehicle use; to limit these third-party costs.

The second reason is that we have Local, State and Federal Government roads. This creates challenges because you immediately have multiple governments involved, and we have motorists travelling, potentially in one trip, on multiple roads that are owned by different governments. The charging arrangements for that entire network therefore becomes far more complicated.

The final layer to this is that is that different governments have different powers in respect to vehicles, vehicle use and charging. The Federal Government has responsibility for the importation and design of new vehicles, and the power to levy the fuel excise, which is often argued to be the main mechanism for implicitly funding the road networks. The State Governments are far more confined in their ability to levy state-based road charges, however, they are in charge of things like registration. So, this limits the ability for any one government to create a comprehensive charging structure on its own.

Electric Vehicles (EV) and road charges

It’s necessary for all governments to consider a reformed approach to road pricing now, because of the emergence of Electric Vehicles (EVs) – who don’t pay the fuel excise. And currently the main mechanism used to implicitly fund road development is this fuel excise. This funding is expected reduce over time, as more motorists take up EVs. Essentially, motorists will be using less fuel, and as we use less fuel, this funding source will disappear.

The time to deal with this is now. Solving this problem means moving away from current arrangements which is challenging. States, such as Victoria, have tried to go it alone by implementing road use charges for EV. But this approach has been struck down in the High Court Challenge. So, you can see states acting on their own isn’t really a great option.

What can be done to create fairer and more efficient road pricing

The first step is to acknowledge that road pricing is an issue across governments and one that might benefit from intergovernmental co-operation. An intergovernmental agreement could be developed, that sets out:

Principles for pricing – what governments are hoping to achieve with different road use charges to deal with the problem of multiple objectives, and

The role of different governments in this charging space. So, we don’t get competing actions – which tends to happen in part because different governments are all not empowered to act on their own.

Some pricing improvements for heavy vehicles have already been achieved. It’s been a slow process with incremental improvements but there is no reason why that process, which we have been heavily involved for the last 15 years with can’t be expanded.

Given the outcomes of the High Court Case, governments need to work together on this emerging issue, and a better, intergovernmental, solution is required if we are to create road charges that are more efficient and fair for all motorists across Australia.

Frontier Economics' Tim McNamara, Mike Woolston and Dinesh Kumareswaran were commissioned by the Water Services Association of Australia (WSAA) to produce the report Understanding Efficiency to explain in "plain English" the concepts of economic efficiency and how they apply to the water sector. The report also illustrates what efficiency looks like under different scenarios using examples from the water sector and detailed case studies. Below is the Executive Summary of the report.

About this report

The aim of this report is to explain in ‘plain English’ the concepts of efficiency and how these are utilised within businesses, by economic regulators and others to assess service and expenditure proposals in pricing submissions and business cases.

Efficiency in the urban water sector

It is important for businesses to be able to understand and demonstrate efficiency, not just to get approval of pricing submissions from regulators – but also to demonstrate they are providing value for money to customers, owners, and other stakeholders.

Common or dictionary definitions of ‘efficiency’ tend to focus on the relationship between inputs and outputs of producing a good or service, but this narrow interpretation may lead to misconceptions. Minimising costs may not necessarily be consistent with providing customers’ desired service levels, maintenance and investment in asset capability and supply resilience, or delivering broader outcomes which are desired by customers or society.

Rather, economic efficiency can be seen as synonymous with value for money - providing the services customers want at the lowest long-term cost. The regulatory frameworks applied by most economic regulators do provide for broader ’value for money’ outcomes in assessing efficiency.

Some common misconceptions about efficiency

There are a number of common misconceptions about demonstrating efficiency in the urban water sector. These related misconceptions include:

Efficiency means prices need to be flat or declining

Efficiency is about cutting costs to the minimum

Efficiency is incurring lowest possible costs over the upcoming determination period

Efficiency means providing services at the lowest possible standards consistent with regulatory and other obligations

Efficiency is about deferring new investment as long as possible and running assets to fail

Efficiency means minimising costs even if this leads to higher risks

Efficiency means neutralising the impact of other drivers of expenditure (e.g. growth) so prices remain constant overall without having to disaggregate the drivers

Efficiency means demonstrating on a once-off basis that a business is efficient relative to the industry standard.

A common thread underlying these misconceptions is that ‘efficiency’ is synonymous with cost minimisation. Not only is cost minimisation in itself not an appropriate objective - but it is not an appropriate interpretation of what it means to be ‘efficient’.

Minimising costs may not necessarily be consistent with:

providing services at the level customers want

maintaining and investing in asset capability and supply resilience

delivering broader outcomes which are desired by customers or society.

How is efficiency measured and demonstrated?

While how best to demonstrate efficiency may depend on the audience, fundamentally it is about demonstrating that a proposal is in the long-term interests of customers.

The overarching approach of economic regulators in determining efficient levels of expenditure for regulated urban water businesses, which they then allow to be recovered in regulated prices, typically involves:

Establishing the services to be provided to meet regulatory and other obligations and customers' preferences

Establishing the minimum expenditure needed to efficiently deliver these services

Setting prices which are forecast to enable the business to recover the total expenditure which the regulator has deemed to be 'prudent and efficient'.

Typically regulators adopt a ‘prudency and efficiency test’ to provide assurance that the businesses are (1) doing the right things; and (2) doing those things as efficiently as possible.

Regulators typically assess the prudency and efficiency of operating and capital expenditure individually, as well as the trade-off between these two types of expenditures:

While both detailed ‘bottom up’ assessments of various operating expenditure items and broader ‘top down’ approaches which focus on broad categories of expenditure have been applied by regulators, the latter (particularly the base-step-trend approach) is becoming increasingly widespread.

Approaches to assessing the efficiency of capital expenditure typically examine the business' capital governance frameworks, policies and procedures, and review a sample of the business's proposed capital expenditure projects. This generally requires reference to an identified need or cost driver, evidence that the business has considered alternate solutions including non-network solutions, and that the cost of the defined scope and standard of works is consistent with conditions prevailing in the relevant markets.

What lessons does recent regulatory experience provide?

We examined a number of recent regulatory reviews and decisions by state economic regulators. This provided a number of key insights and lessons that can be drawn upon for future periods.

The Base Step Trend methodology is being adopted by a number of water regulators

Capital projects exposed to uncertainty have the potential to be deferred to future periods

Willingness to pay studies are helpful but should not be used in isolation to justify expenditure

Consultation and analysis is required to demonstrate the prudency of projects

The introduction of new services needs to predominately benefit customers

Capital expenditure proposals should be supported by robust business cases

Regulators often require alternative options to providing the service to be considered.

Guidance for demonstrating efficiency

We have identified some overarching guiding principles that should be adopted to demonstrate the efficiency of expenditure proposals regardless of the context in which efficiency is being measured or demonstrated:

Adopt a business case (or cost-benefit analysis) approach to all expenditure proposals

Focus on the long-term interests of customers, considering factors including operating and capital expenditure trade-offs and the impact on service standards over time and supported by Net Present Value NPV (analysis)

Consider both prudency and efficiency of expenditure, including how cost proposals incorporate efficiency targets and continuing efficiencies (as would occur in a competitive market)

Explain trends in operating and capital expenditure and key drivers of these trends

Develop a narrative that explains the link between expenditure and outcomes for customers

Conduct analysis that is proportionate to the size and impact of the potential expenditure.

However, there is no single methodology or technique that is appropriate to use in all circumstances to measure and demonstrate efficiency. The appropriate approach may vary depending on factors such as the nature of the:

expenditure (i.e. operating vs capital expenditure or large ‘step’ in operating expenditure)

activity (discretionary vs non-discretionary expenditure).

Table 1. Approach to demonstrating efficiency - a guide

Step

Type of expenditure

Evidence/

data required

Techniques

Example

Outline why the spending is in the long-term interest of customers

All

Link spending to specific outcomes for customers in terms of services and prices over the long term

Clear ‘golden thread’ narrative

Investment Logic Mapping

See section 4.2 and 5.5

Prudency: Link spending to non-discretionary obligation

Non-discretionary

opex & capex

Identify key drivers including relevant legislative or regulatory obligations

Understanding of non-discretionary service (and related) outcomes, including their timing

Central Coast Council (section 3.3.3)

Prudency: Demonstrate that customers want the proposed service/level or outcome

Discretionary opex & capex

Customer feedback

Surveys, customer forums

Case study 2

Prudency: Demonstrate that customers are willing to pay for this service

Discretionary opex & capex

WTP studies

Choice modelling

Case study 2

Analyse a range of options to produce the desired outcome

All

List of alternative options including capital vs recurrent solutions – ideally in business case

Frontier Economics' Stephen Gray was commissioned by Vector to assess whether the draft Input Methodology decision by the New Zealand Commerce Commission will help or hinder the investment that’s needed to decarbonise the economy. The New Zealand Commerce Commission is currently developing a final decision over the key regulatory principles that bind the way electricity networks in Aotearoa New Zealand can operate and invest for the next seven years, and possibly longer (the Input Methodologies, or IMs).

In this video below, Stephen shares his view on how the IMs could support the network investments needed to deliver New Zealand’s energy transition to net zero by 2050.

Electrification is at the core of New Zealand’s decarbonisation strategy, and this will require extensive investment in transmission and distribution networks over a short period of time. Indeed, it will be impossible for New Zealand to meet its decarbonisation commitments without this extensive network investment.

Moreover, there is widespread agreement that investment in electricity networks today will secure long-term benefits for consumers. So it is important that New Zealand’s regulatory framework helps to facilitate the network investment that is required. However, there is a real risk that the current regulatory framework will, in fact, hinder major network investment projects.

The key problem is that the regulatory cash flows tend to be back-ended, creating a risk that the cash flows in the early years of a project’s life are not sufficient to support the credit rating and gearing that the regulator has assumed. Where this happens, a project is not commercially viable and does not proceed. And, of course, no consumers receive any benefit from a project that does not proceed.

Our analysis found the draft Input Methodologies do not contain the sort of ‘financeability’ test that regulators in other markets employ. Nor do they provide potential investors with certainty about how a financeability issue would be addressed if it was identified.

A process to ensure that the regulatory cash flows are sufficient to support the credit rating and gearing that the regulator has assumed would remove a regulatory roadblock to the efficient investment that’s needed to meet the task of decarbonisation.

Extra for experts – a solution

A workable solution could be for the Input Methodologies to accelerate the allowed cash flows in a Net Present Value-neutral manner, as Stephen explains in this short video. The draft Input Methodologies decision canvassed several options to make this happen, of which the most promising was removing indexation of the Regulated Asset Base.

This excerpt was originally published in Vector's stakeholder newsletter.

Frontier Economics' recently advised a number of clients in relation to the Queensland Competition Authority's review of its approach to climate change related expenditure. Below are some highlights and commentary on our advice included in the final position paper.

ensure its framework for assessing the prudency and efficiency of climate change related expenditure is fit-for-purpose and capable of incentivising timely investment when such expenditure would promote the long-term interests of consumers; and

provide greater clarity and certainty to stakeholders—including consumers and regulated businesses—on how the QCA intends to assess future proposals related to climate adaptation and mitigation expenditure.

Economic regulators need to perform a difficult balancing act when assessing expenditure proposals related to managing climate change risks. The impact of climate change on regulated infrastructure (and, therefore, on users of that infrastructure) is fraught with uncertainty.

If regulators set a low threshold for the prudency of climate change related expenditure, then consumers may pay more than the efficient amount required to manage climate change risks effectively.

Conversely, if regulators are too conservative in their assessment of climate change related expenditure, that may imperil the reliability and safety of the infrastructure used to deliver regulated services. This, in turn, may expose consumers to significant economic losses.

Uncertainty over whether regulators will approve climate change related expenditure—or over whether recovery of such expenditure would be disallowed once it has been incurred—may deter regulated businesses from making prudent and efficient investments to improve the resilience of their networks.

Clear guidance about how proposals for climate change related expenditure will be assessed by regulators can help reduce this uncertainty and encourage prudent and efficient investments that may otherwise be foregone.

For this reason, other economic regulators, should conduct their own reviews and publish formal guidelines on how they intend to assess regulatory proposals for climate change related expenditure. The QCA’s guidelines are not specific to any particular industry or jurisdiction, so would be a relevant starting point for other regulators and regulated businesses beyond Queensland.

Managing climate uncertainty to invest prudently and efficiently in resilience

Of the many issues covered by the QCA’s review, our advice focussed on the development of a framework to assess the prudency and efficiency of climate change adaptation expenditure.

Below are some highlights:

We advised Aurizon Network that:

“In assessing prudent and efficient ex ante resilience expenditure the QCA should encourage regulated entities to pragmatically incorporate the uncertainty inherent in climate change related risks into their proposals for adaptation expenditure.”

In our report to DBI, we added:

“Climate-resilience should be a necessary condition to project prudency and efficiency. Investing in infrastructure that is vulnerable, by design, to an accepted range of climate-related risks is likely to be lower cost in the short term but higher cost in total over the life of the asset.”

We discussed the development of an upfront expenditure framework that could facilitate investment under uncertainty, providing advantages to both regulated infrastructure providers and their customers. That is, a framework which:

is ex-ante in nature;

relies on the justification for the proposed expenditure;

includes in its ex-post review mechanisms a consideration of uncertainties related to climate-related risk; and

is proactive in managing long-term demand uncertainty.

We considered that these elements together would promote regulatory certainty and facilitate investment in prudent and efficient levels of infrastructure resilience.

The Coal Effect – funding and financing approaches to address residual stranding risk

Fossil fuel exposed firms are exposed to transition risk, or risks arising from the process of adjusting towards a lower-carbon economy. This can impact forecasted demand, the value of assets and liabilities, and thereby the risk profile and viability of the regulated business.

A key driver of transition risk for coal exposed companies is policy change. Net zero targets, can reduce domestic demand for coal. However, targets vary in status, development and expected achievement date. This uncertainty, in combination with uncertainty around technological development and carbon abatement costs, makes future demand for coal similarly unclear.

We identified a scenario where Aurizon Network may support more adaptation expenditure to increase the resilience of the network (with the expenditure to go into the regulatory asset base). However, future customers may be unwilling or unable to continue to pay for past adaptation expenditure. These factors create asset stranding risk, which may disincentivise a regulated business from investing in network resilience today, even if the investments are supported by current customers.

We then considered options the QCA might adopt to address asset stranding risk. We discussed the merits of addressing an increased stranding risk associated with climate change via an uplift to the allowed rate of return (i.e., the ‘fair bet’ approach) that would be just sufficient to compensate investors for the increase in stranding risk.

Also considered was the use of accelerated depreciation, which has been used by regulators in Western Australia (ERAWA) and New Zealand (the Commerce Commission) to address the stranding risks faced by gas pipelines following the adoption of emissions targets that have shortened the expected economic life of those regulated assets.

In our advice, we recommended that the QCA should confirm clearly that:

its regulatory framework will continue to provide regulated businesses with a realistic opportunity to recover past prudent and efficient expenditure over the long term;

regulatory allowances will be set such that climate change related expenditure that is deemed to be prudent and efficient, based on information available at the time, may be recovered over the expected economic life of the assets; and

the expected economic life of the assets should be reassessed periodically as new information becomes available.

Overall, we identified the benefits in the QCA providing clear upfront guidance on the types of information and evidence it would require from regulated businesses, to demonstrate asset stranding risks and management responses.

This could include the QCA needing to take into consideration a larger range of plausible future scenarios, rather than focusing on just the expected future profile of demand at a given point in time, reflecting the long-term uncertainty faced by the coal industry.

Frontier Economics Pty Ltd is a member of the Frontier Economics network, and is headquartered in Australia with a subsidiary company, Frontier Economics Pte Ltd in Singapore. Our fellow network member, Frontier Economics Ltd, is headquartered in the United Kingdom. The companies are independently owned, and legal commitments entered into by any one company do not impose any obligations on other companies in the network. All views expressed in this document are the views of Frontier Economics Pty Ltd.

This bulletin explains why it is essential for regulators in Australia to adopt financeability tests as standard practice whenever they make a regulatory determination, and to take the results of those tests seriously.Financeability tests are used by regulators in the UK to assess whether the revenues they allow a business to earn over a price control period will be sufficient to finance the business’s operations efficiently. These tests act as an early warning against a regulated business becoming financially constrained or insolvent—an outcome that ultimately harms consumers, or taxpayers, who may be called on to rescue a regulated business providing essential public services from collapse.

By contrast, in Australia, regulators have either refused to employ financeability tests or run them but only pay lip service to the results.

A Case Study: The Thames Water ‘financeability’ problem

Thames Water is Britain’s largest water company, providing water and wastewater services to 15 million customers in London and the Thames Valley.

In late June 2023, alarming reports began to circulate that Thames Water was struggling to meet its debt obligations and may be on the brink of collapse. The crisis deepened as the CEO stepped down suddenly following criticisms about the company’s poor environmental performance and record leakage rates, and a new Chair was appointed hastily to regain control of the situation.

The UK Government and the water sector regulator, Ofwat, began drawing up rescue plans for Thames Water amidst fears that the company might become insolvent. The crisis ended when shareholders agreed to inject £750 million of equity capital into the business, to reduce its debt burden.

The media was quick to blame the financing decisions of the company’s private owners for its woes. Previous owners of Thames Water, including Australian bank Macquarie (dubbed the ‘vampire kangaroo’ by some in the British press), were accused of loading the business with excessive debt, while extracting huge dividends, leaving it unable to meet its financial obligations.

The Thames Water debt crisis

Thames Water is one of the most indebted water companies in Britain. At the time of the crisis, it had £16 billion of debt and a gearing ratio (the proportion of its assets that are financed with debt rather than equity) of around 80%. Ofwat noted that Thames Water (and some other companies) had “borrowed too much.”[1] This meant that the company faced large debt repayments.

The situation was worsened by the fact that nearly 60% of Thames Water’s debt was inflation-linked. That is, a significant portion of the interest Thames Water needed to pay was linked to the retail price index (RPI) measure of inflation. The RPI is similar to the consumer price index (CPI). However, it also includes mortgage interest payments, which makes it more sensitive to changes in interest rates. Hence, Thames Water’s interest bill grew significantly as inflation rose sharply over 2022 and 2023.

But the size of Thames Water’s debt obligations is only one part of the equation.

Inflation and the regulator’s revenue limits

As a natural monopoly, the amount of revenue that Thames Water is allowed to earn is capped through periodic price controls by Ofwat.

A part of that revenue allowance is an amount to cover real interest payments. However, to the extent that a company holds inflation-linked debt, its actual interest bill in each year will be the sum of a base (real) rate plus outturn inflation that year.

Ofwat allows the regulatory asset base (RAB) of the businesses to grow each year in line with actual inflation. Recovery of this inflation-indexed RAB, over 50 years or more, provides the business with compensation for the inflation component of its interest costs.

Herein lies a problem: the business is contractually obliged to pay the entire interest bill every year. But, it will take decades to recover through regulated prices the inflation component of that bill. When inflation starts rising, the mismatch between the business’s regulated cash flows in each price control period and its interest obligations widens.

In short, Thames Water faced a perfect storm: a large pile of debt, rapidly rising interest repayments linked to inflation, and regulated revenues that were insufficient to cover these increasing costs. All of this added up to material risk of default on its debt obligations.

UK regulatory financeability tests: an early warning system

“secure that companies...are able (in particular, by securing reasonable returns on their capital) to finance the proper carrying out of their functions.”[2]

If the annual revenue allowance set by Ofwat is insufficient to pay the business’s interest bill or to attract equity finance, the business will be unable to finance its activities properly or invest in assets. In these circumstances, the business would be unable to deliver services of proper quality to consumers.

Moreover, the financial collapse of essential service providers such as water companies, energy networks or communications firms can cause catastrophic disruptions and economic costs to consumers.

Recognising this, Ofwat and other UK regulators with similar financing duties have developed ‘financeability tests.’ These act as an early warning to detect whether the revenue allowances set by the regulator would be insufficient for an efficient business to remain financeable. If the tests show a likely deterioration in financeability, the regulator can adjust revenue allowances to avert the problem.

The purpose of Ofwat’s financeability test is to assess whether the revenue allowances set in this way are in fact sufficient to support that BBB+ rating at the benchmark 60% gearing. It is effectively a test of the internal consistency of the regulatory decision.

Thames Water argued that, even after bringing forward these allowed revenues, a benchmark business with 60% debt finance would be unable to finance the delivery of its statutory obligations or attract the required amount of equity finance. Ofwat did not accept Thames Water’s representations.

Ofwat also performed a separate test of ‘financial resilience’ based on Thames Water’s actual gearing (at the time) of 80%. Ofwat expressed concerns that Thames Water was very highly geared and noted the company should take steps to improve its financial resilience.

Under this two-pronged test:

Any problem found using the regulator’s benchmark settings is a problem of the regulator’s making and requires a regulatory remedy; and

Any problem that is due to the actual business departing from the regulatory benchmark is the responsibility of the company and its owners to fix. Consumers should not be expected to pay more for poor financing decisions taken by the business.

Australian regulators seem to prefer a late warning system

Whereas Ofwat and Thames Water differed in their views about whether the regulatory allowance was sufficient to support financeability, there was strong agreement that consideration of financeability is a vital component of regulatory best practice.

By contrast, Australian regulators have been slow to embrace financeability tests. Regulators in Australia fall into three groups:

Those that perform no financeability test at all;

Those that perform a test, but invariably conclude that no action is needed regardless of the outcome of that test; and

Those that perform a test and conclude that action is needed – but not by them.

The Thames Water case provides a timely reminder that even the largest and most well-resourced regulated businesses can face serious risk of insolvency, which can be disastrous for consumers. Properly implemented financeability tests can avoid such outcomes. Therefore, it is important to consider:

The essential features of a useful financeability test; and

The right regulatory responses to the outcomes of financeability tests. (Spoiler alert: The right regulatory response is not to always do nothing.)

Features of a good regulatory financeability test

Financeability tests are an essential element of best practice regulation

It is in the long term interests of customers that an efficient provider of essential services is financeable, so that it can provide services desired by customers. This requires that regulated revenues are sufficient for an efficient business to meet its financial obligations as they fall due and to invest what is needed to deliver regulated services.

If regulated businesses cannot provide their services because they are financially constrained or insolvent, then customers or taxpayers will bear the cost. If the regulated business is financially constrained, it may be unable to make the investments needed to provide the level of service today or into the future that customers want. If a regulated business becomes insolvent, then it will likely be taxpayers that step in to ensure the essential services continue to be provided.

This is why financeability tests are a key part of best practice regulation. The purpose of a financeability test is to ensure that the revenue allowance is sufficient for an efficient business to meet its financial obligations over the forthcoming regulatory period.

The test should also allow the regulator to diagnose the source of the problem, so that appropriate corrective action can be taken.

A two-pronged test is needed to determine appropriate action

Financeability problems can arise because:

The regulatory allowance is too low to support the benchmark financing parameters (gearing and credit rating) that the regulator assumed when setting that allowance; or

The regulated business has departed from the benchmark financing parameters (e.g., by adopting higher gearing).

The first is a case of internal inconsistency in the regulator’s process and is for the regulator to resolve. The second is a case of risky financing practices and is for the firm and its owners to resolve.

Regulated businesses should be free to depart from the regulatory benchmark if they choose. The business then keeps any benefits, and bears any costs, of such a departure. Neither the regulator nor consumers should be called on to immunise regulated businesses against bad outcomes arising from such decisions.

The Ofwat approach described above involves a two-part test:

The ‘financeability’ test is performed using the regulator’s benchmark financing parameters. The test provides an indication of whether the regulatory allowance is sufficient to support those parameters.

The ‘financial resilience’ test is performed using the firm’s actual financing parameters. It assesses whether the firm’s departure from the regulatory benchmark may be causing problems.

The source of any financeability concern can be identified more easily by using two separate tests:

If a regulated business fails IPART’s ‘benchmark’ test, that implies that the revenue allowance is too low to service what the regulator itself considers is the efficient debt obligation; and

If a regulated business fails IPART’s ‘actual’ test but passes the benchmark test, that implies that the business is not financially resilient due to its own financing choices.

Recent financeability test practices in Australia

There are almost no examples of Australian regulators taking action to address financeability concerns arising from their decisions to set inadequately low revenue allowances. Some regulators perform no test at all, so have no way to detect the existence of a problem. But, many that do perform financeability tests have chosen to take no action, even when the test has clearly identified a financeability problem.

‘Narrating away’ the outcomes of a financeability test

It is important that regulators acknowledge the outcomes of their financeability tests, respond consistently and do not try to apply a narrative that seeks to ‘explain away’ a potential problem.

IPART

The most important financeability metric considered currently by rating agencies for Australian regulated energy and water businesses is the funds from operations to net debt (FFO/Net Debt) ratio

In IPART’s 2020 determination for Sydney Water, the FFO/Net Debt ratio fell below of the minimum 7.0% threshold specified in IPART’s benchmark test in every year of the regulatory period. This suggested strongly a failure of the benchmark test. IPART should have adjusted Sydney Water’s revenue to ensure an efficient, benchmark business could remain financeable.

However, IPART concluded that the failure of the test on the FFO/Net debt ratio did not indicate a problem. This is because, amongst other reasons, that ratio was expected to improve over the regulatory period towards the target ratio (from 6.6% in 2020-21 to 6.8% in 2023-24). However, it would remain below the required threshold in every year.[4]

According to IPART, there was no problem to fix because the failure of the test was forecast to become less severe over time.

The AER’s test used the FFO/Net debt ratio as the sole metric and set a threshold of ≥7.0% for a ‘pass’.

The AER found that the FFO/Net debt ratio for 25% of the businesses fell below the threshold for a pass.

The AER concluded that there was no evidence of a financeability concern (at the industry level) under its proposed rate of return methodology because 75% of the firms appeared to pass the test.

Of course, this ignored the fact that a quarter of the industry had failed the regulator’s own test.[5]

Not adjusting regulatory decisions in response to a failure of the benchmark financeability test and instead narrating away the outcome is as good as having no test at all.

Applying the wrong solution to the problem

The regulatory response to a financeability problem should properly address the underlying cause of the problem. Without addressing the cause, remedial actions may be misdirected, leading to inefficient outcomes.

If the financeability problem was caused by the business taking imprudent or risky financing decisions (e.g., by gearing up more than the benchmark level), it should not fall to consumers to ‘bail out’ the business for those poor decisions. That would impose unnecessary costs on consumers and create poor incentives for the business to avoid bad financing decisions in future.

However, if the financeability problem was caused by the regulatory allowance being set too low for a efficient business to remain financeable, then the regulator, not shareholders, should fix the problem.

“If the source of the concern is that prices are too low even for a benchmark efficient business, we think the appropriate remedy is to review our pricing decision. In essence, this step would involve correcting a regulatory error. The financeability test could help identify any such error by applying additional information that may not have been available in the building block model used to set prices.

If the source of the concern is that prices are adequate for a benchmark efficient business but too low for the actual business because its owners have been imprudent or inefficient, there are appropriate remedies. The owners could reduce the business’s level of debt by injecting more equity, accept a lower than market rate of return on their equity, or both. It is an important principle that an inefficient business should not be rewarded for its imprudent decisions at the expense of customers.”[6]

The best way to diagnose the source of a financeability problem is to apply a two-pronged test of the sort used by IPART and Ofwat. Because the benchmark test assumes that the regulated business always finances itself efficiently and prudently, the only explanation for a failure of that test would be a regulatory error that requires correction.

Calibrating the financeability tests incorrectly

Even when a test is structured correctly, it will only be useful if it accurately reflects the financial flows of an efficient benchmark business. If the thresholds for passing the test are set unrealistically low, then genuine financeability tests will go undiagnosed and uncorrected.

For example, when running its benchmark test, IPART assumes that businesses faces real, rather than nominal, debt obligations. But, in reality, companies in Australia issue nominal debt and therefore must pay nominal interest expenses.

Assuming that an efficient regulated business faces lower (i.e., real) interest expenses than it in fact does makes IPART’s benchmark test too easy to pass. Hence, the test is prone to ‘false negatives’—i.e., conclusions that there is no financeability problem, when there is one.

Recommendations for improvements to regulatory financeability tests

These examples show that regulators in Australia either do not apply financeability tests at all, or if they do, typically find reasons not to fix a problem identified by their own financeability tests.

The Thames Water example is a reminder that regulated businesses can face serious financeability problems.

Ofwat concluded at the last price control that Thames Water needed an uplift in allowed revenues of £125 million to support an efficient credit rating, at an efficient level of gearing. The crisis that Thames Water faced would probably have been worse than it was, had Ofwat adopted the approach that Australian regulators follow and ignored the results of its own financeability analysis.

Because regulated businesses deliver essential services, it is consumers that suffer if these businesses become insolvent or financially constrained. In the case of insolvency, taxpayers may also be called upon to rescue the business from collapse.

Therefore, regulators in Australia should view financeability tests as an essential part of best practice and incorporate them as a standard feature into their revenue setting processes.

A good framework for regulatory financeability tests should:

Be able to identify the source of a financeability problem.

If the cause is imprudent or risky financing decisions by the business, it should be left to investors to deal with. However, a failure of a benchmark test indicates that the problem is a regulatory one. In these situations, the regulator should take action to fix the problem, rather than explain it away or shift the onus on shareholders.

A two-pronged test allows regulators to pinpoint the cause of the problem and ensure that tailored action is taken.

Be specified in such a way that the outcome—i.e., a ‘pass’ or a ‘fail’—can be identified clearly and objectively.

Regulators should take the outcomes of these tests seriously and not dismiss a clear failure of the test by simply assuming that their regulatory decision is adequate.

Be calibrated in such a way that the tests are realistic and capable of identifying, rather than masking, genuine problems.

Frontier Economics Pty Ltd is a member of the Frontier Economics network, and is headquartered in Australia with a subsidiary company, Frontier Economics Pte Ltd in Singapore. Our fellow network member, Frontier Economics Ltd, is headquartered in the United Kingdom. The companies are independently owned, and legal commitments entered into by any one company do not impose any obligations on other companies in the network. All views expressed in this document are the views of Frontier Economics Pty Ltd.

At the International Institute of Communication’s Telecommunications and Media Forum, Sydney 2023 our Economist Warwick Davis joined a panel on competition issues in the sectors and commented on proposed merger reforms in Australia and the United States. He suggested that the Australian Competition and Consumer Commission (ACCC)’s proposed reforms for processes and legal tests for merger clearance will be contentious but seem more likely to produce economic benefits than the proposed changes to merger guidelines in the United States. This note explains the reasons for his view.

Merger reform proposals are a response to increasing market concentration

Competition authorities in many parts of the world are steering the debate on mergers towards sterner enforcement. The recently released details of proposed changes to merger enforcement in Australia and the United States show that competition authorities are on quite different paths to achieve that goal.

In Australia, details of the ACCC’s proposals for merger reform, as provided to Australian Treasury in March 2023, were recently released under Freedom of Information laws.[1]

The US Department of Justice and Federal Trade Commission (the Agencies) issued new draft merger Guidelines[2] for comment in July 2023. As in Australia, merger guidelines do not have the status of law, but they have been influential in US court merger proceedings.

The proposed changes are different, but they are both reactions to similar concerns – perceived harms from increasing market concentration that have not been prevented by merger laws and/or enforcement practices:

There is growing evidence to support the view that Australian markets are becoming more concentrated…It is important that Australia’s merger regime is effective in preventing increases in concentration before they occur.[3]

and:

[In the United States] Empirical research…has documented rising consolidation, declining competition, and a resulting assortment of economic ills and risks.[4]

Proposed changes to US Merger Guidelines renew emphasis on market concentration

The Agencies’ draft Guidelines have undergone a substantial change in form and substance from earlier versions.[5] The draft Guidelines show the Agencies’ desire to simplify the analysis of mergers that increase concentration or occur in concentrated markets, tied where possible to legal precedent. The FTC Chair has stated the draft Guidelines do not rely on “a formalistic set of theories” but “seek to understand the practical ways that firms compete, exert control, or block rivals”, and offer several ways to analyse transactions.[6]

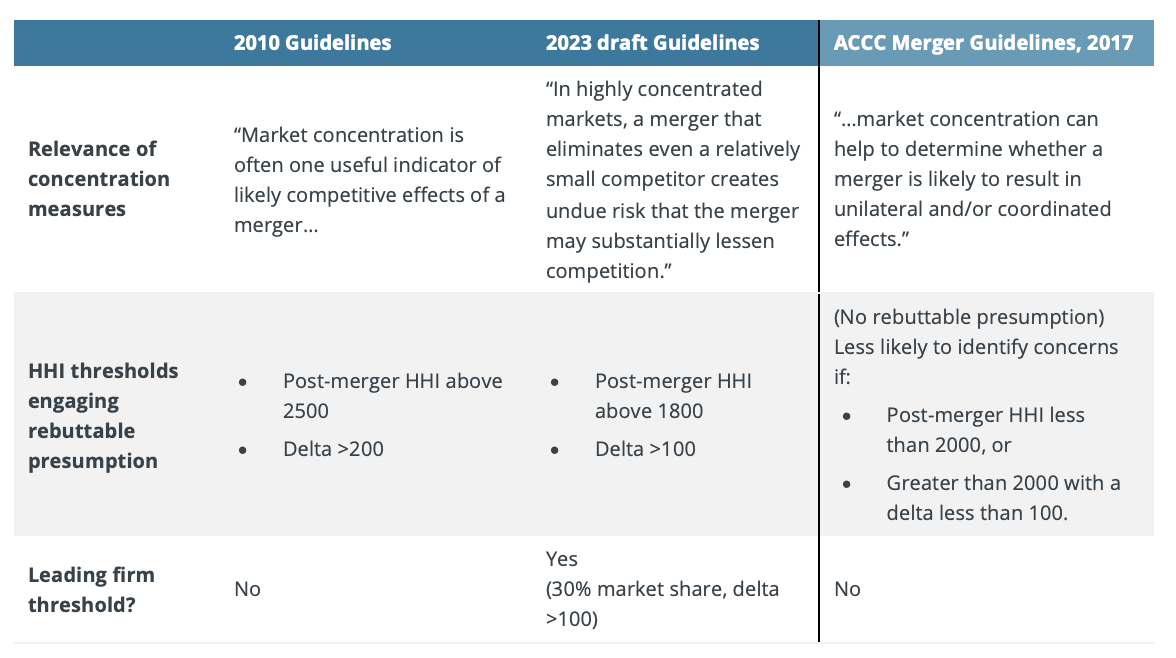

The draft Guidelines have 13 specific guidelines that address analytical frameworks and specific challenges relating to serial acquisitions (creeping acquisitions in Australian parlance), buyer power in labour markets, platform markets and minority interests. This includes a return (in Guideline 1) to a stricter application of the ‘rebuttal presumption’ of market concentration that was first developed by the Supreme Court in 1961[7], and the introduction (in Guideline 6) of a rebuttable presumption in the case of vertical mergers, where a market share of more than 50% is involved.[8]

The changes from the 2010 version of the Guidelines on the significance of increasing market concentration are stark, as highlighted in Table 1. The thresholds at which the rebuttable presumption is engaged are reduced: in rough terms, a 6 to 5 merger of equally sized firms would now be subject to the rebuttable presumption while under the 2010 version it would not. For reference, the current ACCC Merger Guidelines approach (2017) is also highlighted, but these thresholds do not create rebuttable presumptions but instead provide an indication of the likelihood of concerns being raised.

Table 1: Changes in treatment of market concentration, US DOJ/FTC Merger Guidelines

Source: US Department of Justice and the Federal Trade Commission, Horizontal Merger Guidelines, August 19, 2010, draft Guidelines, p. 6, ACCC Merger Guidelines, 2017.

Similar problems, but different responses in merger reforms

The ACCC also has expressed concern with increasing market concentration. But the ACCC’s proposed reforms do not specifically focus on elevating market concentration to a more central role in merger analysis. Rather, the key elements of the ACCC’s reform proposals include:

A formal merger clearance regime: large mergers could not go ahead unless a clearance was obtained from the ACCC or Tribunal.

Changes to the merger clearance test: mergers can be blocked by the Federal Court under section 50 if they have the effect or likely effect of substantially lessening competition. The ACCC proposes that a merger would be cleared only if the ACCC (or Tribunal, on review) is satisfied that it is not likely to have the effect or likely effect of substantially lessening competition.

Revisions to the section 50 merger factors: added factors include an emphasis on creeping acquisitions and entrenching existing market power.[9]

Concentrating on the right measure of competition?

We have previously suggested that the ACCC’s proposed changes to the process by which mergers are assessed, including formal merger clearance, are worthy of serious consideration. The changes would address defects in the current informal clearance regime and adjudication processes, particularly by empowering the ACCC to be the principal decision-maker and increasing the transparency of its decisions.

On the added measures, the proposed ACCC reforms are better for not aiming directly at market concentration, albeit that concentration will remain a significant element of merger investigations. This is for two reasons:

Since the 1970s, economists have grown more sceptical of the causal connections between market concentration, competition, and economic performance. Concentration is only one factor in competitive health, and other market structures and conduct factors can be equally or more important.[10] For example, product differentiation, which is relevant to most mergers in Australia, highlights that the identity of competitors, and the similarity of their products, can have a greater influence on the competitive effects of mergers than aggregate concentration measures.

So much emphasis on concentration places an undue reliance on the defined markets. The definition of markets is rarely clearcut, particularly where products are differentiated, and is inevitably a matter of judgement.

Striking the right balance on the cost of errors

The ACCC’s proposed changes to the section 50 legal test are likely to have a significant impact on the chance of contentious mergers being proposed and approved. Mergers that have uncertain effects would be more likely to be blocked than under the current system.

One framework through which to view the proposed changes is whether they minimise the total costs of decision-making errors:

from not blocking anti-competitive mergers, and

from blocking mergers that pose no threat to competition.

Compared with the existing legal test, the ACCC’s proposed changes will reduce errors of the first kind while increasing errors of the second kind. Both kinds of errors are relevant: while errors of the first kind harm consumers directly, blocking mergers that are pro-competitive will also harm consumers.[11] Undoubtedly, the balance of errors is complex to assess and we expect further debate over whether the proposed change restores or upsets the right balance.

Other proposals to structural merger factors seem more likely to be positive. The proposals focusing on accumulation of market power address long-standing concerns about creeping acquisitions but avoid placing increased weight on market concentration thresholds. This leaves more room for nuance in the merger analysis.

A step in the right direction

The ACCC’s proposals are a serious attempt to improve the processes and outcomes of merger reviews. Although the ACCC may be concerned about market concentration, it is helpful that the ACCC has not looked to tie its proposals directly to that concern – as is being pursued in the United States. While further debate on changes to the legal test is justified, we expect the ACCC’s proposed changes have reasonable prospects of improving competition and economic welfare.

[4] Remarks of FTC Chair Lina M. Khan, Economic Club of New York, July 24, 2023, p.3.

[5] The Agencies have amended the guidelines several times since the first guidelines were released in 1968, including in 1982, 1984, 1992, 1997, 2010, and 2020.

[6] Remarks of Chair Lina M. Khan, Economic Club of New York, July 24, 2023, p.2.

[7]United States v. Philadelphia Nat. Bank, 374 US 321, 363 (1961).

[8] Draft Guidelines, p. 17: “If the foreclosure share is above 50 percent, that factor alone is a sufficient basis to conclude that the effect of the merger may be to substantially lessen competition, subject to any rebuttal evidence.”

[10] For example, in oligopoly settings, common market features such as cost asymmetry between firms or economies of scale can reverse the standard intuition that increasing concentration reduces economic performance.

[11] The ACCC suggests that the increased costs of errors will be borne by the merger parties rather than the public. That would only be true if the merger produced no efficiencies or did not otherwise benefit competition.

Frontier Economics Pty Ltd is a member of the Frontier Economics network, and is headquartered in Australia with a subsidiary company, Frontier Economics Pte Ltd in Singapore. Our fellow network member, Frontier Economics Ltd, is headquartered in the United Kingdom. The companies are independently owned, and legal commitments entered into by any one company do not impose any obligations on other companies in the network. All views expressed in this document are the views of Frontier Economics Pty Ltd.

Should economic regulators pursue other objectives, such as equity and social justice, in addition to efficiency? The theme of the 2023 ACCC/AER economic regulation conference was ‘Beyond efficiency?’

Speakers during the conference’s opening plenary session were invited to explore whether economic efficiency should continue to be the sole objective pursued by the economic regulatory frameworks in Australia. Or, alternatively, should the remit of regulators be expanded to include other objectives besides efficiency in the name of tackling the major challenges of our time, including: climate change, technological disruption and digitisation, the transformation of services and business models, and the growing inequity in access to services and outcomes?

Some of the speakers at this session, and some conference delegates, were firmly of the view that it is now time for regulators to balance the pursuit of efficiency with other objectives, such as equity and social justice.

This bulletin presents a summary of the address given by Dinesh Kumareswaran, Director of Frontier Economics, during this first plenary session. Dinesh argued that regulators should pursue one objective, and one objective alone: the promotion of economic efficiency.

What is economic efficiency?

A common misconception is that efficiency means producing widgets at the lowest possible cost. This is a very narrow and misguided view, and not at all how economists (should) think about economic efficiency.

When economists talk about efficiency, what they really mean is maximising total societal welfare. Total societal welfare is a very broad concept that encompasses economic prosperity, satisfaction, fulfilment and wellbeing.

So, when you hear economists mention efficiency, remember that what they are really referring to is, as the United States Declaration of Independence puts it, “the pursuit of Happiness.”[1]

Economic theory categorises efficiency into three dimensions:

Allocative efficiency is when all resources in the economy are allocated to their best possible use. When this occurs, it is impossible to make someone better off without making someone else worse off.[2]

Productive efficiency occurs when firms are producing a quantity and quality of output that maximises total societal welfare today at least cost.

Dynamic efficiency occurs when firms are making investment choices that result in future production that maximises total societal welfare over the long run.

For more than 30 years, the regulatory frameworks that have been applied in Australia to natural monopoly industries have generally framed the objective of maximising total societal welfare in terms of promoting the long term interests of consumers with respect to price, quality and reliability of essential services.

During those three decades there has been consensus amongst Australian regulators that the most effective way to promote the long term interests of consumers is to set regulated prices or revenues in a way that incentivises allocative, productive and dynamic efficiency. As the Australian Competition Tribunal has observed:

…it is axiomatic in the principles of regulatory economics, that promoting allocative, productive and dynamic efficiency generally serves the long term interests of consumers.[3]

Why efficiency should remain the only economic regulation objective

A second common misconception is that economic efficiency is simply a means to an end. Invariably, those who espouse this view are unable to articulate clearly what the ‘end’ is.

When efficiency is understood properly to mean the maximisation of total societal welfare (happiness), it becomes clear that economic efficiency is in fact the end goal, rather than simply the vehicle to get there.

As explained below, there are at least three reasons why the promotion of economic efficiency should be the sole objective of regulators.

Reason 1: Clarity of purpose

One of the first lessons from public choice theory is that the Government should only intervene in markets if there is clear evidence of a market failure.

Evidence of market failure is not a sufficient condition for intervention—since regulation is almost never costless, and those costs may outweigh the benefits of regulation—but it is a necessary one.

Hence, if the Government is to intervene in a market through regulation, it must be crystal clear why regulation is required in the first place.

Economic regulation of natural monopolies was developed to address a very specific type of market failure. Given the lack of competitive constraint faced by such firms, if left unconstrained, natural monopolies would have a strong incentive to exercise their market power to set prices and output at a level that would diminish total societal welfare.

This reduction of total societal welfare—referred to in the economics literature as the deadweight loss from monopoly—is a form of economic inefficiency.

Economic regulation aims to protect against that loss of economic efficiency by trying to reproduce as closely as possible the efficient outcomes of a market that does not suffer from that market failure.

Remember, the golden rule is that the Government should intervene in markets only if there is a clear market failure. In other words, Government remedies should be targeted to clearly defined market failures, where it can be demonstrated that the Government intervention would result in a net benefit to society.

The market failure problem associated with natural monopolies has remained fundamentally unchanged over the past 30 years. If economic inefficiency is the problem, then the solution must be regulatory frameworks that are oriented towards promoting economic efficiency.

Of course, there are many different types of market failure that can occur, apart from the classic market failure associated with natural monopolies.[4] Economic regulation may have a legitimate role in addressing these different types of market failure. However, in every such case, the sole objective must be to maximise economic efficiency.

Reason 2: Effective institutions

There is overwhelming evidence that the most successful organisations (public and private) are those that single-mindedly pursue one objective, rather than multiple (often competing and unstated) objectives.

There are two reasons for this.

Firstly, all the resources of the organisation can be marshalled in the same direction, towards achieving a common purpose—rather than being diverted ineffectively in different directions.

Secondly, some objectives conflict with one another. In these circumstances, it may be impossible to achieve one objective without sacrificing another.

For example, the pursuit of equity and social justice (which some at the ACCC/AER regulation conference advocated for) typically involves redistributions from one group to another. This inevitably results in some groups being cross subsidised by others. Cross subsidies do not simply involve a transfer of welfare between groups; they also result in a deadweight loss to society (i.e., a reduction of total societal welfare).

Hence, the pursuit of equity and social justice is usually irreconcilable with the goal of promoting economic efficiency. The only way to do more of one is to do less of the other.

Therefore, regulatory agencies are likely to be more effective if they are focussed on a single objective (the promotion of economic efficiency), rather than pursuing efficiency and equity/social justice.

This does not mean that genuine social problems should be ignored. The point is that whether and how such problems should be addressed ought to be left to policymakers rather than regulators to determine.[5]

Reason 3: Sound governance

Ronald Reagan said the nine most terrifying words in the English language are: “I’m from the Government, and I’m here to help.”

A very close second must be: “I’m a regulator, and I have a great idea.”

Many regulators seem to have a penchant for ‘innovation’, new thinking and broadening the scope of their activities. Whilst improvements to the regulatory framework are sometimes necessary to respond to new challenges, it is vital that regulators resist the urge to go beyond their core role and step into the shoes of policymakers.

Good governance requires a bright line to be drawn between the roles of policymakers and regulators. This clear separation of powers is essential to:

Reduce the risk of regulatory scope creep. As explained above, Government intervention in markets should be targeted at addressing well-defined market failures. Unchecked expansion of regulatory action is the antithesis of targeted intervention and is likely to result in more harm to society than good.

Ensure accountability of decision-making. If the regulator is permitted to make policy, and policymakers are permitted to act as quasi-regulators (e.g., by exerting political influence on a supposedly independent regulator), then it becomes impossible to hold policymakers to account for poor policy outcomes, and equally impossible to hold regulators accountable for poor regulatory outcomes. A lack of accountability will inevitably lead to poor decision-making and worse outcomes for society.

If we as a society are unhappy with the direction of policy, we can remove the ultimate policymakers (i.e., elected representatives) via the democratic process. In principle, this limits the scope for bad policies. If regulators encroach on the domain of policymakers and we are dissatisfied with the policies they introduce, given that they are (at least in Australia) unelected officials, how do we vote them out?

The need for accountability and restraint on the power of decisionmakers is why most free, democratic societies such as Australia have a clear separation between the executive, legislative and judicial branches of Government.

If left unconstrained, governing institutions have a tendency to seek the accumulation of power and influence, often to the detriment, rather than service, of society. The solution to this problem is to separate the power of institutions so that they can each be held to account, while providing checks and balances on one another.

The desire for a clear separation of powers was the reason why, for example, three different market bodies—the Australian Energy Market Operator (system planner and operator), the Australian Energy Market Commission (rule maker), the Australian Energy Regulator (regulator)—were established to govern the National Electricity Market.

These three agencies were given separate (rather than overlapping) mandates, powers and obligations.

In principle, this is a good model for the governance of institutions. Because the regulator is not permitted to make the rules that it enforces:

It cannot make changes to the regulatory framework on a whim. This produces more stable, predictable regulatory rules and outcomes; and

It is easier to identify whether good/bad outcomes are due to the design of the rules or their implementation. This is an important discipline on the regulator’s decision-making.

Equally, because the rule maker is not responsible for enforcement, it is free to design and evaluate the rules dispassionately and on their merits.

Of course, under this model, regulators may have a legitimate role in identifying problems (market failures) and bringing those to the attention of policymakers. However, the relationship between the regulator and policymakers should remain at arm’s length, with the regulator simply raising awareness of an issue and then leaving it to policymakers to assess in an open and transparent way whether and how the issue should be addressed. In order to maintain the separation of roles, the regulator should not become an activist or advocate for policy change.

Conclusion

There is no doubt that regulators today must make decisions under considerable uncertainty about the future, in the face of new challenges such as climate change, technological disruption and digitisation, the transformation of services and business models, amongst others.

These challenges may require regulators to re-evaluate how best to achieve the most efficient outcomes for society as a whole and to adapt their frameworks accordingly. But there is no case for abandoning the efficiency objective, or adding new objectives that are unrelated to the problem that regulation is intended to solve. Doing so would likely produce worse outcomes for society at large, blur the distinct roles of policymakers and regulators, undermine clarity of purpose and reduce the accountability of decision-makers.

[1] This point was made by Dr Darryl Biggar during the closing session of the conference.

[2] This is a condition known as Pareto optimality in the economics literature.

[3] Applications by Public Interest Advocacy Centre Ltd and Ausgrid [2016] ACompT 1, para. 93.

[4] Other examples might include misleading and deceptive conduct arising from asymmetric information, negative externalities, coordination failures, and so on.

[5] The rule that the Government should intervene in markets if and only if there is a clear market failure applies just as much to policymakers as it does to regulators. This means that before intervening to address claimed equity or social justice problems, policymakers must (a) demonstrate convincingly, with evidence, that there is in fact a real market failure rather than an imagined one, (b) demonstrate that the intervention would be net beneficial to society as a whole and (c) be transparent with the public about what the equity and social justice objectives are and what Government actions are being taken to pursue those objectives. Policymakers should not intervene unless they are willing and able to do all these things.

The case for developer charges: fair water infrastructure contributions promote better development outcomes and reduce infrastructure costs to the community

Developer groups have opposed Sydney Water and Hunter Water’s planned reintroduction of infrastructure contributions (or ‘developer charges’). These charges to developers help recover the area-specific, development-contingent costs of providing or upgrading the water, wastewater and stormwater drainage networks to serve new development.

However, such contributions have never been more important to the community. These charges signal to developers the costs of providing infrastructure in different areas, and thus promote socially optimal development decisions – i.e., development in locations where the benefits to the community exceed the costs. They also minimise price increases to customers’ water bills (helping to reduce cost of living pressures), and they allow some of the land value uplift generated by rezoning to fund much needed infrastructure.

Cost-reflective infrastructure contributions can also be an efficient and fair funding source for infrastructure provided by local councils to serve new developments, including much needed public open space, transport (eg, local roads) and local stormwater infrastructure.

The reintroduction of water and wastewater developer charges

The term ‘rent-seeking’ was first used to describe the wasting of resources by entrepreneurs to fight for artificially created wealth transfers. This is an apt description for the time spent in recent years by developers seeking to convince the NSW Government to resist the reintroduction of cost-reflective water, wastewater and stormwater infrastructure contributions (or ‘developer charges’) in Sydney and the Hunter.

Following a review by the NSW Productivity Commission in 2020, the NSW Government committed to reform the infrastructure contributions system, with a key element being the phased reintroduction of developer charges for Sydney Water and Hunter Water’s water, wastewater and stormwater services. This follows over a decade of these charges being set to zero (set by Ministerial direction in 2008). The consequence has been that Sydney Water and Hunter Water’s additional costs to provide water infrastructure to service new developments has not been recovered from developers, but from all water, wastewater and stormwater customers via their quarterly bills.

Under the methodology set by the NSW Independent Pricing and Regulatory Tribunal (IPART), these infrastructure contributions would recover Sydney Water and Hunter Water’s costs of providing water, wastewater and stormwater services to new development areas that are above and beyond the retail price revenue the water utilities will receive from servicing customers in the new development areas over time.[1]

Developers have long opposed paying these infrastructure contributions, arguing these costs should be borne by the wider community. They have suggested a broader revenue base (i.e., anyone but them) for infrastructure funding is needed, and that there is limited public benefit to infrastructure contributions.

Given concerns about housing affordability, the community is naturally interested in the key supply-side and demand-side drivers of house prices. Seeing an opportunity, developer groups have sought to re-prosecute their case opposing the developer charges as they claim they increase development costs and house prices.[2]

However, given the incentives at play, this requires closer scrutiny. Do these charges really increase development costs and house prices? What are the implications to the broader community and water customers if these infrastructure contributions are not reintroduced?

A cost to whom?

Infrastructure contributions may be a new cost to developers, but not to society. That is, infrastructure contributions do not create costs, they just represent a way of recovering them.

Since 2008, the costs of providing development-contingent water infrastructure have been paid by all water, wastewater and stormwater customers across Sydney Water and Hunter Water’s areas of operation through their regulated prices. IPART, with responsibility for setting maximum charges levied by Sydney Water and Hunter Water, explicitly accounts for these when setting the charges that are levied on customers via their quarterly bills. This decade old subsidy from water customers (including households) to developers has added billions of dollars to water bills of households and businesses, directly impacting the affordability of these essential services.

In 2019, IPART estimated that by 2029, Sydney Water’s average customer would be paying an additional $140 per year for their water, wastewater and stormwater services if infrastructure contributions were to continue to be set to zero.[3]

Despite the overwhelming current media focus on the cost of living, this impact on the affordability of water is one of the few areas that has escaped public scrutiny.

Re-introducing cost-reflective infrastructure contributions would simply reallocate these costs back to developers, who are creating the need to incur them and benefitting from them. This is in line with the “impactor pays” principle, enshrined in the Council of Australian Government’s National Water Initiative Pricing Principles, which were designed to increase the efficiency of Australia's water resources and infrastructure assets. This principle also underpins funding for a range of other critical services.

The reintroduction of infrastructure contributions would provide bill relief to all water customers, which will be increasingly important as major metropolitan centres in Greater Sydney and the Hunter continue to grow, and households face cost of living pressures.

Supporting planning objectives and efficient development

Cost-reflective infrastructure contributions also support planning objectives, by signalling to developers the costs of providing water infrastructure to different areas in Sydney and the Hunter – with some areas being higher cost and others lower cost to service, and these variations being ideally reflected in infrastructure contributions.

This price signal would encourage efficient development decisions. Currently, without such cost-reflective infrastructure contributions, developers do not need to consider the different cost of providing water infrastructure to different areas in Sydney. This means there is a risk they develop in areas where the costs to the community of providing such infrastructure exceeds the benefits of the development.

Smearing development-contingent costs across all water customers risks diluting one of the key signals related to the cost of development between locations, which in turn can contribute to inefficient investment in relatively high-cost areas.

As the NSW Premier and Productivity Commission have recently said, we need to improve how we plan and develop Sydney to minimise stretching of infrastructure services, including building more housing in infrastructure corridors to enhance amenity, lower infrastructure costs and improve housing affordability.[4]

Water infrastructure contributions and house prices

Provided developers have sufficient line of sight of infrastructure contributions (i.e., they are aware of these contributions before they purchase developable land), the economics of housing supply tells us that these costs are not necessarily passed through to homeowners through higher house prices.

As observed through numerous studies across multiple jurisdictions and the NSW Productivity Commission (see Box 1 in PDF Bulletin), they are likely to be factored into the prices developers pay for developable land – resulting in a lower than otherwise price to the landowner, who may still receive significant windfall gains by virtue of their land being rezoned or deemed developable.

That is, infrastructure contributions can allow some of the land value uplift generated by rezoning to fund much needed infrastructure.

If there are occasions where this means the landowner is not willing to sell to the developer, this would indicate that the benefits of the potential development in that location (as measured by what the developer is willing to pay for the land) does not exceed its costs to the community. However, this is unlikely to be common, as in an environment of increasing population, the value of developable land in and surrounding cities often exceeds its opportunity cost in alternative uses (e.g., for industrial use or agricultural production).

This key conclusion – that housing affordability is not exacerbated by infrastructure contributions, provided developers are aware of these contributions before they purchase developable land – is also backed up by empirical literature. Abelson (1999)[5], Ruming, Gurran and Randolph (2011)[6], Davidoff and Leigh (2013)[7] and Murray (2018)[8] all found that the incidence of development contributions likely falls on developers or landowners rather than home buyers.

The most reliable Australian evidence is consistent with this view; with little credible evidence to the contrary.[9]

The NSW Productivity Commission has observed that, as a policy to increase housing supply, setting Sydney Water and Hunter Water’s infrastructure contributions to zero has been ineffective and costly, predominantly resulting in a transfer of wealth from water customers to owners of developable land, “including those that would have developed land regardless”.[10]

Where to from here?

Cost-reflective infrastructure contributions can help to fund infrastructure more fairly, reduce pressure on water bills to residential and non-residential customers, and support better planning and development outcomes.

The focus should not be on whether these contributions should be reintroduced, but rather how to:

ensure water, wastewater and stormwater infrastructure solutions and services provided by Sydney Water and Hunter Water meet the community’s expectations and needs, including in relation to enhanced environmental, amenity and liveability outcomes;

set infrastructure contributions to ensure they reflect the efficient costs of development-contingent water, wastewater and stormwater infrastructure to various areas within Greater Sydney and the Hunter; and